Chris Coombs

5.4K posts

Chris Coombs

@chefchriscoombs

Founder • Creator • Entrepreneur • Visionary @bosse_pickledom • @bosse_enoteca • Bosse Cafe • Bosse Sports Lounge • Co-Owner • Co-Founder @deuxave

BOSTON, MA Katılım Ağustos 2009

561 Takip Edilen2.5K Takipçiler

@jaytatum0 You will be back and better than ever before you know it! Heal up Champ!

English

Chris Coombs retweetledi

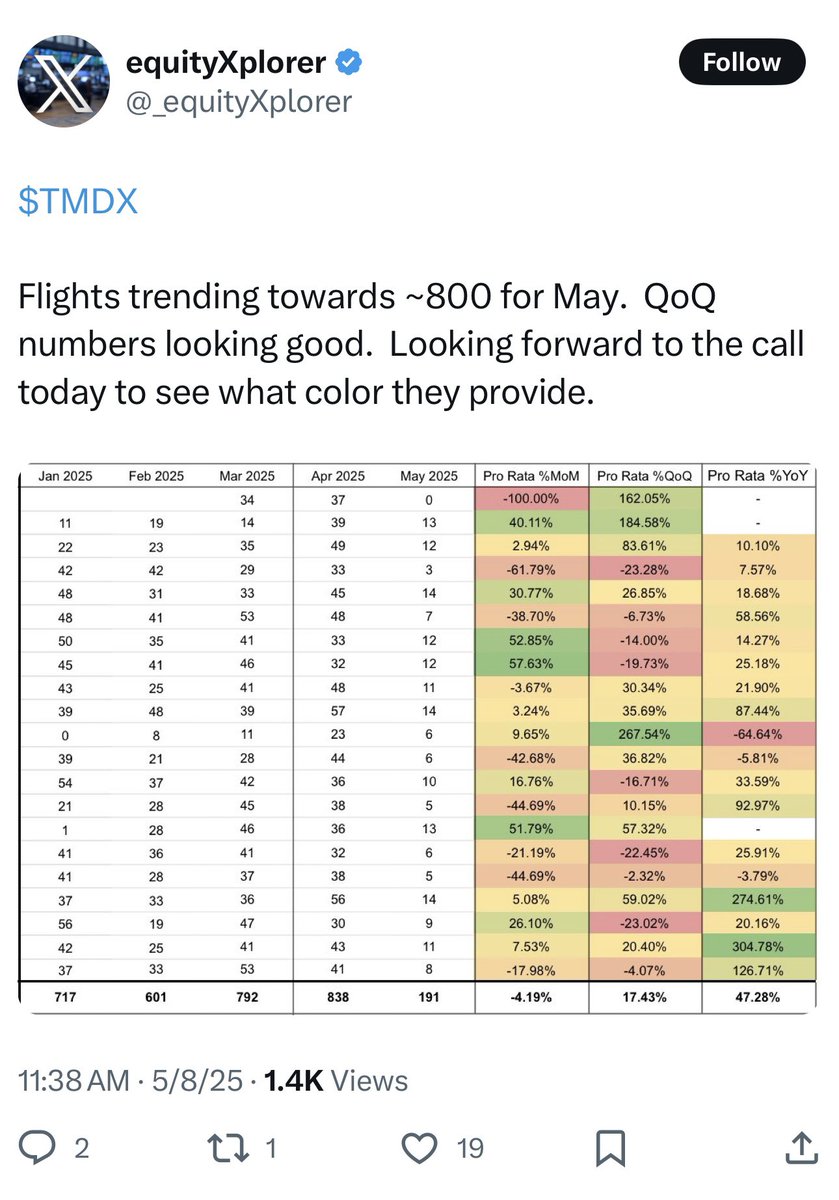

It's going to be a monster day for $TMDX which is currently up +21% premarket but could be up 30-40% by end of day.

$TMDX posted blowout Q1 earnings last night... revenues up 48% YoY and 18% QoQ.

On top of that Q2 flights (which we track daily) are currently trending 17% above Q1 flight numbers so we could be looking at another blowout report in 3 months.

$TMDX also reported $0.70 in eps thanks to 17.9% net income margins. The eps number was 190% above street estimates.

