Titus 𝕏 리트윗함

Titus 𝕏

5.3K posts

Titus 𝕏

@beamtitus

📍BKK-LOS ANGELES 🎓 USC Marshall’18 | Northwestern CU Law 💼 Financial | Tech | Equity Investor | Law

Los Angeles, CA 가입일 Aralık 2009

133 팔로잉620 팔로워

Howard Marks-Style Breakdown: How to Think About Markets 🧠📊

Investing is not about predicting the future perfectly. Nobody can do that. A better way is to understand what is happening right now.

Howard Marks calls this taking the temperature of the market. Is the market too hot? Is everyone too optimistic? Or is the market cold, fearful, and cheap? That question matters more than trying to guess the exact future.

1. Do Not Forecast Too Much 🔮❌

The future is uncertain. Even smart investors cannot know exactly what will happen next.

But we can look at today and ask:

Is the market expensive?

Are people too confident?

Are investors ignoring risk?

Are prices already too high?

This is more useful than saying, “The market will crash next month.”

A market can be overpriced and still keep going up. That is why timing is hard. 📈🔥

2. Market Temperature Matters 🌡️

When the market is hot, people become very optimistic.

They say things like:

“This time is different.”

“This technology will change everything.”

“Valuation does not matter anymore.”

“Everyone will get rich.”

That is usually dangerous. 🚨

When the market is cold, people are fearful. Prices are lower. Investors are pessimistic. That is often when better opportunities appear.

Simple rule:

Buy more carefully when people are excited.

Look more closely when people are scared.

3. A Great Story Is Not Always a Great Investment 🚀⚠️

New technology can be real and still become a bad investment.

The internet changed the world, but many internet companies from the dot-com bubble failed. Why? Because they had bad business models, weak revenue, or no profit.

The same idea can apply to AI, crypto, SaaS, SPACs, or any new hot theme.

A story can be powerful.

A product can be revolutionary.

But investors still need to ask:

Can this business make money?

Is the price reasonable?

Is the valuation too high?

Is the company strong enough to survive?

A great future does not automatically mean a great stock price. 💰

4. Price Matters More Than Popularity 💵

One of the biggest lessons is:

It is not only what you buy.

It is what you pay.

A great company can be a bad investment if you pay too much.

A disliked asset can be a good investment if the price is low enough.

This is why intelligent investors do not just chase quality. They compare quality vs. price.

Good investing is not buying what everyone loves.

Good investing is buying something at a price that gives you a margin of safety. 🛡️

5. Emotion Is the Investor’s Enemy 😨📉

Most people do the wrong thing at the wrong time.

When prices go up, they feel safe and buy more.

When prices go down, they feel afraid and sell.

But this often means they buy high and sell low.

The best investors try to do the opposite:

They become careful when others are greedy.

They become open-minded when others are fearful.

That sounds simple, but it is hard because emotions are powerful. 🧘♂️

6. Being Different Is Uncomfortable 🧍♂️

To outperform, you cannot always think like the crowd.

If everyone owns the same popular stocks, it is hard to get a different result.

Sometimes the best opportunities are in areas that people dislike, ignore, or misunderstand.

But being different is uncomfortable. People may think you are wrong. You may look foolish for a while.

That is why successful investing requires courage, patience, and discipline. 💪

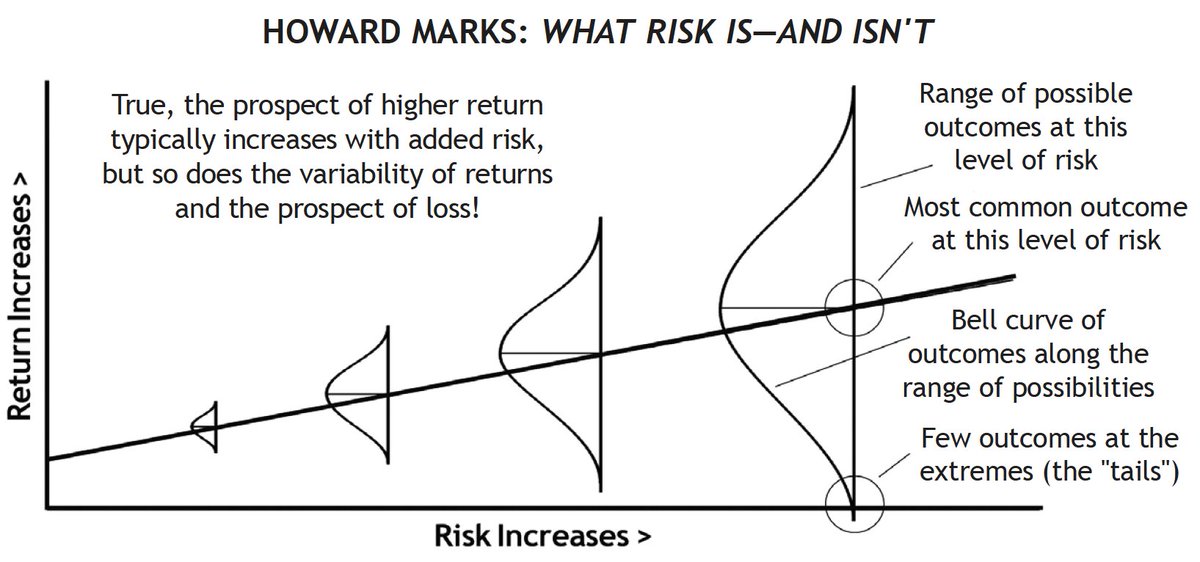

7. Risk Cannot Be Fully Measured 📊⚠️

Numbers are helpful, but they do not tell the full story.

Risk is about what bad things could happen in the future. The problem is that the future cannot be measured perfectly.

A model can show past volatility.

A chart can show past drawdowns.

A spreadsheet can show assumptions.

But risk often appears when the past stops working.

That is why investors need judgment, not just data. 🧠

8. Survival Comes First 🛡️

The goal is not to win every year.

The goal is to survive long enough to compound.

An investor who avoids big disasters can do very well over time. You do not need to hit home runs every year. You need to avoid getting destroyed.

