Blue Velvet Capital

647 posts

Interceptor STING takes down enemy Shaheds over water 💥

Thanks to the soldiers of the 39th Separate Coastal Defense Brigade for the great work!

English

@DavidGeorge83 retarded article (not to mention AI slop)

English

@EconstratPB irrelevant take, we learned nothing new

English

Thinking out loud here….

I was always told that for the US to lose hegemonic status it would need to lose a kinetic conflict against a peer competitor. And it had none so that was it. Maybe China.

But wut about losing a bluff to a middle power??

English

I believe today we're in an environment again where logic is more important than data.

Blue Velvet Capital@Blue_Velvet_Cap

Many of the big mistakes in investing start with saying "I'm not seeing it in the data". As a corollary, easiest alpha capture is when data is not available yet, but some simple observations + logical inference give conviction on an upcoming trend. Logic > Data

English

Blue Velvet Capital@Blue_Velvet_Cap

@DarioAmodei writes (wonderful essay btw): "I disagree with the notion of AI misalignment being inevitable from first principles." Dario, would you disagree that (1) AI is evolving, and (2) "misaligned AI" is equivalent to "AI that is mostly aligned with its own survival"?

QME

The Adolescence of Technology: an essay on the risks posed by powerful AI to national security, economies and democracy—and how we can defend against them: darioamodei.com/essay/the-adol…

English

@DarioAmodei writes (wonderful essay btw): "I disagree with the notion of AI misalignment being inevitable from first principles."

Dario, would you disagree that

(1) AI is evolving, and

(2) "misaligned AI" is equivalent to "AI that is mostly aligned with its own survival"?