To top it off, $TMDX raised full year 2025 revenue guidance from 22.5% (midpoint) to 30% (midpoint). I've owned $TMDX for 4+ years so I know how the CEO thinks about guidance. If they are raising guidance to 30% after Q1 earnings then it means they have at least 1-2 more raises coming before year end. This is why I think $TMDX does ~40% YoY revenue growth which puts the number at $615-620 million.

$TMDX came into Q1 earnings trading at 5.5x 2025 EV/sales. If you look across growth stocks and medtech stocks, that multiple is way too low for a company growing revenues at ~40% with ~18% net income margins and very little dilution.

I believe $TMDX should be trading at 8-10x NTM EV/sales based on current guidance, current Q2 flight data, 1-2 more guidance increases, OCS 2.0 in the pipeline, KidneyOCS in the pipeline and European expansion coming soon.

NTM revenues should be approx $645M, throw a 9x multiple (very reasonable) on that and you get fair value of $170 per share.

Now let's talk about the 28% short interest and what that might mean. I don't know if we see $TMDX short squeeze higher but it's the perfect setup... big revenue beat, big earnings big, big guidance raise, big gap up and big short interest with 10-12 days to cover.

This is not your typical short squeeze shitco where most investors don't care about the company and are willing to sell on a short term pop. I believe the average $TMDX investors cares about this company, wants to hold for the next 3-5 years and has no interest selling on a pop just so the shorts can cover. We know $TMDX is going to $200+ in the next 12 months and we're here for the ride.

April 2024, $TMDX gapped up +17% at open and closed up +24% on the day.

November 2023, $TMDX gapped up +42% and closed up +51% on the day.

Congrats to all the $TMDX shareholders, you earned this!!!!

English

@JonahLupton @ScorpionFund Send them Ramen Noodles. 💪🏻💪🏻

English

Thanks for this post because it proves you don't know shit about this company or follow it very closely.

If you did you'd know that $TMDX was servicing multiple planes at the end of April and beginning of May which is why the late April and early May flight numbers look slower.

This means $TMDX is using charter planes until their own planes are back in service.

$TMDX just crushed Q1 earnings... beating estimates by 16% and raised full year revenue guidance to 30% (at the midpoint)

You're a fucking joke, just give up.

English

$TMDX Our observations prior to Transmedics earnings report. We remain short.

1. Flight data posted by retail investors suggests that the May run-rate is flat with March and down from April. See screenshot. We suspect that TMDX achieved a one-time bump in flights by waiving or cutting fees for dry runs. Our opinion is based on color from two customer calls. The stock seems to move up and down like a levered derivative on the latest weekly flight count posted on this platform. Look out below if the May trend continues.

2. Transmedics was a dud at the key annual medical conference (ISHLT in late April). Investors hyped up the potential of new versions of their device but were eerily quiet after day one. We predict the trials will never enroll or complete, and that $TMDX will remain a one-trick pony dependent on its liver product. Liver was already the vast majority of revenue last quarter, and we expect the concentration on one SKU to increase every quarter.

3. We expected the product "innovation" at ISHLT to flop as Transmedics head of product quietly departed just a few weeks prior to the key annual conference. Mark Anderson was at TMDX for almost 12 years, per his LinkedIn bio, see screenshot (linkedin.com/in/mark-anders…). His title was VP Product Development. His name appears to have been quietly scrubbed from Transmedics website around early April with no 8-K. We find it surprising for a longtime executive to depart immediately prior to a purported major product upgrade.

4. OrganOx today announced an upsizing of its recent financing to $160MM total. This is substantially larger than the net proceeds from TMDX's IPO and suggests strong traction by a key competitor. We think OrganOx is eating into Transmedics market share. Customer interviews lead us to believe that Organox has huge pent up demand from TMDX users that it has been thus far unable to fill. We think OrganOx's pace of product shipments was a bit slow, but we heard anecdotally that it picked up in Q1. We recently spoke with a large customer of TMDX who told us that they would like to use Organox but can't get a device at the moment.

5. Two other competing devices appear to be on the cusp of FDA approval, and these pose an even more significant existential threat to TMDX than OrganOx. One is the Bridge To Life/Vitasmart hypothermic oxygenated machine perfusion system. We heard that one of TMDX largest customers (different than the one above) expects to move 100% of its OCS liver usage to this device upon FDA approval. We're not sure of the exact cost but heard a $5,000 figure, which makes it essentially free vs. TMDX outrageous and unsustainable device pricing.