Howard Marks’ style is more about cutting off the downside than chasing the biggest upside.

Simple idea:

Avoid the losers, and the winners can take care of themselves. ⚾📈

9. Humility Is a Superpower 🙏

Good investors know they can be wrong.

Confidence is important, but overconfidence is dangerous.

If you have no confidence, you will panic every time prices fall.

If you have too much confidence, you may double down on a bad idea.

The right balance is:

Confidence, but not arrogance.

Humility, but not fear.

This helps investors stay calm and make better decisions. ⚖️

10. AI and Data Help, But They Are Not Enough 🤖

Today, investors have more data than ever. AI can analyze information very fast.

That is useful.

But if everyone has the same data, the data alone is not enough to create an edge.

The real edge comes from judgment:

Understanding market psychology

Understanding business quality

Understanding valuation

Understanding risk

Understanding what others may be missing

AI can process numbers. But investors still need wisdom. 🧠✨

Final Takeaway 💡

The best investors do not pretend they know the future.

They study the present.

They watch market psychology.

They respect valuation.

They control emotion.

They avoid big mistakes.

They stay humble.

In simple words:

Do not chase every hot story.

Do not panic during every scary moment.

Pay attention to price.

Respect risk.

Survive first.

That is the Howard Marks way. 📚📈

English

The Risk Curve: From Safety to Speculation 📊⚖️

Every asset sits somewhere on the risk curve.

At the low-risk end, investors mainly look for safety, liquidity, and capital preservation. 🛡️💵

At the high-risk end, investors chase higher returns, but must accept deeper drawdowns, higher volatility, and more uncertainty. 🚀📉

A simple risk curve looks like this:

💵 Cash

→ 🧾 T-Bills

→ 🇺🇸 US 2Y Treasury

→ 🇺🇸 US 5Y Treasury

→ 🇺🇸 US 10Y Treasury

→ 🇺🇸 US 15Y / 20Y / 30Y Treasury

→ 🏦 Investment Grade Bonds

→ ⚠️ High Yield Bonds

→ 📈 S&P 500

→ 🏡 Real Estate / Land / REITs

→ 🟡 Gold

→ ⚪ Silver

→ 🏭 Platinum / Palladium

→ 🌍 Emerging Markets

→ 🚀 Small Caps / Growth Tech

→ 🧠 Private Equity / VC

→ ₿ Bitcoin

→ 🎰 Altcoins / Meme Coins

The key lesson: 🧠

💵 Cash protects liquidity.

🏦 Bonds protect capital.

📈 Stocks grow capital.

🏡 Real estate stores wealth.

🟡 Gold hedges uncertainty.

⚪ Silver and industrial metals add cyclical exposure.

₿ Bitcoin adds asymmetric upside.

🎰 Altcoins add maximum speculation.

The mistake many investors make is treating all “risk assets” the same. ⚠️

They are not the same.

📈 The S&P 500 is risky, but it is not the same type of risk as Bitcoin.

₿ Bitcoin is risky, but it is not the same type of risk as a meme coin.

🟡 Gold is volatile, but it is not the same type of risk as high-growth tech.

🇺🇸 A 30-year Treasury is safer than stocks, but it can still fall hard when yields rise.

Risk is not one thing. 🧩

There is:

📉 Interest rate risk

🏦 Credit risk

💧 Liquidity risk

🔥 Inflation risk

📊 Valuation risk

🌍 Currency risk

⚖️ Regulatory risk

🧠 Narrative risk

🎰 Speculation risk

Understanding where each asset sits on the curve helps investors build better portfolios. 🧱📊

In a strong liquidity cycle, money usually moves outward: 🌊🚀

💵 Cash → 🏦 Bonds → 📈 Stocks → 🚀 Growth → ₿ Crypto

In a fear cycle, money often moves backward: 🧊📉

₿ Crypto → 🚀 Growth → 📈 Stocks → 🏦 Bonds → 💵 Cash

That is why the risk curve matters. 🎯

It helps explain market rotation, investor behavior, and why certain assets outperform during different macro environments. 🌍📊

The real question is not:

“Which asset is best?” ❌

The better question is:

“Where are we in the liquidity cycle, and how much risk should I take right now?” ✅

English

The bond market is flashing a warning sign for the S&P 500 ⚠️📉

The U.S. 30-year Treasury yield is around 5.18%, the highest level since 2007.

This is important because Treasury yields are like the “base price of money” for the whole economy.

When yields rise, stocks usually face more pressure.

Here is why:

1️⃣ Safe bonds become stronger competition

If investors can earn around 5% from U.S. government bonds, they may ask:

“Why should I take extra risk in stocks?”

That makes expensive stocks less attractive.

2️⃣ Higher yields lower stock valuations

Stock prices are based on future earnings.

But when interest rates rise, those future earnings are worth less today.

Simple idea:

Higher yields = lower valuation multiples

This can hurt growth stocks the most, especially tech and AI companies, because much of their value depends on future profits.

3️⃣ Borrowing costs increase

Higher Treasury yields can push up:

🏠 Mortgage rates

🚗 Auto loan rates

💳 Credit card rates

🏢 Business loan rates

When borrowing becomes more expensive, consumers may spend less and companies may invest less.

That can slow earnings growth.

4️⃣ Company profits can be pressured

Companies with debt may need to refinance at higher rates.

That means higher interest expense and lower profit margins.

If earnings slow while the S&P 500 is still expensive, the market becomes more vulnerable.

5️⃣ The Fed may have less room to cut

If yields are rising because investors fear inflation, the Federal Reserve may not be able to cut rates quickly.

That removes one major support for stocks: cheaper money.

Simple takeaway:

The S&P 500 is not just facing one problem.

It is facing higher borrowing costs, stronger bond competition, valuation pressure, and inflation risk at the same time.

This does not mean the market must crash.

But it does mean the margin of safety is smaller.

When the 30-year Treasury yield is above 5%, the stock market needs real earnings growth — not just optimism — to justify high prices.