English

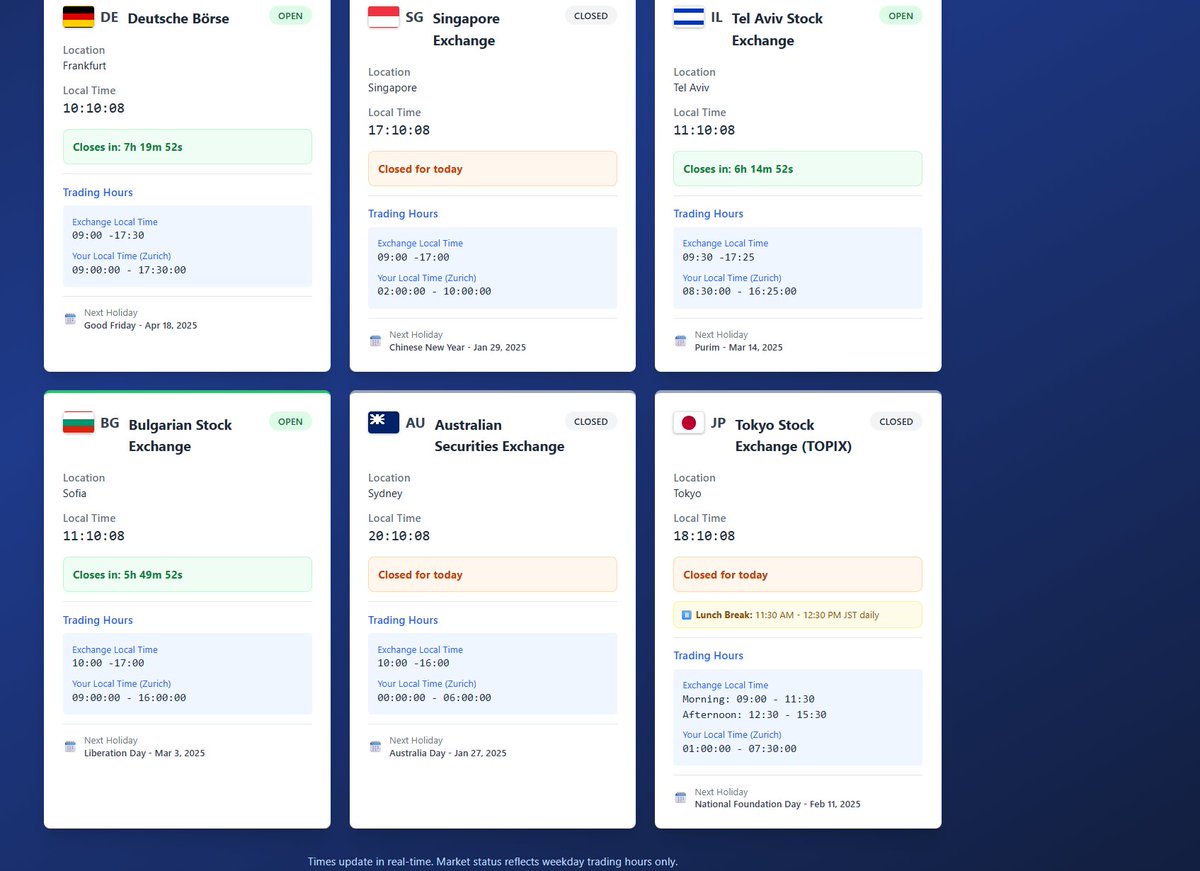

Not perfect, as The UK and AU flags are weirdish, but finally built a screen that helps immediate visibility on the opening hours and upcoming holidays for the exchanges I care about most (including the Japanese Lunch Break) :)

English

Just arrived at the Munich Security Conference to pitch all allies of Ukraine on imposing sanctions on the 8 oil refineries in China, India and Turkey who buy 90% of Putin’s oil. If this is done, Putin would run out of money in six months and could no longer afford the war.

English

DEUTSCHE BANK RESEARCH senkt das Kursziel für PVA TEPLA von 33 EUR auf 31 EUR. Buy.

