UnderTheBalanceSheet

164 posts

$ZIM

"Calcalist has learned that the party originally intended to be the Israeli partner in the deal was Udi Angel, through his investment firm, XT. Although all terms had been finalized with Angel, a delay in signing the agreement led Hapag-Lloyd to begin last-minute negotiations with FIMI just two weeks ago. These talks matured into a binding Memorandum of Understanding, as FIMI was prepared to accept several clauses that Angel had hesitated to approve."

Udi Angel was formerly married to Liora Ofer, the daughter of Yuli Ofer, the couple has a son and a daughter and divorced in 1995. Their son, Ori Angel, was appointed CEO of Ofer Shipping in October 2007.

Angel joined the Ofer Shipping Group (owned by the Ofer Brothers Group) in 1975 and was appointed CEO in 1980.

Major Business Milestones:

1999: He was a partner in the acquisition of Israel Corporation from Shaul Eisenberg.

1999-2003: He served as the Chairman of Zim Integrated Shipping Services.

2012: Together with Idan Ofer, he initiated the rebranding of the company as XT Group. Angel and Ofer hold equal shares in the company.

Current Roles and Holdings

Today, Angel serves as the Active Chairman of XT Holdings and Chairman of the group’s various subsidiaries. The group’s primary operations are in shipping, real estate, and high-tech.

His primary holdings include:

50% ownership of Ofer Ship Holding (through which he shares ownership of Ofer Shipping and Ofer Hi-Tech with the Sami Ofer family).

4.6% stake in Israel Corporation.

English

UnderTheBalanceSheet 리트윗함

The new number for $ZIM is $4.2 billion🚀

Dmitriy Kozin 🇺🇲🛢️⚓@dmiko789

Over $4B? " $Zim’s board of directors approved on Sunday evening the sale of the company to German shipping giant Hapag-Lloyd and the FIMI fund, Calcalist has learned...Hapag-Lloyd will acquire Zim in a deal valued at more than $4 billion." calcalistech.com/ctechnews/arti…

English

UnderTheBalanceSheet 리트윗함

אני אוהב להיות זהיר וכשיש ספק לגבי מספר תמיד בוחר ברף התחתון. גם בצים היה כך אתמול, אבל מתברר שהפעם הייתי זהיר מדי והמחיר הסופי יהיה כ-4.2 מיליארד דולר.

העיסקה אושרה הערב בדירקטוריונים של שתי החברות. מחר ימשך המו״מ מול העובדים, ייחתם הסכם, ואז אישורים

calcalist.co.il/market/article…

עברית

UnderTheBalanceSheet 리트윗함

UnderTheBalanceSheet 리트윗함

As a reminder: $ZIM has by far the highest share of LNG vessels in their fleet (currently 40%) which brings competitive advantages.

$ZIM invested pretty early into LNG and at very cheap long term charter rates (up to 12yrs) with buying options.

spglobal.com/market-intelli…

InvestyMan@InvestyMan

@Chuckyb22074706 Your chart does not include LNG - which is impacted as well by EU ETS. Here is a better overview: spglobal.com/energy/en/news… $ZIM is having overall cost advantages. And will continue to benefit from it also in the future: safety4sea.com/zim-signs-2-3-…

English

UnderTheBalanceSheet 리트윗함

EU VLSFO last week was $464/mt while 2026 ramp-up of EU-ETS(emission costs) fees/added costs this week went from $220/mt to $319/mt; nearly 50% incr. $ZIM fleet is way ahead of the curve on LNG.

shipandbunker.com/news/emea/7537… #shipandbunker

English

$ZIM

Which values are we talking about here? And which people? Are you referring to Oren Kaspi, the union chairman?

Only three days before they start a strike? Are you actually encouraging them?

Glickman, your conduct is absolutely disgraceful. I’ve never seen anything like this in any other company. It is time to put an end to it.

Eli Glickman@eli_glickman

As we enter the new year, I look back with pride at how ZIM navigated global uncertainty and industry challenges, standing strong with our #ZFactor in action. Looking ahead, we're guided by a strong strategy, clear values, and the people who make it all possible.

