FRAGMENTS Value

1.8K posts

FRAGMENTS Value

@FragmentsValue

“Deep value investor✦ $1-for-50¢ opportunities ✦ Cycles, catalysts, conviction ✦ FRAGMENTS” #Fragments

가입일 Haziran 2017

269 팔로잉136 팔로워

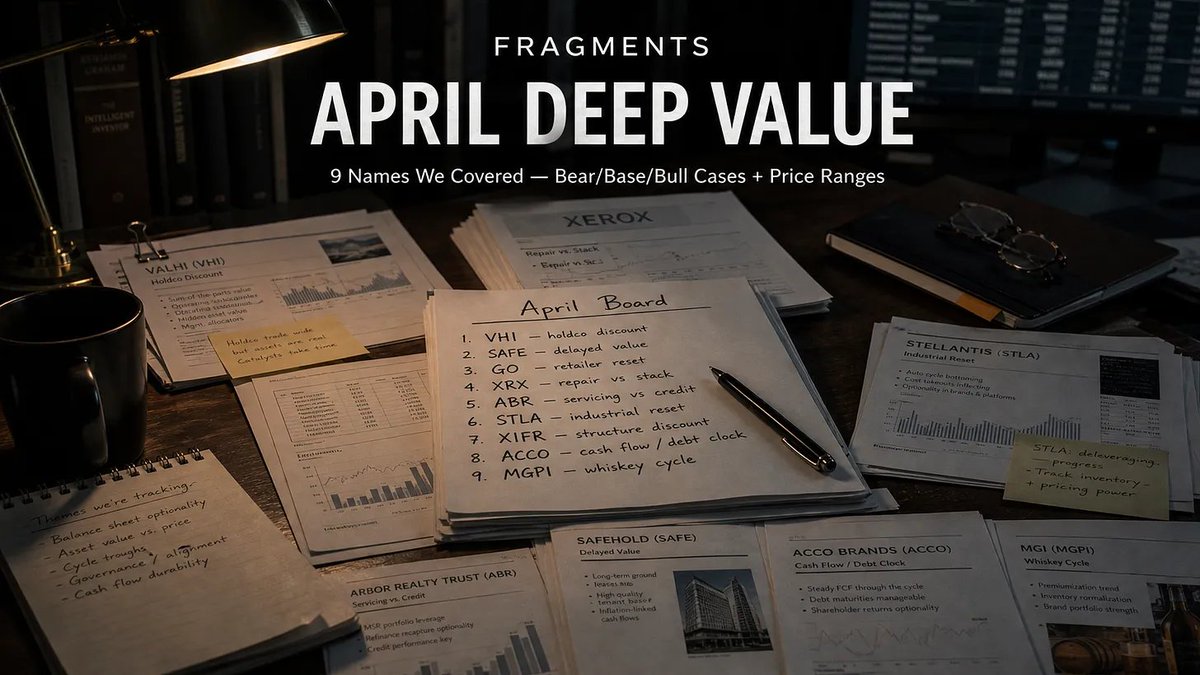

APRIL DEEP VALUE — 9 Names We Covered

It brings together the Deep Value Reports from April into one full write-up.

Inside, I go through the names we covered during the month, give a short read on each one, and lay out the Bear / Base / Bull cases with price ranges for each one.

A few of these names are messy. A few are misunderstood. A few are being priced like the market has already made up its mind.

That is usually where things start to get interesting.

So this article is a clean way to see the whole April board at once — the names, the pressure behind each one, the downside, the upside, and the range of outcomes.

If you followed the deep value work this month, this is the easiest way to see it all in one place.

If you missed some of the reports, this is the best place to start.

There are some very real opportunities in here. Not easy ones. Not always comfortable ones. But real ones.

Here:cundilldeepvalue.substack.com/p/april-deep-v…

$XRX

English

FRAGMENTS Value 리트윗함

Deep Value Report — Stellantis $STLA

This is not a pretty stock.

Stellantis has a huge share count, a lot of debt, and a lot that still needs to be repaired. But it also still has a lot of cash, a lot of liquidity, meaningful finance value, and operating regions that continue to produce real profits.

That is what makes this one interesting.

The market is pricing Stellantis more like a failed repair story than a business that still has time and value left inside it.

In our new report, we go through the full file: 5-year history, balance sheet, asset map, what the equity sits behind, and where we think the stock could be worth more than the current price suggests.

Full Deep Value Report on $STLA is now live.

Here:cundilldeepvalue.substack.com/p/deep-value-r…

English

Deep Value Report — $MGPI

I spent time on MGPI because the stock looked too cheap to ignore, but not cheap in the easy way.

Yes, it trades well below book value.

But that’s not the report.

The report is really about what happens when a company owns real barrels, real warehouses, real brands, and real distilling assets… right when the whiskey cycle turns against them.

That is where the case gets interesting.

Because if the market is right, those barrels are trapped capital.