English

🏦📈 Why Cutting Interest Rates Too Early Can Create Bigger Inflation Later

Rate cuts feel good at first.

They make money cheaper.

They help stocks.

They help housing.

They help businesses borrow.

They make people feel richer. 📈

But if inflation is not fully solved, cutting rates too early can create a bigger problem later. ⚠️

━━━━━━━━━━━━━━

1. Cheap money increases demand 💸

━━━━━━━━━━━━━━

When rates go down:

🏠 More people buy houses

🚗 More people finance cars

🏢 Companies borrow more

📈 Investors take more risk

🛒 Consumers spend more

This can restart demand.

If supply cannot keep up, prices rise again.

Simple idea:

More money chasing limited goods = inflation pressure 🔥

━━━━━━━━━━━━━━

2. Inflation expectations can come back 🧠

━━━━━━━━━━━━━━

Inflation is not only about prices today.

It is also about what people expect tomorrow.

If people think the Fed will cut too early, they may expect inflation to stay high.

Then:

👷 Workers ask for higher wages

🏢 Companies raise prices early

🏠 Sellers demand higher prices

📈 Investors buy inflation hedges

This can make inflation harder to kill.

━━━━━━━━━━━━━━

3. The 1970s lesson 📚

━━━━━━━━━━━━━━

The 1970s are the classic warning.

The Fed tightened, then eased when unemployment rose.

But inflation was not fully defeated.

So inflation came back again.

Later, Paul Volcker had to raise rates much more aggressively to restore credibility. 🏦⚔️

That caused pain, but it finally broke inflation psychology.

Lesson:

Small cuts too early can force bigger hikes later.

━━━━━━━━━━━━━━

4. Asset bubbles can form 📈

━━━━━━━━━━━━━━

Low rates push investors into riskier assets.

That can inflate:

🏠 Housing

📊 Stocks

🪙 Crypto

🏢 Commercial real estate

🚗 Car prices

💳 Consumer credit

At first, it feels like wealth.

But if prices rise faster than income, the economy becomes fragile.

Then the Fed may need to tighten again.

━━━━━━━━━━━━━━

5. Currency can weaken 💵

━━━━━━━━━━━━━━

If a central bank cuts too early while inflation is still high, the currency can weaken.

A weaker currency can make imports more expensive:

⛽ Oil

🍱 Food

🚗 Cars

📱 Electronics

🏭 Industrial goods

That can push inflation higher again.

━━━━━━━━━━━━━━

6. Why rates may need to go even higher later 📈

━━━━━━━━━━━━━━

If inflation returns, the Fed has to rebuild trust.

That may require:

📈 Higher rates

⏳ Keeping rates high longer

🧊 Tighter credit

📉 Slower growth

💼 Higher unemployment risk

The longer inflation survives, the harder it is to remove.

Inflation is like fire. 🔥

If you stop fighting too early, it can spread again.

Then you need more water later.

━━━━━━━━━━━━━━

Simple summary 🧠

━━━━━━━━━━━━━━

Rate cuts are helpful when the economy is weak.

But if rates are cut before inflation is truly controlled, it can create:

🔥 More demand

💵 Weaker currency

📈 Asset bubbles

🧠 Higher inflation expectations

💳 More debt

🏦 Bigger rate hikes later

The pattern from history is simple:

Easy money feels good first.

But if it creates inflation again, the next tightening cycle can be much more painful.

That is why central banks fear cutting too early.

They do not only worry about today’s economy.

They worry about losing inflation credibility for years. 🏦📊

Sources: Federal Reserve History, Bank of England long-run data, CBO, Brooking

English

💻📉 Dot-Com Lesson: 48% Survived 5 Years, But Maybe Only ~1% Became True Long-Term Winners

This is the investing lesson from the dot-com bubble:

The technology was real.

But most stocks were still bad investments. ⚠️

The internet changed the world.

But that did not mean every internet company became Amazon.

━━━━━━━━━━━━━━

1. Survival ≠ good investment 🧊

━━━━━━━━━━━━━━

Some dot-com companies survived.

But many survived at much lower prices.

Some became tiny.

Some were bought out.

Some diluted shareholders.

Some never returned to old highs.

For investors, “the company survived” is not enough.

The real question is:

Did the stock create wealth? 💰

━━━━━━━━━━━━━━

2. The index survived, but investors waited years 📉

━━━━━━━━━━━━━━

The Nasdaq survived.

But after the 2000 peak, it crashed about 77%.

It took around 15 years for Nasdaq to reclaim the dot-com high.

That means even if you bought the “right trend,” timing and valuation still mattered.

Real technology + bad price = bad investment.

━━━━━━━━━━━━━━

3. Most companies were not real winners 🔥

━━━━━━━━━━━━━━

Many dot-com companies had:

🚫 no profit

🚫 weak cash flow

🚫 high cash burn

🚫 expensive marketing

🚫 no moat

🚫 unrealistic valuation

They were selling dreams, not durable businesses.

When easy money disappeared, weak companies broke fast.

━━━━━━━━━━━━━━

4. Winners were rare 🏆

━━━━━━━━━━━━━━

A few companies became legendary:

✅ Amazon

✅ eBay

✅ Priceline / Booking

✅ Google later became dominant after the bubble period

But these were the exception.

Most investors did not own only the winners.

They owned the hype basket.

And the hype basket got destroyed. 📉

━━━━━━━━━━━━━━

5. Lesson for AI, crypto, EVs, and tech today 🤖

━━━━━━━━━━━━━━

A big trend can be real, but most stocks can still fail.

AI can be real.

EVs can be real.

Crypto can be real.

Robotics can be real.

But that does not mean every company wins.

Ask:

✅ Does it have profit?

✅ Does it have cash flow?

✅ Does it have a real moat?

✅ Can it survive high rates?

✅ Is valuation reasonable?

✅ Is it a leader or just hype?

━━━━━━━━━━━━━━

Simple summary 🧠

━━━━━━━━━━━━━━

The dot-com bubble teaches one big lesson:

Technology trend ≠ guaranteed stock return.

Maybe many companies survive legally.

But only a tiny minority become true long-term winners.

