고정된 트윗

Don't let stock price movements influence your perception of a company's business fundamentals.

English

Feather Fund

5.6K posts

@FeatherFund

Compounding knowledge @ https://t.co/yZ9v7H5Vvv Not financial advice.

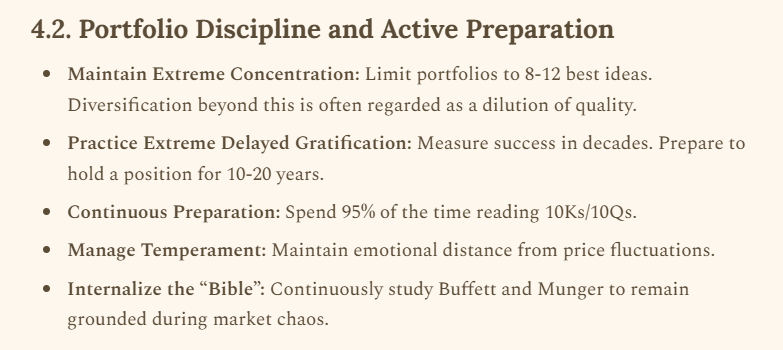

Michael Mauboussin on how the best investors behave

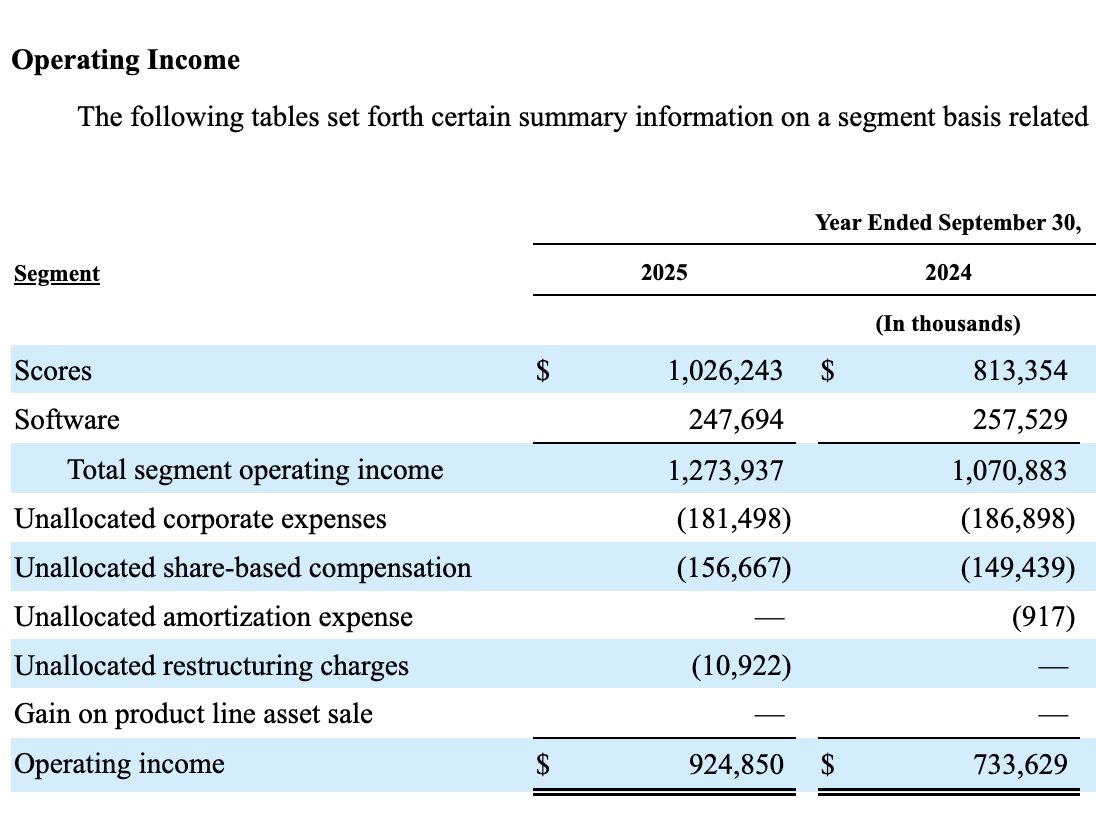

Heterogenous loan pools – that is, those that use both $FICO and VantageScore – are harder to price and we believe that MBS investors will demand a discount for loan pools scored with VantageScore. This supports the notion of the FICO Score being deeply entrenched.

We also look at a number of scenarios that comp $FICO pricing against VantageScore in light of the economics that the credit bureau will receive from each. Our conclusion is that a race to the bottom on Scores prices is extremely unlikely (more in the report on this).

We attempt to decompose the credit report cost into its constituent parts, including the royalties $FICO receives as well as credit bureau fees and markup of the FICO Score. FICO is directly responsible for only 33% of the 2022 to 2025 credit report cost inflation.