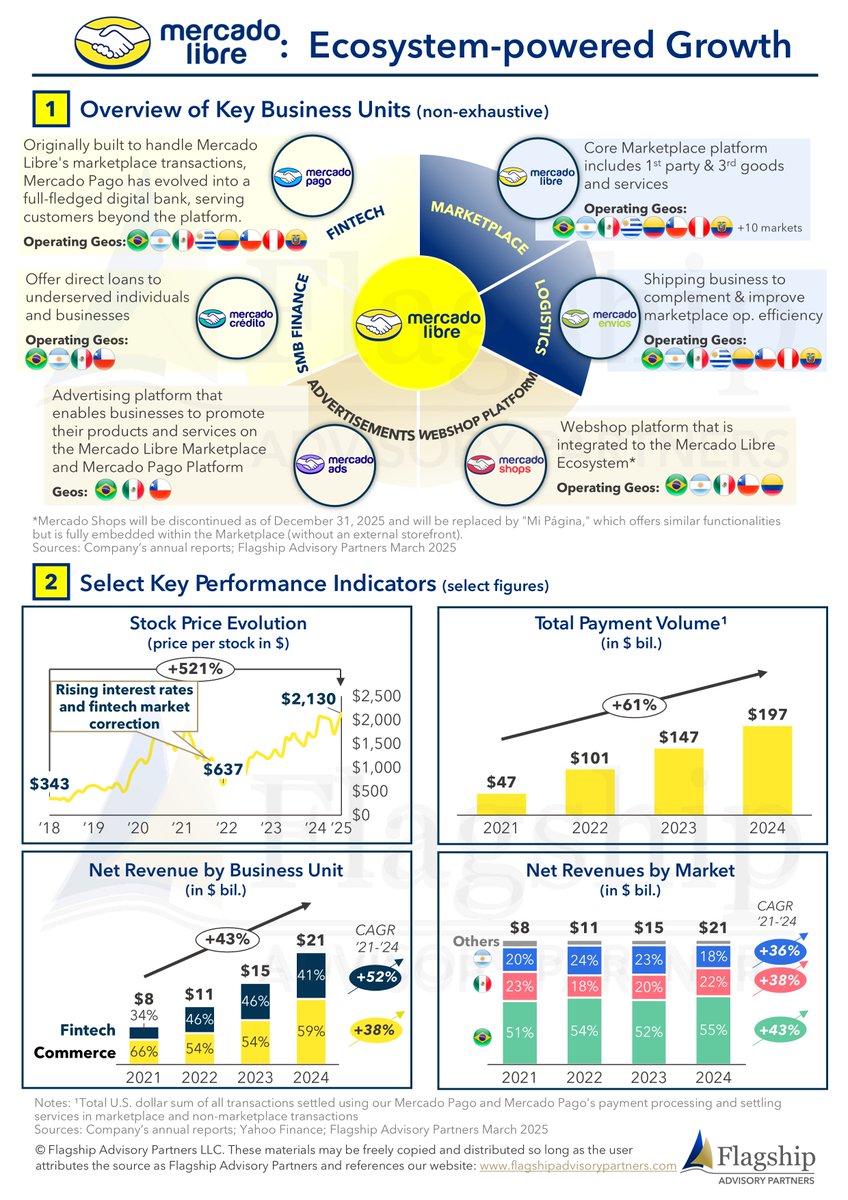

Latam powerhouse @Mercadolibre is a global example of how to successfully integrate fintech with commerce, showing how platform-driven expansion and embedded finance can transform digital businesses: insights.flagshipadvisorypartners.com/mercado-libre-… #fintech #payments #latam #Argentina #brazil

English