고정된 트윗

Uday 👨💻📈

13.5K posts

Uday 👨💻📈

@u_plus_k

In a default consumptive state | Early stage venture investor |

Madrid, España 가입일 Ocak 2012

264 팔로잉325 팔로워

@AdamDraper How can I get in touch to share a couple of pitch decks with you?

English

Really unfortunate how many Substacks have become pure AI slop these days.

Seems almost insulting as a reader

English

@BigJohn043 LPs don't know you're saying? Its prob a reflection of where the NAV or marks should actually be

English

In fairness, Blue Owl probably knows a lot more about their portcos than the public markets. Their portfolio may very well be pristine with largely green flags....

junkbondinvestor@junkbondinvest

Blue Owl says their software portfolio is "pristine" and has "largely green flags" Public markets disagree (-24% YTD, 52-wk lows). 15% redemptions also disagree. But the marks agree. That's what matters.

English

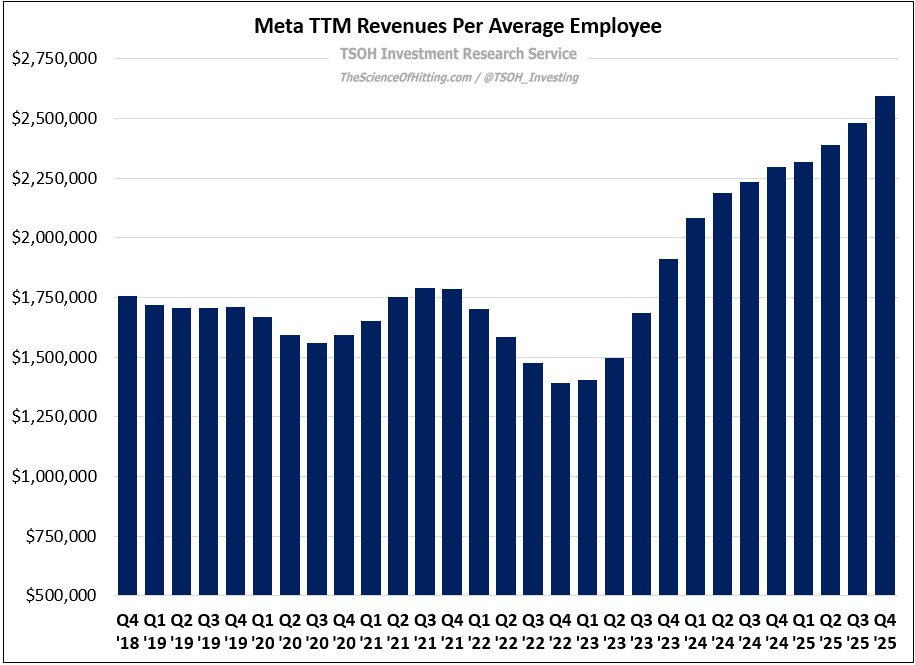

Meta TTM Revenues Per Average Employee $META

English

Uday 👨💻📈 리트윗함

Best bit of journalism I've read around Man Utd in years theguardian.com/football/2026/…

English

@colejaczko Cringe galore mate. All this lifestyle stuff is fine but this? You're better than that mate

English

@PabloFedez Sí, pero llegamos a la escala que necesitan? Más probable si es un mercado europeo más unificado

Español

@u_plus_k Vamos nos lo pasaríamos pipa aquí apostando a movidas tipo

"el tiempo que iban a tardar Koldo y Abalos en llevarse a señoritas a Soto del Real"

Español

Gente del venture:

¿Creeis que cabe en España/Europa un Kalshi o Polymarket europeo?

Para mí tendría todo el sentido comercial que haya uno por pais.

Para apostar a las movidas locales de cada uno.

Ayer me metí en sus webs por primera vez, y en portada no me podía dar más igual como iban a quedar los Raptors contra los Timbervolwes o no sé qué de las Kardashian.

Español

@RihardJarc NVDA being hyperscaler/cloud agnostic has deeper moats. A TPU business that is not vertically integrated will fail as a standalone.

NVDA mentions Gemini 3 was also trained on Blackwell, so not sure aout that claim either. And What about CUDA then? Did you consider it?

English

Hence, the IF, in reality, the margin would probably be lower, but the annual revenue growth rate for next year will/would be higher than $NVDA, so it's hard to say what multiple it would fetch.

What many still fail to comprehend is that we now have the number 1 AI model that was NOT trained on $NVDA but TPUs. This will have big ripple effects in the industry.

English

I am publishing my $GOOGL TPU deep dive on Monday. Based on my estimates, if $GOOGL didn't have TPUs, they would spend an additional $30B-$40B in CapEx this year to get a similar amount of compute from $NVDA. Meaning $GOOGL's CapEx for this year would go from the guided $91B to $120B-$130B.

Looking ahead to next year, if TPUs were a standalone business and had a similar multiple and margin profile to $NVDA, they would be a +$800B standalone business.

More in the article.

English

@holistic_pm Healthy market correction? Or more stress in the credit markets?