Deutsch

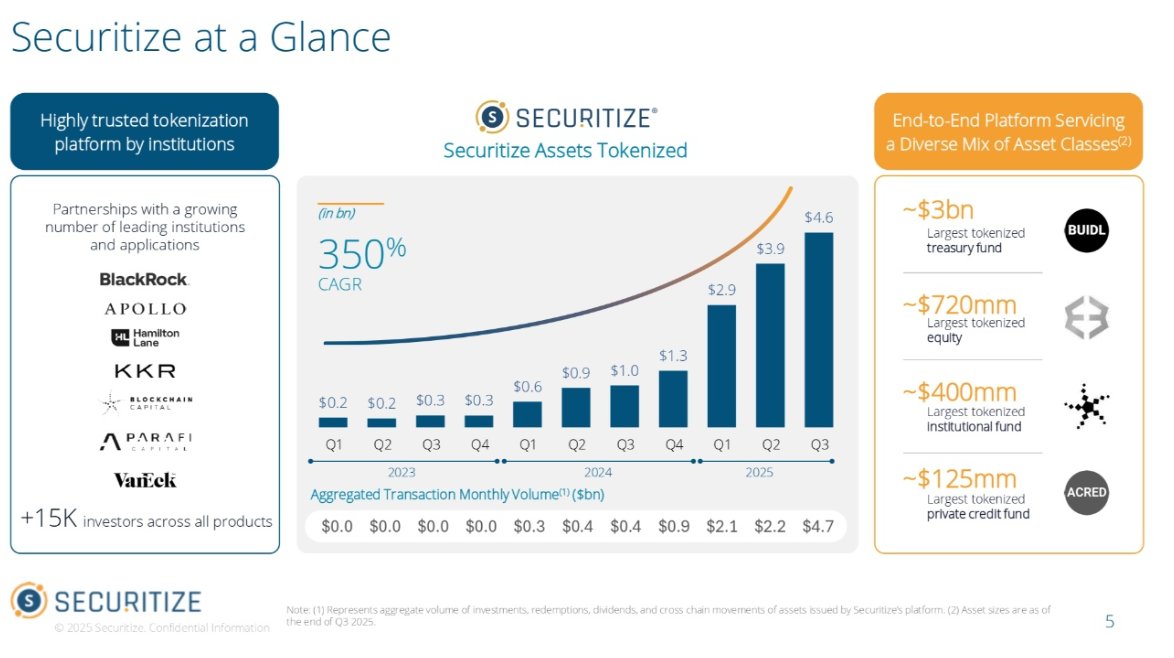

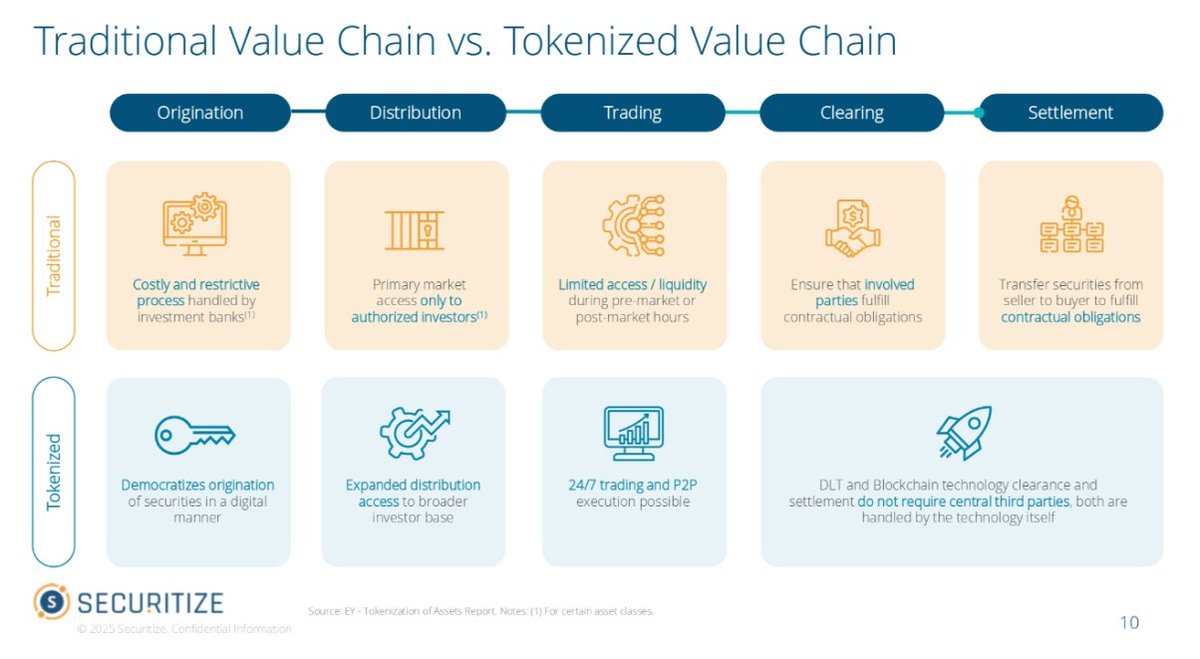

$CEPT @Securitize SPAC deal I'm actually interested in.

Tokenization could open up new opportunities for shortselling. Finally get some borrow in illiquid small-caps without being raped by IBKR and other middle-men.

Stablecoins with yield also an interesting use case.

English

ONE Nuclear Energy / Hennessy Capital Investment VII deal overview

Nuclear small modular reactor (SMR)

$1.1 billion enterprise value

Closing H1 2026

Symbol $ONEN

PR: sec.gov/Archives/edgar…

IR deck: sec.gov/Archives/edgar…

Disclosure: Long $HVII shares + rights in $ARB.to

English

@Fund_CDM Valuation is about 40% of my decision making process, in terms of weight (not in terms of time spent). The rest should be a mix of variant perception, top-down considerations, technical factors. Does that sound right? When I get lazy it goes to >50% very quickly.

English

If investors of a certain age are still obsessed with valuation work as their primary investment tool, it usually comes down to three things:

1) They don’t understand how markets actually work

2) They don’t understand who their competition is

3) They have a huge sense of entitlement

All three are red flags.

English

@themagicbakery One idea on distribution: many distributors have a lot of in-house knowledge which is effectively sold bundled with the product itself. Risk from AI is that the knowledge part gets commoditized so the risk of disintermediation goes up.

English

@S_curvecap @P_Remarks Question came from you trying to "influence your peers". I'm just wondering why, if it doesn't give you an edge... Get their views, share yours and why care what they think? At least that's how I do it...