For investors, the goal is not to buy the trend.

The goal is to buy the few companies that can survive, dominate, and compound for decades. 🚀

The internet was real.

But most dot-com stocks were not great investments. 💻📉

Sources: University of Maryland dot-com survival research, Goldman Sachs, Nasdaq market history

English

🤖💸 Why AI Is Making Real Life More Expensive

AI is supposed to make life cheaper.

Maybe one day it will.

But right now, AI is also pushing real-world costs up. 📈

Why?

Because AI is not just software.

AI needs:

⚡ Electricity

🏢 Data centers

💻 Chips

🔋 Power grids

🌊 Water cooling

👷 Skilled workers

🏗️ Construction

💵 Huge investment

━━━━━━━━━━━━━━

1. AI uses huge electricity ⚡

━━━━━━━━━━━━━━

AI data centers need massive power.

Training and running AI models requires thousands of expensive chips working nonstop.

That means more electricity demand.

More demand can push up:

🏠 Home power bills

🏢 Business utility costs

🏭 Industrial energy costs

🏗️ Grid upgrade costs

More AI = more data centers

More demand = more pressure on power prices ⚡📈

━━━━━━━━━━━━━━

2. AI needs expensive chips 💻

━━━━━━━━━━━━━━

AI depends on advanced GPUs and memory chips.

When big tech companies all buy chips at the same time, supply gets tight.

That can make chips, servers, cloud computing, laptops, phones, and electronics more expensive. 💻📱

AI feels digital, but it runs on physical hardware.

━━━━━━━━━━━━━━

3. AI raises cloud and software costs ☁️

━━━━━━━━━━━━━━

Many apps now add AI features.

Then companies say:

“Now this product has AI, so the price is higher.” 🤖💳

This can happen with:

📄 Office software

🎨 Design tools

📊 Business apps

📚 Education apps

🧾 Accounting tools

📧 Email tools

Sometimes AI adds value.

But sometimes it becomes an excuse for subscription price hikes.

━━━━━━━━━━━━━━

4. AI increases demand for skilled workers 👨💻

━━━━━━━━━━━━━━

AI needs people who can build, manage, and use it.

That increases demand for:

🤖 AI engineers

📊 Data scientists

🔐 Cybersecurity workers

☁️ Cloud engineers

⚡ Energy engineers

🏗️ Data-center builders

When demand rises, wages can rise too.

That cost often gets passed to customers.

━━━━━━━━━━━━━━

5. AI pushes up land and infrastructure 🏗️

━━━━━━━━━━━━━━

Data centers need land, power lines, cooling, backup generators, fiber internet, and construction materials.

That can pressure:

🏞️ Land prices

🏗️ Construction costs

⚡ Power grid spending

🌊 Water resources

🏘️ Local infrastructure

So AI can make some local areas more expensive.

━━━━━━━━━━━━━━

6. Companies must recover huge AI spending 💵

━━━━━━━━━━━━━━

Big tech companies are spending hundreds of billions on AI infrastructure.

Eventually, they want a return.

That means companies may raise prices on:

☁️ Cloud services

💻 Software subscriptions

📱 Apps

📊 Business tools

🎮 Digital services

🛒 Online platforms

If AI costs companies more, customers may pay more.

━━━━━━━━━━━━━━

7. AI can reduce jobs, but not always prices 🧠

━━━━━━━━━━━━━━

Some people think:

“If AI replaces workers, prices should fall.”

Sometimes yes.

But not always.

Companies may use AI to increase profit margins instead of lowering prices.

AI may raise demand for high-skill jobs while reducing some lower-skill jobs.

That can make life feel more expensive for many people.

━━━━━━━━━━━━━━

Simple summary 🧠

━━━━━━━━━━━━━━

AI can make life more expensive because it increases demand for:

⚡ Electricity

💻 Chips

☁️ Cloud computing

👨💻 Skilled workers

🏗️ Data centers

🔋 Power grids

💳 Software subscriptions

AI is not “free magic.”

It is a giant new industry that needs massive energy, hardware, land, workers, and money.

Long term, AI may make some things cheaper. 🚀

But short term, the AI boom can push costs higher.

AI may be digital on your screen…

but it is expensive in the real world. 🤖💸

Sources: IEA, Goldman Sachs, Reuters, World Economic Forum

English

Titus 𝕏 리트윗함

🚨 SOMEONE JUST KILLED THE REAL ESTATE INDUSTRY

A guy scanned an entire house with his phone. Uploaded it.

Now anyone on Earth can walk through it in a browser tab. No app. No VR. No agent. No appointment.

Click → you’re inside. Every room. Every angle. Every shadow. Photoreal.

The numbers are insane:

- Agent fee on a $500k home: $15,000

- Cost to make this scan: ~$200

- Time to “tour” 50 houses: one evening

- File size: smaller than a TikTok

The science is wild too:

It’s called 3D Gaussian Splatting instead of polygons (how games render), it uses millions of tiny glowing “splats” of color and depth.

AI reconstructs reality from your photos. The result loads on a phone and looks like you’re THERE.

The grift opportunity is even wilder:

Freelancers are already charging $300–$800 per scan for realtors, Airbnbs, venues, car dealers, museums.

One person + one phone + one weekend = a business.

100% Open source. Built on PlayCanvas.

English

🎓📉 Why a Pricey College Degree May Not Be Worth It in the Next Decade

College is not useless.

A good degree in the right field can still change someone’s life. Doctors, nurses, engineers, accountants, lawyers, teachers, and many technical workers still need formal education. ✅

But the problem is the price.

A college degree used to be a simple rule:

🎓 Get degree

💼 Get good job

🏠 Buy home

💰 Build wealth

Now that path is less guaranteed.

━━━━━━━━━━━━━━

1. College became too expensive 💸

━━━━━━━━━━━━━━

Many students pay huge tuition, housing, books, fees, and living costs before they even earn real money.

Even if the degree is good, the debt can make life harder.

A degree is an investment.

But if the price is too high, the return can be weak. 📉

━━━━━━━━━━━━━━

2. Not all degrees pay the same 💼

━━━━━━━━━━━━━━

A nursing degree and a low-demand degree are not the same investment.

