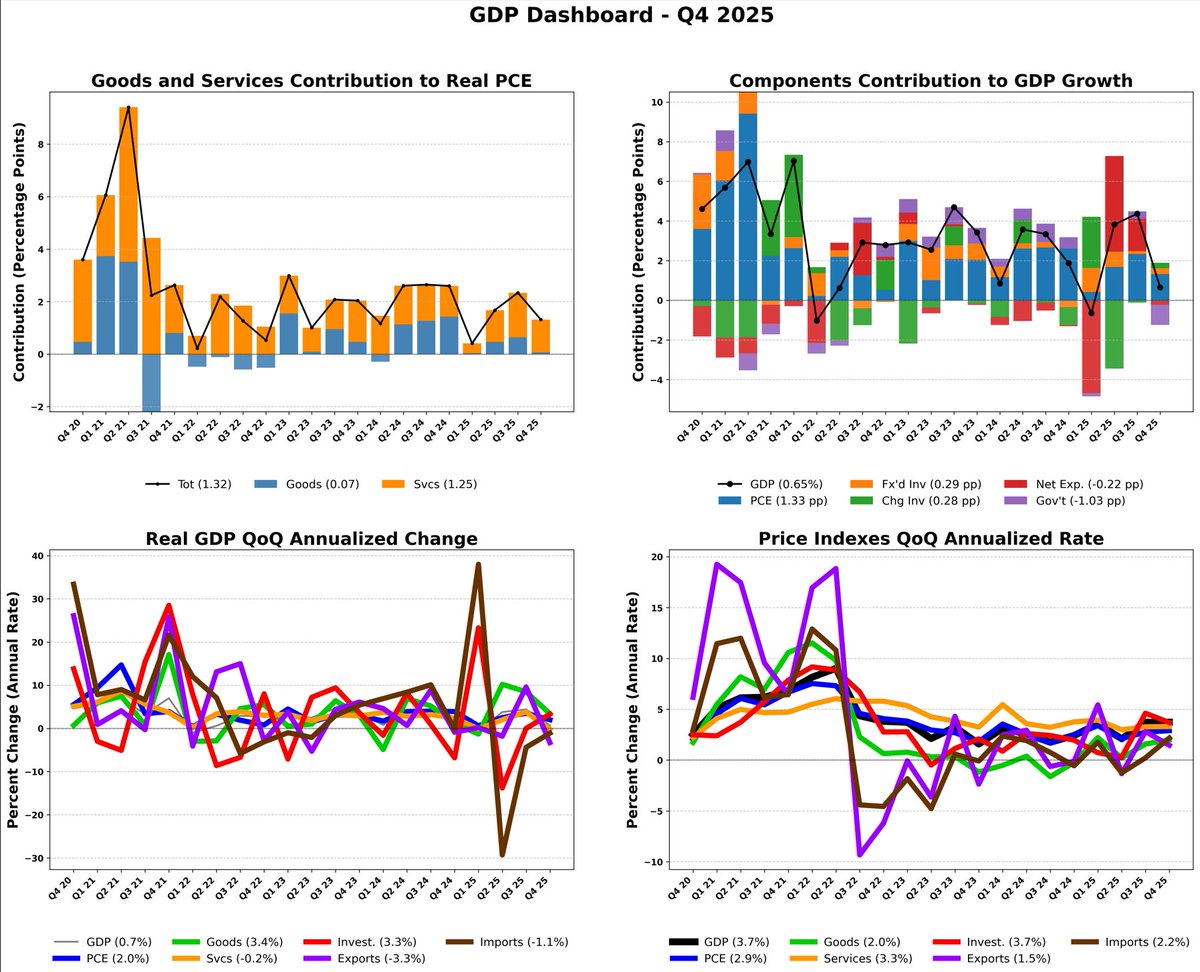

second estimate for Q4 2025 reveals a sharp deceleration in economic activity, with real GDP increasing at an annual rate of just 0.7 percent — down from 4.4 percent in Q3. This represents a downward revision of 0.7 percentage point from the advance estimate of 1.4 percent, driven by softer data across exports, consumer spending, government spending, and investment. A critical variable in this deceleration was the October–November 2025 federal government shutdown, which the BEA estimates subtracted about 1.0 percentage point from real GDP growth. Stripping out that temporary drag, underlying momentum remains modestly positive but is undeniably cooling, with real final sales to private domestic purchasers revised down to 1.9 percent from the advance estimate of 2.4 percent.

Adv(%) 2nd(%)

Real GDP 1.40 0.70

Curr$ GDP 5.10 4.50

Real Final Sales PrivPurch 2.40 1.90

Grs Dom Purch Price Idx 3.70 3.80

PCE Price Index 2.90 2.90

PCE Price Idx Excl F&E 2.70 2.70

On inflation, the gross domestic purchases price index was revised up to 3.8 percent, while the core PCE price index held unrevised at 2.7 percent. This divergence signals that cost pressures remain embedded in the broader domestic economy — including government and business purchases — even as consumer-facing inflation stabilizes. For the full year 2025, real GDP increased 2.1 percent, and annual core PCE came in at 2.8 percent, leaving the Federal Reserve constrained in its ability to ease policy.

The forward-looking picture is bifurcated. A mechanical rebound in government output is highly probable in Q1 2026 given the shutdown reversal, but the genuine cooling in private sector demand is real. The combination of slowing current-dollar GDP at 4.5 percent alongside an elevated gross domestic purchases price index of 3.8 percent presents late-cycle margin compression risks.

Expect a low-growth, sticky-inflation environment in early 2026.

#economy #recession #GDP #jobs #CPI #PPI #inflation #deflation #stagflation #Sales #wages #unemployment #employment #payrolls #earnings #Housing #trend #ISM #PMI #FOMC #Fed #Manufacturing #Services

English