English

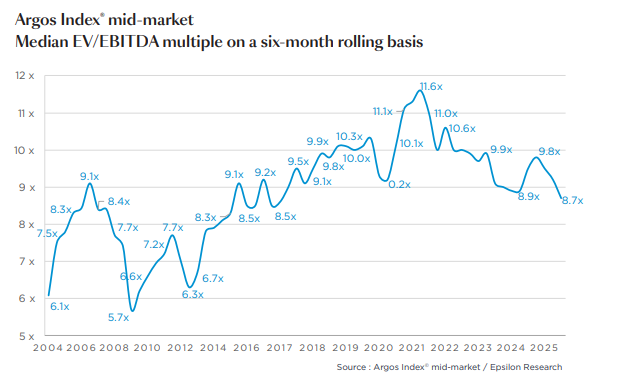

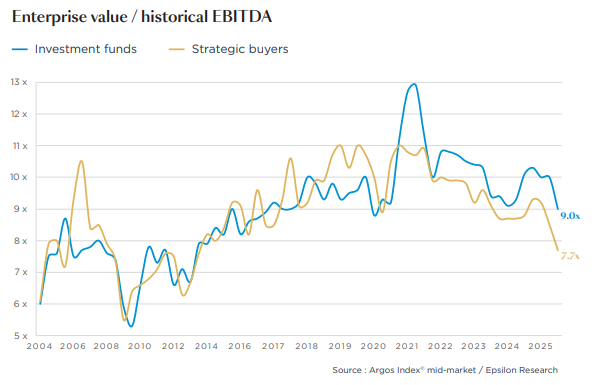

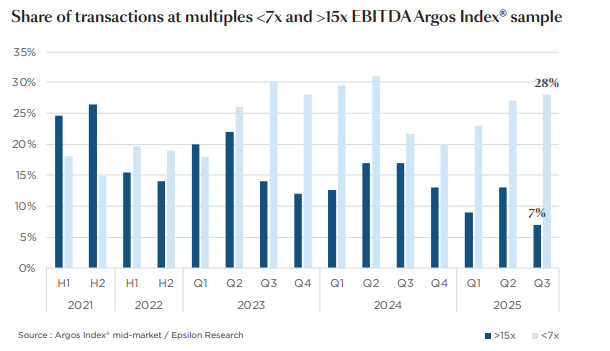

Valuations for European mid-market deals continue to decline, reaching levels not seen in years.

1. Argos Index fell to 8.7x EV/EBITDA, the lowest level since 2017

2. Both Private Equity and strategics are paying down (resp. 9x and 7.7x)

3. Only 7% of deals are now closed above 15x EBITDA, a record low

English

@InvestmentTalkk Absolute monster of a product. Then they're "what are even the returns on AI capex??"

English

Facebook/Meta has a knack for turning their largest threats (Mobile, Short Videos) into their largest strengths.

Koyfin@KoyfinCharts

$META Reels Monetization Timeline: - Q3 20': Launched in August 2020 - Q2 22': $1 billion run rate - Q3 22': $3 billion run rate - Q2 23': $10 billion run rate - Q3 25': "Reels now has an annual run rate of over $50 billion".

English

It is only a real breakthrough if there is a LuxCo on the other side. Sigh. This hate towards Big Tech is just ridiculous.

Josh Wolfe@wolfejosh

1/ why Quantum is BULLSHIT "paving a path towards potential future" like saying: 'Working towards possibility of maybe a thing that might one day be a breakthrough if a breakthrough were to maybe occur' Here I assemble just 2005 to 2015 annual headlines or this BULLSHIT

English

@RDPandole Still a monopoly by a mile. And the moat is widening not shrinking (if you include other markets like robotics/autonomy).

English

This stuff is on seriously shifting sands .. which is why I don’t understand the current nvdia valuations .. their moat is def wide .. but isn't immune to being drained ..

just because we don’t see what’s going to allow the competition to catch up doesn’t mean it might not happen ..

Betting on cyclicals like memory and chips is always tough (although hugely rewarding if you get it right ofc) .. there’s always not enough of them and suddenly a glut ..

kudos to everyone who’s made money on the back of this but luck > perception / knowledge in this vertical in many cases

SemiAnalysis@SemiAnalysis_

The quality of AMD software now is totally different from when we started deeply using summer 2024. In 2024, we were running into many ROCm specific bugs. Today, the frequency in running ROCm bugs is orders of magnitude lower. AMD hardware is pretty good & the software is getting better every night. On Llama3 70B FP8 reasoning workloads at frontier lab volume pricing, MI300X vLLM offers 5-10% lower perf per TCO than H100 vLLM from our benchmarking across all interactivity levels (tok/s/user) and competitive perf per TCO on MI325X vLLM vs H200 vLLM and GPTOSS MX4 weights 120B Mi355 vs B200. Of course there is also various workloads in InferenceMAX where AMD software is currently losing too. The point of InferenceMAX is that there is nuance and we benchmark every night so that we are able to track the software improvements. visit inferencemax dot ai to see the full set of nuanced nightly results.

English

Interesting read but nearly every time OpenAI has gone away from its core product, it has mostly underwhelmed.