The second device is Organ Recovery Systems LifePort Liver Transporter, also a fraction of the cost. The device poses a particularly acute existential threat to TMDX as ORS kidney product dominates the space; and we have heard tremendous enthusiasm from KOL's who appear to be eagerly waiting for FDA approval.

6. We recently spoke with a marquee transplant center which we believe to be one of TMDX's highest volume users (top 5). They stated their usage in liver (their main use case) hit the wall in 2H 2024 and declined ~20%, and that they do not expect it to recover. They named two marquee institutions in the New York who they stated have also "taken a step back" from TMDX ("everyone frustrated"). We think TMDX has plugged a finger in the dike by leaning into smaller, second-tier transplant centers while it can.

Note: Please refer to the disclosures in our Jan 10, 2025 report on TransMedics, which this post incorporates fully by reference and may be downloaded at scorpioncapital.com. We remain short TransMedics.

English

Chris Coombs retweetledi

After the last two days, RSI (relative strength index) on $SPX (S&P 500) is at 20.6 on the weekly chart and 19.4 on the daily chart.

20.6 on the weekly chart is the 3rd lowest reading in the past ~20 years.

The only lower RSI's over the past 20 years are the Covid lows (March 2020) and the GFC lows (Oct/Nov 2008).

After those $SPX bottoms, the index was up an average of 75% over the next 12 months. No joke. I almost didn't believe it myself, had to double check the charts.

While I certainly don't expect $SPX to be up 75% over the next 12 months, it's very possible we're getting close to a new bottom which means there will be some tremendous buying opportunities in the near future.

I'm confident these numbers are correct however if I'm mistaken feel free to say so.

English

Chris Coombs retweetledi

Beginning in early January, we began acquiring a position in @Uber. Today, we own 30.3 million shares.

I have been a long-term customer and admirer of Uber beginning when Edward Norton showed me the app in its early days. I was also fortunate to be a day-one investor in the company through a small investment in a venture fund.

While a great business, Uber suffered from erratic management. Since he joined the company in 2017, Dara Khosrowshahi CEO has done a superb job in transforming the company into a highly profitable and cash-generative growth machine.

We believe that Uber is one of the best managed and highest quality businesses in the world. Remarkably, it can still be purchased at a massive discount to its intrinsic value. This favorable combination of attributes is extremely rare, particularly for a large cap company.

We will have more to share about our thinking on the company shortly.

English

@JonahLupton I am declaring today the bottom in $TMDX day. It is all up from here! What a steal to be able to buy more at $58 this morning!!!

English

Chris Coombs retweetledi

Pickleball takes New England by storm wcvb.com/article/pickle…

English

Chris Coombs retweetledi

@StockSavvyShay @JonahLupton I think we got them all, except you got $CELH at $3

English

$AMD was obvious to buy at $100 and many waited

$CELH at $48 (this year) was the easiest money and people waited.

$PLTR at $14 was extremely undervalued and many waited

$META was obvious to buy at $200 and everyone waited

$CRWD was a clear buy at $150 and people waited

$TMDX at $38 with a market cap of $1 Billion was a steal and nobody wanted to buy it.

Focus on the essentials: aligning fundamentals and technicals is key to making informed decisions, irrespective of prevalent negative news.

Act decisively to avoid missing opportunities and personally filter out the noise, as positive insights are rarely highlighted 💯

English

metrowestdailynews.com/story/entertai…

Can’t wait for this exciting new project!

English

Chris Coombs retweetledi

@Jeffdeehan @BarneyPelty Speaking of pickleball, my buddy is doing all 4 restaurants for this new 100,000 square foot pickleball complex going into the Boston area bostonmagazine.com/restaurants/20…

English

Chris Coombs retweetledi

Big news out of Natick for #Pickleball lovers @chefchriscoombs @BostonMagazine @blumie bostonmagazine.com/restaurants/20…

English

Chris Coombs retweetledi

News: Chris Coombs is opening four new dining spots, all of which will be within a pickleball facility. bostonrestaurants.blogspot.com/2024/02/chris-…

English

Chris Coombs retweetledi

Boston Chops and Deuxave’s Chris Coombs gets into the pickleball game with Bosse, an indoor pickleball and culinary complex coming to Natick this fall. trib.al/gEM5XgU

English

Chris Coombs retweetledi

News -- Chris Coombs to open four dining spots at a new pickleball facility in Natick. bostonrestaurants.blogspot.com/2024/02/chris-…

#natick #restaurants

English