Some degrees lead to strong jobs.

Some degrees lead to low pay, unstable work, or jobs that do not require a degree.

The question should not be:

“Should I go to college?”

The better question is:

“What job will this degree realistically lead to?” 🤔

━━━━━━━━━━━━━━

3. AI may hurt entry-level office jobs 🤖

━━━━━━━━━━━━━━

The next decade may be harder for basic white-collar jobs.

AI can already help with:

📝 Writing

📊 Reports

📧 Emails

💻 Coding basics

📞 Customer service

📂 Admin work

🔍 Research

These were often entry-level jobs for college graduates.

If AI reduces beginner jobs, new graduates may struggle to get experience.

That makes expensive degrees riskier.

━━━━━━━━━━━━━━

4. Skills are becoming more important than the paper 📚

━━━━━━━━━━━━━━

Employers still care about degrees.

But they increasingly care about proof of skill:

💻 Can you code?

📊 Can you analyze data?

🧰 Can you fix things?

🗣️ Can you sell?

🏥 Can you do clinical work?

🤖 Can you use AI tools?

📁 Can you show projects?

In the future, a degree without useful skills may not be enough.

━━━━━━━━━━━━━━

5. Opportunity cost matters ⏳

━━━━━━━━━━━━━━

College is not only tuition.

It also costs time.

Four years in college can mean four years not earning full-time income.

For some careers, that trade is worth it.

For others, a cheaper path may be better:

🧰 Trade school

🏥 Healthcare certificate

💻 Coding / IT certificate

🚗 Apprenticeship

🏢 Community college

📊 Portfolio-based skills

💼 Starting work earlier

The best path is not always the most expensive one.

━━━━━━━━━━━━━━

6. Debt delays adult life 🏠

━━━━━━━━━━━━━━

Student debt can delay:

🏠 Buying a home

🚗 Buying a car

👶 Starting a family

💰 Saving money

📈 Investing

🏢 Starting a business

If the degree leads to high income, debt may be manageable.

But if the income is low, debt becomes a heavy backpack. 🎒

━━━━━━━━━━━━━━

Simple summary 🧠

━━━━━━━━━━━━━━

A pricey college degree may not be worth it if:

🚨 Tuition is too high

🚨 Debt is too large

🚨 The major has weak job demand

🚨 Starting salary is low

🚨 AI may replace entry-level tasks

🚨 The school brand is not strong

🚨 The degree does not build real skills

College is still worth it when:

✅ The field has strong demand

✅ The salary can repay the cost

✅ The school is affordable

✅ The degree is required for the job

✅ The student builds real skills, internships, and projects

The future rule is simple:

Do not buy a degree only for status.

Buy education like an investment. 📊

Ask:

💰 What will it cost?

But overpriced degrees with weak job outcomes may become one of the worst financial decisions of the next decade. ⚠️

Sources: BLS, College Board, New York Fed, World Economic Forum

English

🥇📈 Why Gold Runs for Decades — Then Stops for Decades

Gold is not like stocks.

📈 Stocks can grow earnings

🏠 Real estate can collect rent

🏦 Bonds can pay interest

Gold does not produce cash flow.

Gold mainly rises when people lose trust in:

💵 Paper money

🔥 Inflation control

🏦 Banks

🌍 Governments

📉 Financial markets

━━━━━━━━━━━━━━

🚀 When gold runs

━━━━━━━━━━━━━━

Gold usually becomes strong when:

🔥 Inflation is high

💵 Currency feels weak

🏦 Banks look risky

🌍 War/geopolitics increase

💰 Government debt rises

📉 Real interest rates are low or negative

🖨️ Money printing fears grow

Simple idea:

When people fear the system, gold wakes up. 🥇

━━━━━━━━━━━━━━

🧊 When gold stops

━━━━━━━━━━━━━━

Gold can stop rising for many years when:

📈 Real interest rates are high

💵 Dollar is strong

📊 Stocks perform well

📉 Inflation is low

🏦 People trust central banks

😴 Crisis fear fades

Then investors prefer stocks, bonds, or cash because they can earn returns.

Gold becomes boring.

━━━━━━━━━━━━━━

🧠 Simple summary

━━━━━━━━━━━━━━

Gold moves in long macro cycles.

1970s: inflation + dollar fear = gold boom 🚀

1980s–1990s: high rates + strong dollar = gold slept 🧊

2000s: crisis + low rates = gold boom 🚀

2010s: stocks strong + low inflation = gold slowed 🧊

Gold runs when trust is low.

Gold sleeps when trust comes back. 🥇💤

English

🚗💸 What Matters Most When Buying a Car?

Many people only ask:

“Is the MPG good?” ⛽

“Should I buy EV?” 🔋

But the real cost of a car is bigger than gas.

The most important things are:

📉 Depreciation

🏦 Interest rate

🛠️ Reliability / repair cost

⛽ MPG or 🔋 charging cost

🚘 Insurance and registration

━━━━━━━━━━━━━━

📉 Depreciation is usually the biggest cost

━━━━━━━━━━━━━━

Depreciation means:

You buy the car for $40,000

Later it is worth $25,000

You lost $15,000 even if the car runs fine.

This is why a “cheap monthly payment” can still be dangerous.

Some cars lose value fast.

Some cars hold value well.

EVs can save money on fuel, but some EVs depreciate very fast because:

🔋 Battery technology changes

🏷️ New EV discounts hurt used prices

⚡ Charging network matters

🚘 More competition enters the market

💰 Tax credits affect resale value

So the real question is not only:

“Gas or EV?”

The better question is:

“How much value will this car lose?” 📉

━━━━━━━━━━━━━━

2. 🏦 Interest rate can quietly destroy the deal

━━━━━━━━━━━━━━

A good car at a bad interest rate can become a bad deal.

High interest makes you pay more every month and more total money over time.

Example:

🚗 Car price looks okay

🏦 But APR is high

📆 Loan term is long

💸 Total cost becomes expensive

Used-car loans often have higher rates than new-car loans.