CustomGPT store, Operator, and now their new Agent Builder have all seriously underwhelmed.

Image & video and great but Google is still better.

Serious competitor to TikTok? Come on now 😆

English

Over the last two decades, Google captured intent.

You go there, punch in what you want, and it directs you to where you can get it.

Over time, it received more and more "rent" as a middle-man, by charging advertising fees.

Despite this, if you knew how to play ball with Google (pay them for advertising, jump through the SEO hoops), you could build a pretty solid business.

But now ChatGPT has captured intent.

I no longer use Google Search. Like, ever.

(If you'd told me that 3 years ago, I wouldn't believe you)

And this time around, things are very different.

Because now, if your service is digital, ChatGPT doesn't need to direct users to your business at all.

Instead, it can simply solve the problem for the user.

This destroys huge numbers of businesses.

First, it killed education and reference sites.

Need a recipe? It creates one.

Want to learn to code? ChatGPT will teach you inline.

But hell, why even learn? It can now just code for you.

Right now, it's killing code editors and IDEs.

We all thought Cursor was a great business just a year ago.

Now, tools like Codex and Claude Code may render Cursor and Windsurf irrelevant.

Like a stack of punch cards to feed into a mainframe.

You used to Google "how to do my taxes" and get sent to TurboTax.

Soon, ChatGPT will just ingest your accounting data and do your taxes for you.

Next up, will be design and creative tools.

Do I need Photoshop, Figma, or Ableton Live when I can simply type a string of text describing what I want and have it spit out a perfect song, video, image or design?

Earlier this week, ChatGPT welcomed "Apps" into ChatGPT.

Companies like Booking .com, Spotify, and Figma excitedly announced that they were integrating.

I'd wager a bet, that within 3-5 years, OpenAI will simply replace these companies with its own inline services.

After all, the only reason Google didn't do this was because didn't make sense from a resources perspective.

They owned the intent and could have competed—it would have made business sense—but they had limited human capital.

In the old world, competing with a business line required allocation of limited human capital. But now, for companies like Anthropic and OpenAI, it's simply allocation of compute.

Sora is just a small preview.

With one fell swoop, they've created a serious competitor to TikTok.

But it's not just TikTok that is under siege...

Right now, Sora is only producing 10 seconds at a time.

Soon videos will be 1 min, then 10 min, then 60 min, then 2 hours.

In time it will compete with every video platform—TikTok, YouTube, Netflix, and even Hollywood.

Software is the most vulnerable.

They've already started with consumer and soon will move to enterprise.

Adobe. Notion. Salesforce. DocuSign. Zoom.

Any software company that is JUST software or digital assets will be under siege from OpenAI in the long-term.

Building a pure software company today is like opening a Blockbuster in 2007.

You will soon find yourself competing with a juggernaut that has infinite scale and zero marginal cost.

Grammarly? Built into the base model.

Expensify? "Scan and process these receipts."

Calendly? "Find a time that works for everyone."

Notion? "Organize my thoughts on this project."

Stock photo providers like Getty? "Make me an image with X and Y."

Resume builders? "Write my resume for this Google PM role."

Travel planning sites? "Plan my entire Japan trip with bookings."

You get the idea.

So, who is safe?

Businesses that have a hardcore moat.

Amazon is safe because warehouses and logistics are atoms, not bits.

Spotify is safe because it has rights to the music libraries.

Airbnb is safe because they own relationships with millions of property owners.

Stripe is safe because payment processing requires trust and regulatory compliance.

Apple is safe because of its hardware ecosystem and userbase.

The pattern is brutal and clear: if you exist purely in code, you will be replaced by code.

If you have physical assets, regulatory barriers, network effects with real humans, or IP rights – you might be safe from the steamroller for a while.

But unlike the shift from desktop to mobile, which created new opportunities, this shift is consolidating power.

The largest network has always won. But now, they're collecting your profits instead of the rent.

English

@SleepwellCap The Odd Lots podcast with the Circle CEO was pretty good. open.spotify.com/episode/5Lmmug…

English

what is the best thing you've read/watched/listened to on Stablecoins and the risk (or opportunity) they pose to cross-border payments?

English

@SleepwellCap Sending EUR the other way around (US to Spain) worked quite well with Revolut on the receiving end when I tried it with a friend, but Wise is way ahead when it comes to fees and transparency.

English

Cross border transfer personal anecdote:

Friend in Spain needed to send EUR to my US bank account, so we opted for ACH from his Revolut acct (supposed to be super friendly), seemed easiest and most direct. Money got stuck for days in the intermediary bank and never arrived. Over a week went by, still waiting for response on what happened, money is still stuck somewhere.

Decided to open a EUR Account on $WISE (already had USD account, took <30 seconds) and told him to send the money there instead. EUR arrived instantly (using local EUR rails), I then converted it to USD at the midpoint rate and sent a real-time transfer to my Chase account.

From EUR to USD in my acct in basically <10 minutes. Total cost $1.13. Felt pretty magical honestly, the experience with cross border transfers is always a pain.

English

Uday 👨💻📈 리트윗함