English

@Blue_Velvet_Cap @P_Remarks i don't really get the q -- you're always selling in this biz, it's a requirement not really "edge"

do it in every channel. don't like what ss is modeling? call them to figure out rationale / get them to see why you think diff

pitch buyside friends ideas, understand both sides

English

Without getting mired in the "pod vs SM/LO" debate, I'll just offer that the ppl I know who have lasted the longest in the MM model (& have made the most $$$) are way better at thinking through LT debates than most of Fintwit assumes.

English

@S_curvecap @P_Remarks Very interesting. Question. Is that sales aspect really significant enough for pods that it's part of their edge? Surprises me. And what is the main channel, influencing the buy side or sell side?

English

Fair pt - it felt nonsensical to me until I did it. Then I came to see it just as a sales aspect of my job where I'm trying to influence my peers so my positioning wld benefit

We're all doing that w/ stock pitches anyway

I get your pt tho which is more the hyperbole ppl feel compelled to put fwd to defend essentially a thesis that something shld be a "relative u/p" -- but again, understandable when you look at incentives/scale

English

@valwithcatalyst @valwithcatalyst your 11% mentioned above seems wrong now?

English

$CCCM

BCA finally out sec.gov/Archives/edgar…

RLH Capital@valwithcatalyst

$CCCM Might be beating a dead horse here, but after digesting everything, wanted to chime in. Also happy to host a Spaces w/ @vik_mittal talk about the deal, SPACs broadly, and crypto transactions we’re seeing (disclosure: I’m not a crypto guy). The thesis is simple: BTC treasury names have been trading at 1.5–3.0x NAV. That creates real value opportunities. We’ve seen it before—PIPEs like $UPXI and $SBET, and $CEP —where investors came in around 1.0x NAV ($10 in CEP’s case). The SPAC wrinkle: The promote (and @APompliano's piece) creates real dilution. To get PIPE investors in at ~1.1x NAV, they raised at $8.00 and added a $13 convert (1.7x NAV). This leaves public holders paying: 1.33x NAV @ $10 1.4x @ $10.50 (pre-FT leak) 2.1x @ $15.76 (pre-announcement pop, although ripped into end of day) BTC exposure: Majority goes to the PIPE, which makes sense—they're the ones immediately buying BTC. Trust account stays in cash, so it only gets ~11% of the upside if BTC runs. Execution of announcement was terrible. The $8 PIPE price should’ve been front and center and the presentation immediately released. I didn’t feel comfortable selling stock, and many funds were restricted until the investor deck hit. Negative Technical Dynamic There was significant overlap between IPO and wall-crossed investors, investors who usually lighten up at unit split. These investors are likely sellers at this point. Only ~13M shares traded since announcement, so float still needs to turn. Interesting side note: In another SPAC deal leak, the PIPE price wasn’t disclosed - and considering this transaction that would have been a critical part of the leak. Why don’t arbs raise PIPEs for every SPAC above trust? Risk is totally different. Here, I take real BTC downside risk, no liquidity, and can’t margin the position. Our average PIPE is ~10% of our SPAC sizing—this isn’t the same. Everyone’s frustrated. Losses hurt. Emotions are high. So the only real question is: Where do we go from here? You either believe BTC treasuries trade at 1.5–3.0x NAV (implying $11.25–$22.50 stock), or you don’t. Trust has ~$10.04, heading to $10.25 by year-end. If you’re bullish BTC, the skew is compelling. One final note on the warrants: 5-year levered BTC vol is high. Optionality is meaningful. Disclosure: we are long common and warrants, and participated in the PIPE (at 10% of our usual SPAC position size)

English

@APompliano nobody cares about your stupid video's, give us the investor deck

English

I announced a $750 million fundraise this morning as part of a $1 billion merger.

The goal is to build a leading bitcoin-native financial services firm.

$CCCM

English

@APompliano post an investor deck! -- I knew this would be amateur hour, but it's even worse than I expected!!

English

@hfreflection Overall worldview, intuition and ability to read people matter even more. Having a natural sense for which ideas and things make sense, which things are bullshit, and the various shades in between. And then at the same time, understanding change and maintaining an open mind.

English

What traits do you think are important for younger analysts to be successful, and how do you think AI is changing the skills required? I will share some thoughts but curious other perspectives.

English