Long loans like 72 or 84 months can lower the monthly payment, but increase total interest and negative-equity risk.

━━━━━━━━━━━━━━

3. ⛽ MPG matters, but not always the most

━━━━━━━━━━━━━━

MPG is important if you drive a lot.

If you drive delivery, commute far, or drive every day, MPG matters more. 🚗💨

But if you do not drive much, saving gas may not beat:

📉 Depreciation

🏦 Interest

🛠️ Repairs

🚘 Insurance

Example:

Saving $800/year on gas is good.

But if the car loses $5,000 more in resale value, the MPG savings did not really win.

━━━━━━━━━━━━━━

4. 🔋 EV cars can be great, but only for the right buyer

━━━━━━━━━━━━━━

EVs can be very good if:

✅ You charge at home

✅ Electricity is cheap

✅ You drive a lot

✅ You keep the car long-term

✅ Insurance is reasonable

✅ Depreciation is already priced in

A used EV can be a great deal because the first owner already took the big depreciation hit.

But a new EV can be risky if the price drops fast after you buy.

EV is not automatically good or bad.

It depends on:

🔋 Purchase price

⚡ Charging cost

📉 Depreciation

🚘 Insurance

🛠️ Repair risk

📆 How long you keep it

━━━━━━━━━━━━━━

5. 🧠 Simple ranking

━━━━━━━━━━━━━━

If I rank importance for most buyers:

📉 Depreciation

🏦 Interest rate / loan terms

🛠️ Reliability and repair cost

🚘 Insurance cost

⛽ MPG or 🔋 charging cost

🏷️ Purchase price

😍 Looks / features

Why?

Because MPG saves money slowly.

But depreciation and interest can cost thousands quickly.

━━━━━━━━━━━━━━

Simple summary 🚗

━━━━━━━━━━━━━━

Do not buy a car only because it has good MPG.

Do not buy an EV only because electricity is cheaper.

The best car is the one with the lowest total cost:

📉 Holds value well

🏦 Has low interest rate

🛠️ Reliable

🚘 Affordable insurance

⛽ Good MPG or cheap charging

📆 Fits how long you will keep it

For most people, the biggest mistake is not bad MPG.

The biggest mistake is buying a car that depreciates fast with a high-interest long loan.

That is how people become upside down. 🚨

Best rule:

Buy the car based on total cost, not just gas savings. 🧠🚗💰

Sources: iSeeCars, Experian, Edmunds, AAA

English

🚗📉 Why Car Depreciation Is Usually More Important Than Interest Rates

Most people focus too much on the interest rate.

They ask:

“Is the APR 5%, 7%, or 9%?” 🏦

That matters.

But in most cases, the bigger money leak is depreciation.

Depreciation means your car loses value over time.

You buy a car for $40,000.

A few years later, it may be worth $24,000.

That is a $16,000 loss. 📉

━━━━━━━━━━━━━━

Interest is visible 👀

━━━━━━━━━━━━━━

Interest is easy to see.

The bank shows:

💳 APR

📆 monthly payment

⏳ loan term

💰 total interest

Because it is written clearly, buyers worry about it.

But depreciation is quiet.

The dealer does not show you:

“This car may lose $15,000–$25,000 in value.”

So many people ignore it.

━━━━━━━━━━━━━━

2. Depreciation is usually bigger 💸

━━━━━━━━━━━━━━

Example:

🚗 Car price: $40,000

🏦 Loan: 60 months

📈 Interest rate: 7%

💰 Total interest: about $7,500

That sounds painful.

But if the car loses 40% value in 5 years:

📉 Depreciation loss: about $16,000

So depreciation can be more than double the interest cost.

That is why resale value matters so much.

━━━━━━━━━━━━━━

3. A cheap payment can hide a bad deal ⚠️

━━━━━━━━━━━━━━

A dealer may make the monthly payment look low by using:

📆 longer loan term

💰 small down payment

🎁 rebates

📉 low APR promotion

But if the car depreciates fast, you still lose money.

Low payment does not always mean low cost.

The real cost is:

Purchase price

interest

insurance

maintenance

resale value

━━━━━━━━━━━━━━

4. Some cars lose value faster 🚨

━━━━━━━━━━━━━━

Two cars can have the same price and same interest rate.

But one may hold value much better.

Example:

Car A loses 25%

Car B loses 50%

Even with the same APR, Car B is much more expensive long term.

Fast depreciation usually hits:

🚘 luxury cars

🔋 some EVs

🏷️ unpopular brands

📉 cars with big discounts

🛠️ cars with reliability concerns

📦 cars with oversupply

Better resale usually comes from:

✅ reliability

✅ strong brand demand

✅ low repair fear

✅ good fuel economy

✅ limited supply

✅ popular body style

━━━━━━━━━━━━━━

5. Depreciation matters most if you sell early 🔁

━━━━━━━━━━━━━━

If you keep a car for 10–15 years, depreciation matters less each year.

But if you trade cars every 3–5 years, depreciation is huge.

That is when many people lose the most money.

The first owner often takes the biggest hit.

The second owner may get better value.

━━━━━━━━━━━━━━

6. Simple rule 🧠

━━━━━━━━━━━━━━

Interest rate is important.

But depreciation is often the bigger enemy.

A low-interest bad-resale car can cost more than a higher-interest good-resale car.

So before buying, ask:

📉 How fast does this car lose value?

🏷️ What is resale demand?

🛠️ Is the brand reliable?

🔁 Will I sell it in 3–5 years?

💰 What is the total cost, not just payment?

━━━━━━━━━━━━━━

Final summary 🚗

━━━━━━━━━━━━━━

APR affects your loan.

Depreciation affects your wealth.

Interest is the cost of borrowing money.

Depreciation is the cost of owning the wrong car.

In most cases, the best car deal is not the lowest monthly payment.

It is the car with:

✅ fair purchase price

✅ good reliability

✅ strong resale value

✅ reasonable insurance

✅ low repair risk

✅ slower depreciation

That is why depreciation is usually more important than interest rates. 🚗📉

Sources: AAA, Edmunds, iSeeCars, Federal Reserve

English

🪙🚀 Why the Next Crypto Cycle Could Have a Higher Chance of Altseason

This is not guaranteed.