English

$ZIM

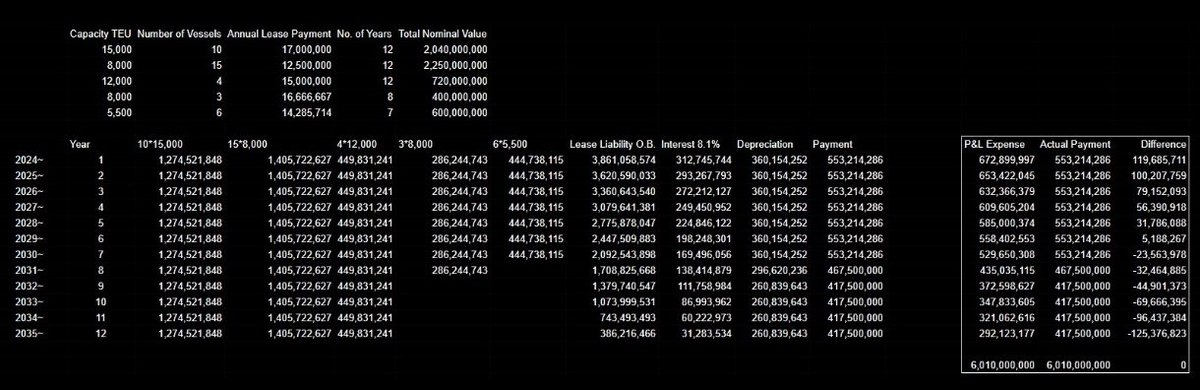

While the calculation relies on simplified assumptions and is not precise, the actual figures do not differ materially. The objective is to illustrate the distortions created by IFRS 16 in long-term lease transactions.

When such leases are capitalized using a relatively high discount rate, the income statement in the early years reflects an expense that is materially higher than the actual cash payment.

Conversely, in the later years, the cash payment exceeds the recognized expense.

In addition to the figures presented, three factors contribute to cash flow exceeding reported profit:

1. Vessels with variable or step-up charter rates: Actual cash payments in those years are lower than the expense recognized on a straight-line basis.

2. Down payments: These total approximately $490 million, creating an annual non-cash depreciation expense of roughly $40 million.

3. 13-year container leases: Similarly, the P&L expense exceeds the actual cash outflow in the initial years of the lease.

English

$ZIM operates across five distinct Geographic Trade Zones:

- Pacific

- Cross-Suez

- Atlantic-Europe

- Intra-Asia

- Latin America

ZIM calls at over 300 ports in more than 100 countries. Given that ZIM accounts for 2%–2.5% of global market share, its Israeli operations represent only a minor fraction of its total global activity.

While ZIM’s routes pass through Israel only within two specific zones, Cross-Suez and Atlantic-Europe it should be noted that a substantial portion of the activity within these zones does not involve Israel at all.

The company does not disclose the specific percentage of volume or revenue originating from, or passing through, Israeli ports within these segments.

Trade Zone Definitions:

Cross-Suez: Covers all major international shipping ports in the East Mediterranean, the Black Sea, China, East and Southeast Asia, and India.

Atlantic-Europe: Covers major international shipping ports in the East and West Mediterranean, the Black Sea, Northern Europe, the Caribbean, the Gulf of Mexico, and the East and West coasts of North America.

Attached Data:

- Percentage of total TEUs carried for the period.

- Percentage of total freight revenues from containerized cargo.

It is difficult to ignore the potential conflict of interest and the suspicion of financial arrangements between the management team whose MBO proposal was rejected and the union.

