固定されたツイート

Talkot

3.3K posts

Talkot

@Talkot

Bond geek that utilizes equity investments to express interest rate and macroeconomic inefficiencies. Still enjoys a good high risk venture investment as well.

San Francisco 参加日 Aralık 2010

390 フォロー中944 フォロワー

$DX released earnings this morning and book value (BV)came at $12.60 on 3/31 much lower than expected due to spread widening. Since then book has improved to $13.31. The portfolio grew from $16.2B to $22.2B or almost 40%. Leverage increased from 7.3X to 8.2X. The ATM was busy as well raising $440M in new capital. Clearly $DX is growing very agressively. The G&A expense was very high @ 2.1% vs capital for the quarter. It's now trading at a premium to book. Let's hope they can grow without a hiccup but I'm on the sidelines watching.

English

Talkot がリツイート

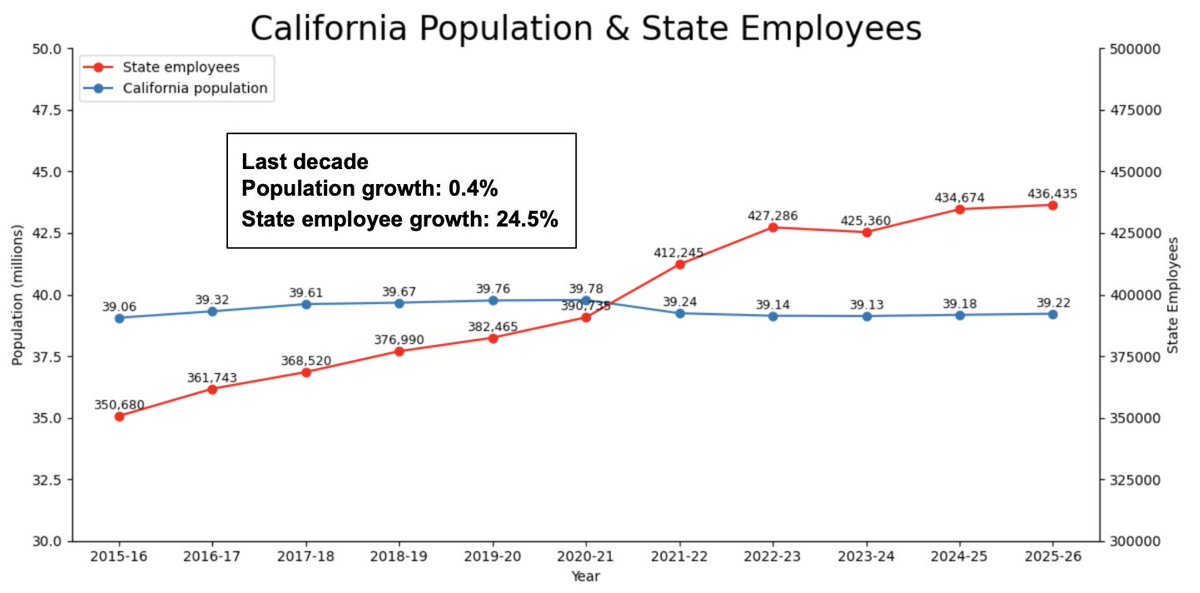

California's population grew 0.4% in the last decade.

The number of state employees grew 24.5%.

Total state spending grew 48%, inflation adjusted.

You have to ask - where did all the money go?

Kenneth Schrupp@kennethschrupp

Newsom has nearly doubled state spending, but where has the money gone? Our latest @CityJournal California report explains how $180B or more of taxpayer funds appears to have evaporated into the hands of fraudsters and criminals.

English

Talkot がリツイート

Repeat after me: There is NO housing shortage.

There IS a yawning housing DISCONNECT between Boomers (avg # children=3.2) & Millennials (avg # children=2.0) & Gen Z (TBD but much lower).

WHO will buy Boomers’ homes as they die?

Multigenerational HH formation to keep rising.

Capital Markets Guy@CapitalMktGuy

Nearly 10mo of housing supply. What ever happened to the housing shortage?

English

$FNKO — Valye Company Analysis

Funko, Inc. operates as a prominent player in the pop culture consumer products market with a diversified portfolio of licensed properties and proprietary brands, offering collectible figures, accessories, and apparel globally. Despite stro

Key points:

• Operating losses intensified dramatically in 2025, with operating income at -$45.5M following a positive operating income of $13.0M in 2024 [F1].

• Net losses deepened markedly to -$67.4M in 2025 from -$14.7M in the prior year [F1].

• Operating cash flow turned negative to -$5.1M in 2025 from a robust positive $123.5M in 2024, while capital expenditures remained steady near $33M [F1].

• Free cash flow was approximately negative $38M in 2025 indicating cash burn despite efforts [F1].

• Equity contracted to $186M at end-2025 from $233M in 2024, reflecting ongoing capitalization challenges [F1].