But the next cycle may have a better chance of altseason than 2023–2025.

Why?

Because the last cycle was mostly Bitcoin-led.

The next cycle may have more conditions for money to rotate into altcoins. 🔁

━━━━━━━━━━━━━━

Bitcoin dominance is already high 🟠

━━━━━━━━━━━━━━

From 2023 to 2025, Bitcoin took most of the attention.

Bitcoin dominance rose strongly, helped by spot Bitcoin ETFs, institutional buying, and the “safer crypto” narrative after FTX. CoinGecko reported BTC dominance rising from 38.4% at the start of 2023 to about 58.5% in 2025. (CoinGecko)

When BTC dominance gets very high, the next important question becomes:

When does money rotate out of BTC into ETH and altcoins? 🔵🟣

That rotation is usually what creates altseason.

━━━━━━━━━━━━━━

2. Institutions already entered crypto 🏦

━━━━━━━━━━━━━━

Last cycle, institutions mainly bought Bitcoin.

Spot Bitcoin ETFs made BTC easier to buy through normal brokerage accounts. Chainalysis reported global Bitcoin ETF AUM reached about $179.5B by mid-July 2025. (Chainalysis)

This matters because the road is now built.

First, institutions bought BTC.

Then ETH ETFs launched.

Later, more crypto products may become easier to access.

The next cycle could have more institutional “rails” for capital to reach beyond Bitcoin.

━━━━━━━━━━━━━━

3. ETH and altcoin access improved 🔵

━━━━━━━━━━━━━━

In 2024, the SEC approved exchange applications for spot Ether ETFs, and Reuters reported the first U.S. spot Ether ETFs began trading in July 2024. (Reuters)

This is important because altseason usually needs ETH to wake up first.

Typical rotation:

BTC pumps 🟠

ETH follows 🔵

Large caps move 🟣

Mid caps move 🟢

Small caps explode 🔥

If ETH becomes stronger next cycle, altseason chances increase.

━━━━━━━━━━━━━━

4. Liquidity may improve later 💧

━━━━━━━━━━━━━━

Altcoins need liquidity.

High rates usually hurt speculation because safe assets already pay decent yield.

In 2023–2025, high rates made investors more careful. Even in 2026, Reuters reported brokerages were split on Fed cuts, with some expecting no cuts because inflation risks remained elevated. (Reuters)

But if the next cycle has:

✂️ lower rates

🛑 less QT

💧 more liquidity

📈 stronger risk appetite

Then altcoins could benefit more than Bitcoin.

Why?

Because altcoins are higher beta.

When liquidity comes back, money often moves from safer assets to riskier assets.

━━━━━━━━━━━━━━

5. Retail may return if prices move enough 🧍♂️📱

━━━━━━━━━━━━━━

Retail did not fully return in 2023–2025.

Many people were burned by:

📉 2022 crash

🏦 FTX

🐸 memecoin dumps

🔓 token unlocks

💸 high living costs

But retail usually comes back when the market becomes exciting again.

If BTC makes big gains first, people may start looking for “the next coin.”

That is when altcoins can attract attention again.

Crypto adoption also remains global. Chainalysis ranked India, the U.S., Pakistan, Vietnam, and Brazil among the top countries for crypto adoption in 2025. (Chainalysis)

━━━━━━━━━━━━━━

6. New narratives are stronger than before 🤖

━━━━━━━━━━━━━━

The next cycle may not be only memes.

It may have stronger narratives like:

🤖 AI

🏦 RWA

🔋 DePIN

💵 Stablecoins

🧱 Layer 2s

🎮 Gaming

🔐 Privacy

📊 On-chain finance

The key is not “everything pumps.”

The key is:

Strong narrative + real users + good tokenomics + liquidity = higher chance of winners.

The next altseason may be more selective.

Not every coin will win.

━━━━━━━━━━━━━━

7. Bad projects may get filtered out 🧹

━━━━━━━━━━━━━━

The 2023–2025 cycle exposed many weak altcoins.

Problems included:

🔓 huge unlocks

📉 no revenue

👻 no users

🐸 pure hype

🏦 weak liquidity

🧨 insider selling

By the next cycle, the market may become smarter.

Retail and institutions may care more about:

✅ real usage

✅ lower unlock pressure

✅ revenue

✅ product-market fit

✅ strong community

✅ transparent tokenomics

This could make the next altseason healthier than the last one.

━━━━━━━━━━━━━━

Simple summary 🧠

━━━━━━━━━━━━━━

The next cycle could have a higher chance of altseason because:

🟠 Bitcoin dominance is already high

🏦 institutions already entered crypto

🔵 ETH access improved through ETFs

💧 liquidity may improve later

🧍♂️ retail may return if prices get exciting

🤖 stronger narratives are forming

🧹 weak projects may get filtered out

But important warning:

Altseason is not guaranteed. ⚠️

If rates stay high, liquidity stays weak, BTC dominance stays strong, or ETH keeps underperforming, altseason can be delayed again.

The best signal to watch:

📉 BTC dominance starts falling

🔵 ETH/BTC starts rising

💧 liquidity improves

📈 altcoin volume increases

🧍♂️ retail attention returns

That is when the real altseason probability increases.

Until then, the next cycle is still a “maybe,” not a promise. 🧠📊

Sources: CoinGecko, Reuters, Chainalysis, Federal Reserve

English

🪙📉 Why Most Retail Investors Don’t Care About Crypto Right Now

Crypto is not dead.

But retail attention is weak. 🧍♂️📉

The market is now more institutional, more macro-driven, and less exciting for normal people.

━━━━━━━━━━━━━━

1. People got burned 🔥

━━━━━━━━━━━━━━

Many retail investors lost money in:

📉 2021–2022 crash

🏦 FTX / exchange collapses

🪙 failed altcoins

🐸 memecoin dumps

🔓 token unlock sell pressure

After losing money, many people stop caring.