English

UnderTheBalanceSheet 리트윗함

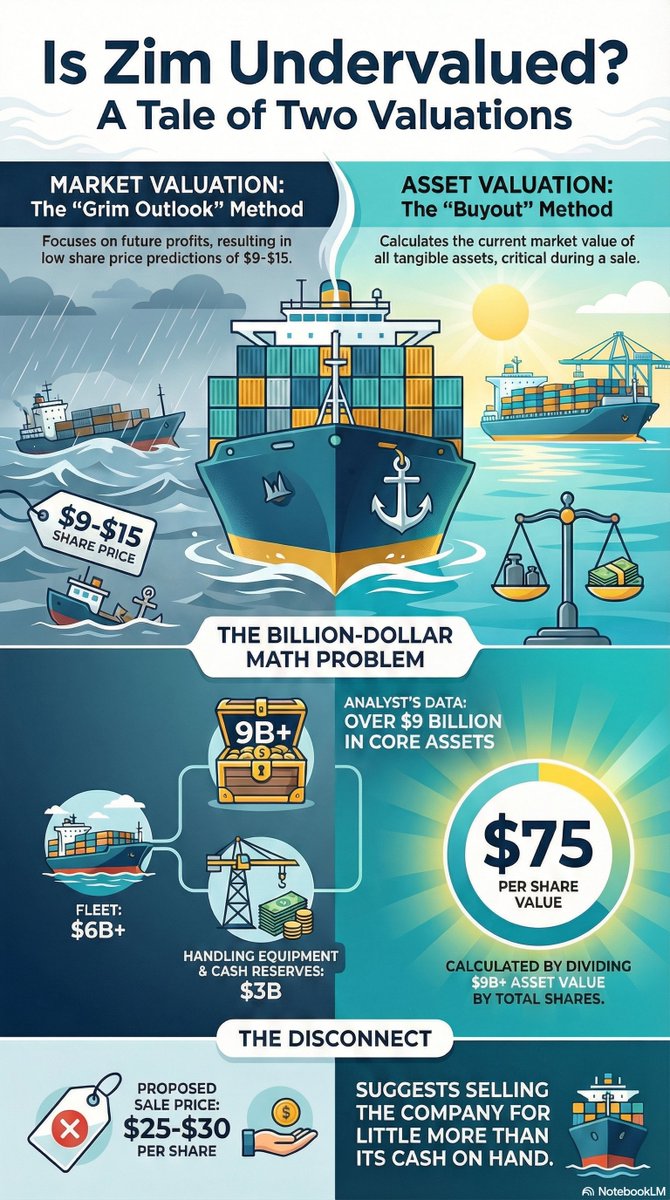

$ZIM Buyout or No Buyout - same same

$ZIM can be sold whole or in pieces. Either way, the key point is that the board finally appears aligned with shareholders—and the market still isn’t pricing that in.

Most activists I’ve spoken with actually prefer selling parts rather than the entire company. Why? Because instead of selling the whole business for, say, $30 only for the buyer to later unlock $70 of asset value-the board can do that unlocking itself.

In that scenario, $30 isn’t the exit price. It’s just the starting point.

Dmitriy Kozin 🇺🇲🛢️⚓@dmiko789

"The two new directors are expected to join the board only after the sale process concludes, which may explain why the existing board, led by Seroussi, ultimately did not object to their appointment." $ZIM 🤔

English

To clarify, we are referring to two distinct categories of assets under the 'Containers' heading:

1. The Q3/2023 Acquisition: A $1B transaction executed in the third quarter of 2023 (as referenced in the attached conference call transcript).

2. Fully Depreciated Assets: A separate and additional fleet of containers that have already been written down to zero on the balance sheet.

English

@UnderTheBalance Thanks I couldn’t find the container purchase in press releases. Where did you see it was depreciated to 0??! That’s not normal accounting for just two years of large asset capital?

English

$ZIM

Attention should be drawn to the strategic timing of the container acquisitions, which took place during an industry downturn when prices were at their lowest.

Furthermore, the acquisition itself was executed as an opportunistic transaction.

Notably, the company has omitted any mention of the containers' substantial fair market value, which significantly exceeds their current book value.

Certain containers have already been fully depreciated to zero. Consequently, regarding the $1B transaction, the company holds assets with a market value vastly superior to their recorded carrying amount.

English

$ZIM

Seaspan options to purchase:

15,000 TEU: Signed February 2021

7,700 TEU: Signed July 2021

What are the option terms and the hidden value they represent?

Which other vessels have purchase options, and under what conditions?

These options are recorded at zero book value.

English