But if the market is too harsh, MGPI may still have a lot more value than the stock price is giving it credit for.

We went through the balance sheet, the inventory, Penelope, the debt, the insiders, and our Bear/Base/Bull cases.

Here:cundilldeepvalue.substack.com/p/deep-value-r…

English

FRAGMENTS Value 리트윗함

Deep Value Report — Xerox $XRX

I just published a new Deep Value Report on Xerox.

This is really deep value.

What makes it interesting is that there is still real value inside the business, even with all the debt and all the noise around it.

I put actual numbers on it with a Bear case, Base case, and Bull case.

Carl Icahn has been in this file before. The Deason side is still there with real ownership. There is real skin in the game, real cash flow, and a real reason to dig deeper here.

That’s what I did in the report.

HERE:cundilldeepvalue.substack.com/p/deep-value-r…

English

FRAGMENTS Value 리트윗함

Deep Value Report — Arbor Realty Trust $ABR

I just published my new report on Arbor Realty Trust.

This is the kind of stock the market stops looking at too early.

People see the credit stress, the dividend cut, the ugly cleanup, and they move on. That is exactly where it starts to get interesting.

Because under all of that, there is still a real business here: a large servicing platform, real fee income, real capital markets access, and maybe more value left for the common than the stock price is giving it credit for.

That is what I wanted to measure properly in this report.

Here:cundilldeepvalue.substack.com/p/deep-value-r…

English

Deep Value Report — $MGPI

MGPI is not the kind of deep value case where you just point at book value and move on.

The stock is around $20. The company still has real assets, real brands, real barrels, real warehouses, and real cash flow.

But the whiskey market is ugly right now. Customers slowed down. Inventory built up. Distilling got hit. Penelope created a real cash obligation.

That is why the stock is cheap.

The question is whether the market is pricing a temporary reset like permanent damage.

That’s what we tried to answer in the Deep Value Report.

Here:cundilldeepvalue.substack.com/p/deep-value-r…

English

New Deep Value Report is live: ACCO Brands $ACCO

This one is simple.

The market is not giving ACCO much credit right now. Sales have been under pressure, the balance sheet has debt, and investors clearly do not trust the story.

But the stock is around $3.31, book equity is about $7.37 per share, and management is still guiding to $75M–$85M of free cash flow in 2026.

That gap is why I spent time on it.

In the report, I go through the balance sheet, working capital, division value, debt timeline, buybacks, insiders, holders, and Bear/Base/Bull math.

Here:cundilldeepvalue.substack.com/p/deep-value-r…

English

Scott Barbee: How Deep Value Looks Before It Works

Scott Barbee is a really interesting investor because his method is not built around clean stories.

He goes into the part of the market most people don’t want to study: small companies, ugly sectors, hard assets, cyclicality, and situations that need patience before they make sense.

In this piece, I wanted to explain where he comes from, how his process works, and why his way of looking at a stock is different from just saying “it’s cheap.”

Here:cundilldeepvalue.substack.com/p/fund-manager…

$CAT

English

Scott Barbee: How Deep Value Looks Before It Works

This Fund Manager Series piece is about Scott Barbee, but it is not just a biography.

I wanted to go deeper into his method.

How does he look at an ugly stock before it becomes obvious? What does he check first? How does he separate a broken business from a hated one?

That’s why I used Capital Limited as the case study.

Not to copy the position, but to show the mechanics behind the way he thinks.

Here:cundilldeepvalue.substack.com/p/fund-manager…

$CVE

English

I just published my new Deep Value Report on ACCO Brands $ACCO

At around $3.31, the stock is trading well below book equity per share, while management is still guiding to $75M–$85M of free cash flow in 2026.

That is what made me open the file.

This is not a flashy business. It owns boring, familiar brands: Mead, Five Star, Swingline, Kensington, PowerA, AT-A-GLANCE, Leitz, GBC, Rexel, Tilibra, Quartet, Derwent and Artline.

But at this price, boring is not the problem.

The question is whether the market is discounting the cash flow too aggressively.

Full Deep Value Report is live now.

Here:cundilldeepvalue.substack.com/p/deep-value-r…

English

@tbonecapital Yes you right, but its manageable. I talk about it in the report. :)

English

@traderInosuke $ACCO ;)

x.com/FragmentsValue…

FRAGMENTS Value@FragmentsValue

I just published my new Deep Value Report on ACCO Brands $ACCO At around $3.31, the stock is trading well below book equity per share, while management is still guiding to $75M–$85M of free cash flow in 2026. That is what made me open the file. This is not a flashy business. It owns boring, familiar brands: Mead, Five Star, Swingline, Kensington, PowerA, AT-A-GLANCE, Leitz, GBC, Rexel, Tilibra, Quartet, Derwent and Artline. But at this price, boring is not the problem. The question is whether the market is discounting the cash flow too aggressively. Full Deep Value Report is live now. Here:cundilldeepvalue.substack.com/p/deep-value-r…