They do not want another “next big thing.”

They want trust first. 🛡️

━━━━━━━━━━━━━━

2. Bitcoin won, but alts disappointed 🟠

━━━━━━━━━━━━━━

This cycle was mostly Bitcoin-led.

Bitcoin had:

🏦 ETFs

💼 institutions

📜 more regulatory clarity

💰 deep liquidity

But many altcoins did not follow strongly.

Retail usually comes back when many coins pump together.

But this time, it felt like:

Bitcoin up 📈

many alts weak 📉

retail bored 😴

━━━━━━━━━━━━━━

3. High rates reduced speculation 🏦

━━━━━━━━━━━━━━

When interest rates are high, people become more careful.

Safe assets can pay decent yield.

So people ask:

“Why gamble on random coins?” 🤔

High rates also reduce liquidity.

Less liquidity = less money for risky assets like altcoins. 💧📉

━━━━━━━━━━━━━━

4. Life is expensive 💸

━━━━━━━━━━━━━━

Many people are dealing with:

🏠 high rent

🍔 expensive food

💳 debt

🚗 car payments

📈 inflation

👶 family costs

When real life is expensive, people have less extra money for crypto.

Retail speculation needs extra cash.

Right now, many people do not feel rich enough to gamble. 🐢

━━━━━━━━━━━━━━

5. Too many coins confused people 🪙

━━━━━━━━━━━━━━

Before, narratives were easier:

Bitcoin

Ethereum

DeFi

NFTs

Layer 1s

Memecoins

Now there are too many categories:

🤖 AI

🔋 DePIN

🏦 RWA

🧱 Layer 2

🔁 restaking

🎮 gaming

🐸 memes

🪂 airdrops

🧬 old coins vs new coins

Too many choices = decision fatigue.

Retail gets confused and leaves. 😵💫

━━━━━━━━━━━━━━

6. Crypto became less fun 📱

━━━━━━━━━━━━━━

In 2021, crypto felt like a cultural movement.

NFTs, memes, DeFi, Discord, influencers, and huge gains made people excited.

Now crypto feels more like:

🏦 ETFs

📊 macro

📜 regulation

💼 institutions

⚖️ compliance

That is good for maturity.

But less exciting for retail. 😴

━━━━━━━━━━━━━━

7. Trust is still damaged 🧠

━━━━━━━━━━━━━━

Many people still think crypto is full of:

🚨 scams

🐸 pump and dumps

🔓 insider unlocks

💀 failed projects

📉 fake hype

Even good projects suffer because the whole space has trust issues.

Retail needs confidence before coming back.

━━━━━━━━━━━━━━

Simple summary 🧠

━━━━━━━━━━━━━━

Most retail investors do not care about crypto right now because:

🔥 many got burned

🟠 Bitcoin took most attention

📉 altcoins disappointed

🏦 high rates reduced speculation

💸 life is expensive

🪙 too many coins caused confusion

🧠 trust is still damaged

Crypto did not disappear.

But the crowd is tired.

This cycle is not like 2021.

It is more institutional, more selective, and less emotional.

Retail may come back later if:

📈 prices trend up strongly

🔵 ETH/alts outperform BTC

💧 liquidity improves

🎮 real apps become useful

🛡️ trust improves

🌈 a clear new narrative appears

Until then, most people are watching from far away.

Not because crypto is dead.

Because retail needs excitement, trust, and extra money.

Right now, many people have none of those. 🐢📉

Sources: Reuters, Chainalysis, CoinGecko, Federal

English

🌍📉 Why Life Feels Harder by Generation

“Easy life” benchmark:

💼 Stable job

🏠 Affordable home

💳 Low debt

👶 Can start family

💰 Can save money

👵 Can retire safely

━━━━━━━━━━━━━━

👴 Boomers

━━━━━━━━━━━━━━

Many had hard lives too.

But the ladder was clearer.

In the U.S., Boomers hold about 51% of household wealth. 💰

They also bought homes before prices rose so much.

Benchmark result:

✅ Best chance at home + wealth building

━━━━━━━━━━━━━━

👨💼 Gen X

━━━━━━━━━━━━━━

Gen X is the “sandwich generation.” 🥪

They often support:

👵 Aging parents

👶 Kids

🏠 Mortgage/rent

💳 Debt

👵 Retirement savings

They hold about 26% of U.S. wealth.

Benchmark result:

⚠️ More pressure, less comfort

━━━━━━━━━━━━━━

👩💻 Millennials

━━━━━━━━━━━━━━

Millennials were hit by:

📉 2008 crisis

🏠 Expensive housing

🎓 Student debt

💼 Less stable jobs

📈 Higher cost of living

Globally, people age 18–39 worry about housing more: 60% vs 38% for ages 55–64.

Benchmark result:

🚨 Harder to buy home + save

━━━━━━━━━━━━━━

🧑🎓 Gen Z

━━━━━━━━━━━━━━

Gen Z faces:

🏠 High rent

🤖 AI job disruption

💼 Harder entry-level jobs

📱 Social media pressure

🌍 Global competition

In 2025, about 262 million young people worldwide are not in work, school, or training — about 1 in 4.

Benchmark result:

🚨 Hard start to adult life

━━━━━━━━━━━━━━

👶 Gen Alpha

━━━━━━━━━━━━━━

Still young, but future competition may be tougher.

They may need:

🤖 AI skills

💻 Coding/digital skills

🧠 Creativity

🌱 Climate adaptation

🌍 Global mindset

By 2050, about 1 in 6 people globally may be over 65, meaning younger workers may support bigger aging populations.

Benchmark result:

⚠️ Future depends on skills + policy

━━━━━━━━━━━━━━

🧠 Simple summary

━━━━━━━━━━━━━━

Older generations had struggles too.

But the “normal life package” became more expensive:

🏠 Homes cost more

💳 Debt is higher

🎓 Education matters more

💼 Jobs are less stable

🤖 Technology changes faster

👵 Aging society adds pressure

The problem is not laziness.

The ladder is longer, more expensive, and less stable. 🪜

Sources: IMF, Federal Reserve, UN

English