Gobe@StrateGeee

Samsung Electronics ($005930.KS / $SMSN / $SMSD) reported Q1 2026 earnings, today, April 30th (fair disclosure). But we're still waiting on the call for more indepth information.

Headline:

- Revenue: ₩133.87T vs ₩126.29T (FactSet) / ₩131.00T (Sharp) → 🟢 BEAT (+6.0% / +2.2%)

- Operating profit: ₩57.23T vs ₩50.85T → 🟢 BEAT (+12.6%)

- Net Income: ₩47.23T vs ₩40.59T → 🟢 BEAT (+16.4%)

- EPS: not disclosed in preliminary filing (₩6,028 FactSet / ₩6,817 Sharp consensus to watch in full release)

The Sharp consensus sitting ~13% above the broad consensus on EPS is the tell — sell-side is still catching up to the memory cycle.

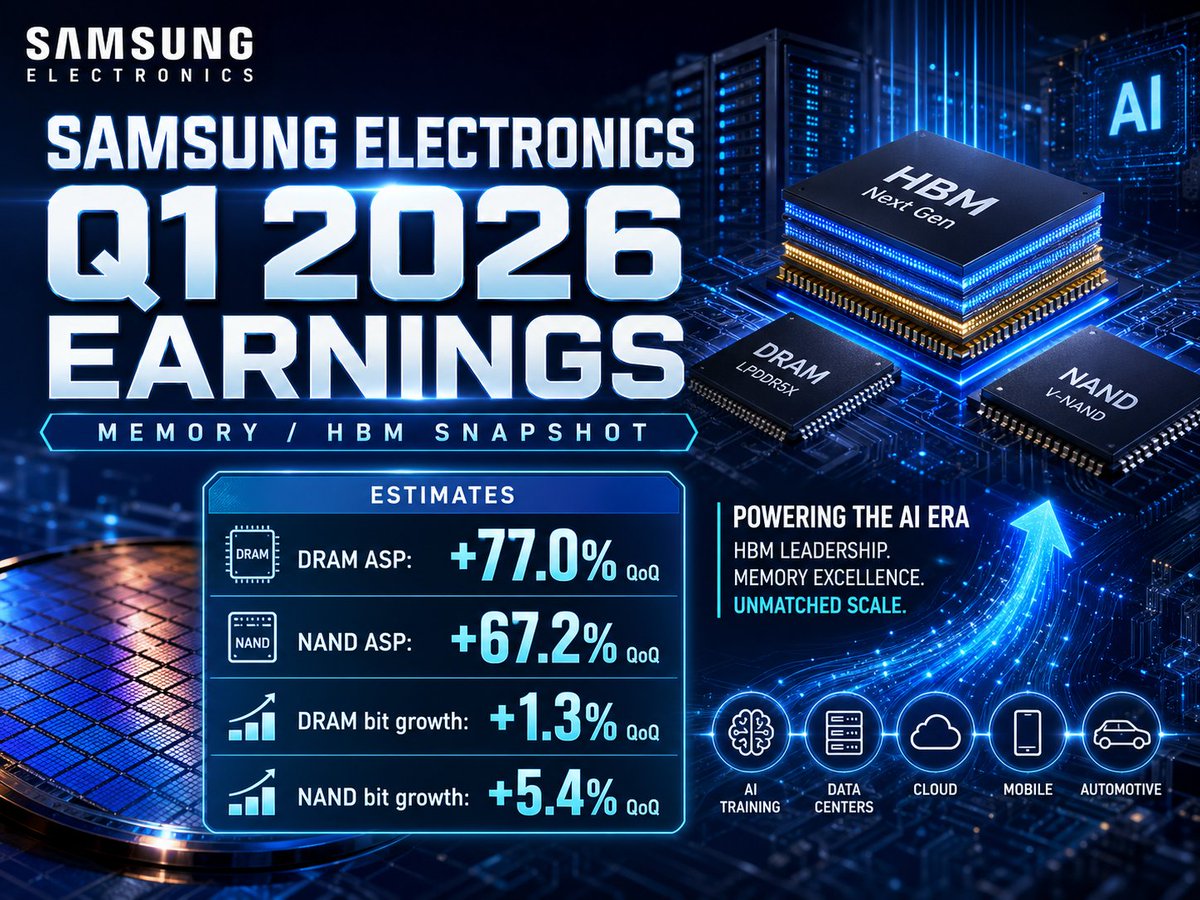

The memory super-cycle is the story (Q1 '26E):

DRAM ASP: +77.0% QoQ

NAND ASP: +67.2% QoQ

DRAM bit growth: +1.3% QoQ

NAND bit growth: +5.4% QoQ

According to estimates, pricing is doing most of the heavy lifting.

Exactly the dynamic flagged on $QCOM earnings call — memory supply constraints pressuring [handset] OEMs.

- As expected, consumer electronics are taking the largest hit from rising memory prices.

Samsung sits on both sides of that trade.

Segments (Q1 '26E segment actuals pending in full release):

1. DX - Device Experience (mobile + consumer): ₩51.01T revenue, ₩3.08T EBIT

2. VD/DA - Visual Display & Digital Appliances: ₩14.66T revenue, ₩0.18T EBIT

3. DS - Device Solutions (chips/foundry/memory): ~₩47.6T EBIT — ~93% of total operating profit (implied estimates)

For context: Q1 2026 EBIT alone (₩57.23T actual) now exceeds full-year FY2025 EBIT of ₩43.60T by ~31% — a single quarter eclipsed the entire prior year.

Cash flow:

- CapEx.: ₩18.05T

- Cash Flow from Operations: ₩9.23T

- FCF: -₩4.97T (front-loaded capex; FCF expected to turn positive in Q2)

The setup: 43 analysts | Buy rating (1.15)

- Target: ₩288,711 vs current ₩226,000 → +27.7% upside

- Forward P/E (FY26E): 6.5x

What I'm watching: whether HBM/DDR5 mix commentary supports the consolidated FY26E EBIT of ₩288.6T vs. ₩43.6T in 2025 (a 6.6x jump), and any read-through on memory ASP trajectory beyond Q2.

The FactSet curve has DRAM ASP decelerating to approx. +24% QoQ in Q2, +7% in Q3, +3% in Q4 — meaning consensus is that the bulk of the upcycle is already in the Q1 print.

Beat or miss matters less than the forward guide on memory pricing into 2H 2026.

SK Hynix did not comment on HBM as a share of DRAM, maybe Samsung will shine some light on theirs?