Read: valye.com/news/fnko-comp…

#ValyeAI #Stocks #StockAnalysis #StocksInFocus #FNKO #StockMarket #PopCulture #ConsumerProducts #Collectibles #MarketNews

English

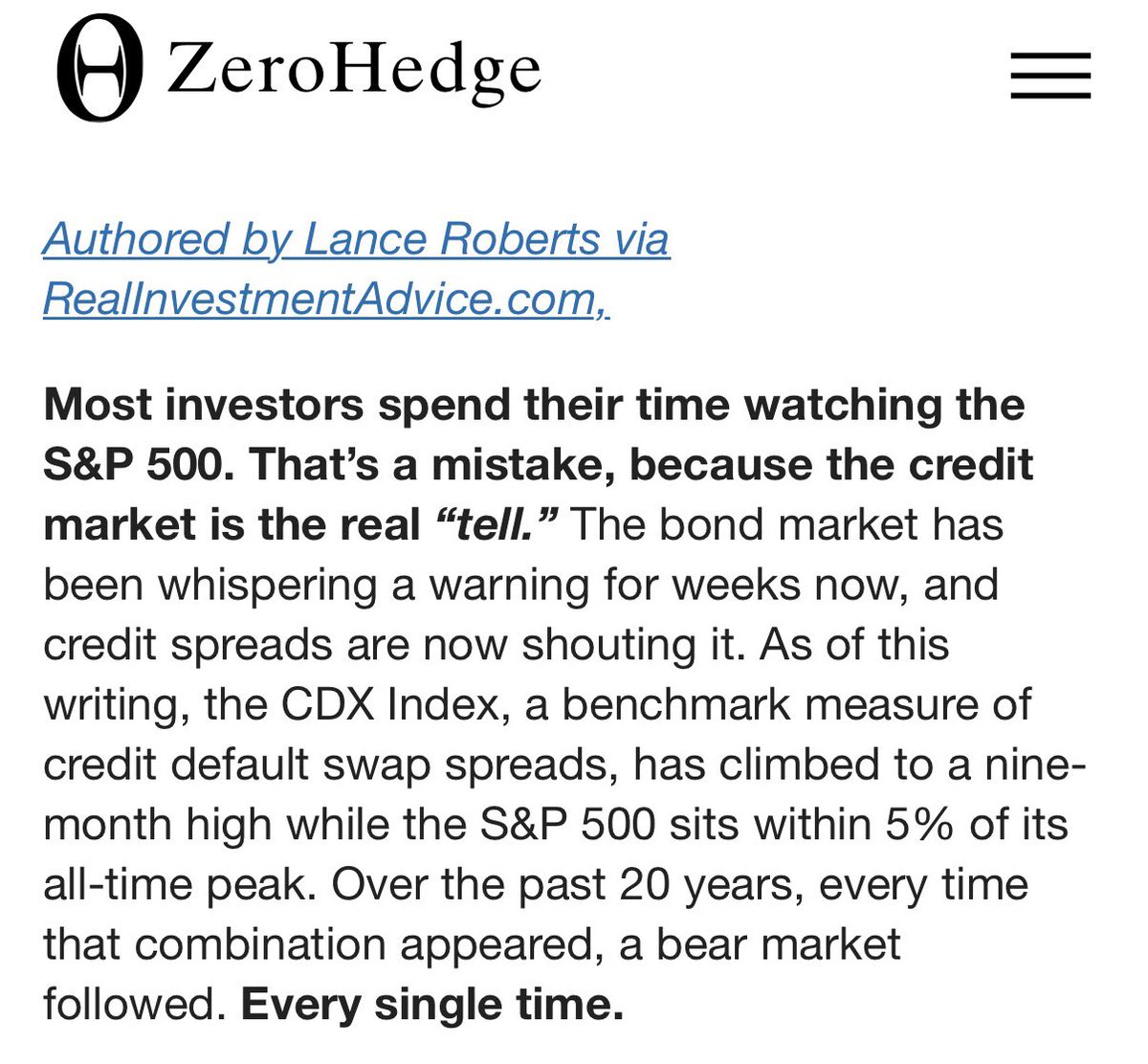

I feel like we're watching a "Sam Peckinpah" movie. Very slow motion with tons of carnage being created. Caveat Emptor.

A fund holding consumer and small-business loans made by companies including Affirm and Block is the latest corner of the private-credit market to come under stress wsj.com/finance/invest… via @WSJ

English

Talkot がリツイート

The metrics of success for California should be how much wealth are we creating for every family in real dollars & reducing the cost of living. Every resident in California should have the opportunity to share in the economic growth of our state.

English

$FNKO will release FY2025 earnings this Thursday. Lots to digest:

-Price increase late last year from $11.99 to $14.99

-Tariff relief from $40MM paid in 2025

-New CEO Josh Simon to give FY2026 guidance

-Activist Pleasant Lake Partners seeking strategic review

-Possible Short squeeze if business parameters look better than the 10% short interest indicate.

-FNKO debt was rolled forward giving them time to improve business metrics

Could be a wild ride......

English

@GardinerIsland $WD had their investor day today and from the price reaction it didn't go very well. I suspect quite a few skeletons in that closet for now. I'm not enamored with originators right now.

English

@Talkot helluva call ... up 33% since you posted this in Dec despite US markets weak

how about $WD ? $155 to $47 since 2021

over done yet ?

English

Talkot がリツイート

Talkot がリツイート

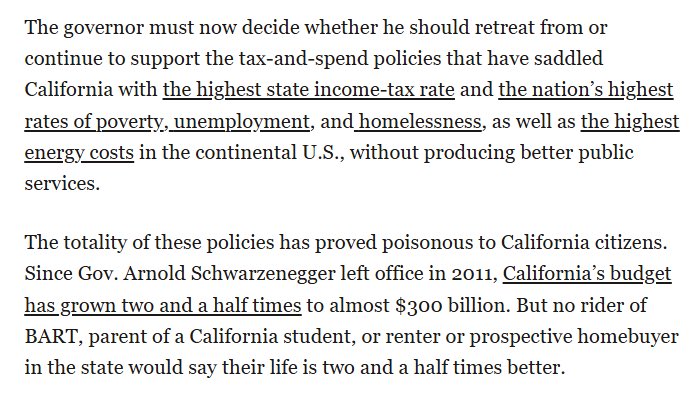

The State of California has been run top to bottom by one party since 2011.

Here are their results:

1) highest state income tax

2) highest rate of poverty

3) highest rate of unemployment

4) highest rate of homelessness

5) highest energy costs

Hard to explain this away.

English