HODL me-retweet

🚨 IMPORTANT: THE OIL SHOCK HASN’T HIT YET

The real damage might lands in May, June, and July.

And by then, central banks won’t be able to do anything about it.

Don’t believe me? Hear me out:

The Strait of Hormuz has been effectively closed since February 28, 2026.

20% of the world’s entire oil supply moves through that 21-mile passage every day.

Al Jazeera confirmed this is the largest disruption in fuel supply history.

Not in a decade, IN HISTORY.

Over 600 vessels are still stuck in the Gulf including 154 laden tankers waiting to exit, per Lloyd’s List.

A ceasefire was announced April 8. Oil dropped 9% on the headlines.

Then reality set in. Only 45 ships have transited the strait since the ceasefire was declared as of April 14, per Al Jazeera.

No formal transit windows. No security guarantees. Shipping companies are still pricing this as a war zone.

The EIA confirmed on April 7 that prices will stay elevated for months even after the conflict fully ends.

The numbers.

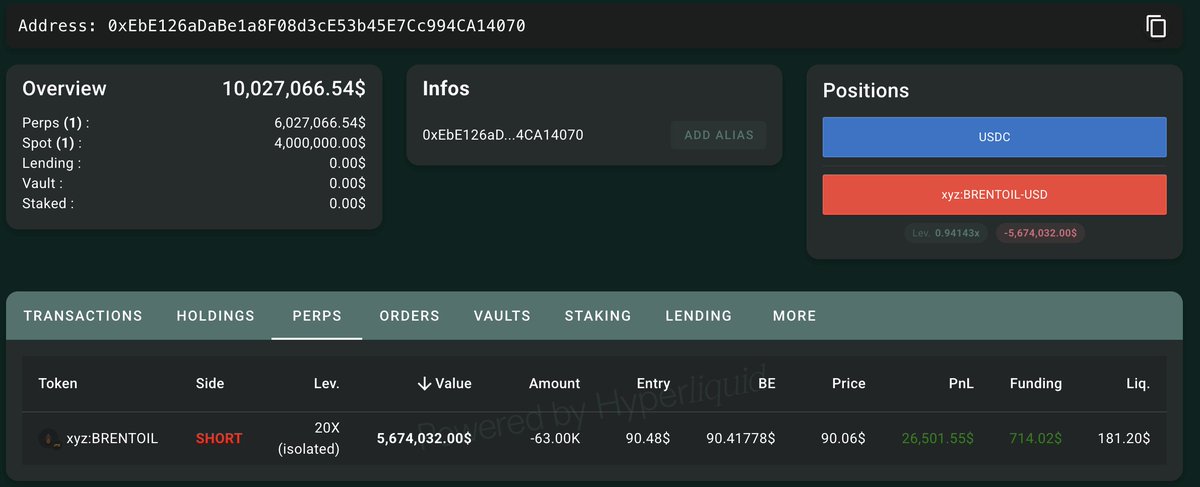

Brent was at $70.27 a year ago. It hit $111.69 on April 2. That is a 58.9% surge in 12 months.

National gasoline average hit $4.12 per gallon as of April 15, per EPRINC data.

West Coast diesel hit $6.92 per gallon, up 55.1% since the end of February.

US wholesale diesel and jet fuel benchmarks are up 67.3% and 70.3% respectively since the strait closed.

The myth you need to stop believing.

The US is a net crude oil importer. Full stop.

In 2025, the US imported 7.9 million barrels per day of crude while exporting 10.7 million barrels per day of refined products.

US refiners buy globally priced crude, refine it, and sell the products overseas.

Globally priced crude just went up 59%. That cost lands at your pump.

Why the worst hasn’t hit yet.

Oil shocks transmit in layers.

Wholesale first. Retail gas second. Then transportation, logistics, food prices, and finally core inflation.

That full transmission takes 3 to 6 months.

We are 7 weeks in. The CPI and PCE prints that actually reflect this shock have not been published yet.

If it stays closed another month.

The IMF’s severe scenario projects global growth collapsing to around 2%, global inflation hitting close to 6%, and a full global recession.

Even the base case, published April 14, cut global growth to 3.1% and raised inflation to 4.4%, a 0.6 percentage point upward revision driven entirely by energy prices.

The IEA released 400 million barrels of emergency reserves including 172 million from the US SPR.

That bought time, but it did not fix the problem.

The ceasefire is symbolic as long as 600 vessels are still sitting in the Gulf waiting for a green light that hasn’t come.

Inflation is not done. The lag is real. And the data proving it hasn’t even printed yet.

I’ve been doing this for a long time. The data analysis is my job so it doesn’t have to be yours.

My next market move gets posted to The Assembly first.

We’re closed right now. Reopening May 18 in about a month.

Join the waitlist at the bottom of the website: intheassembly.com

English