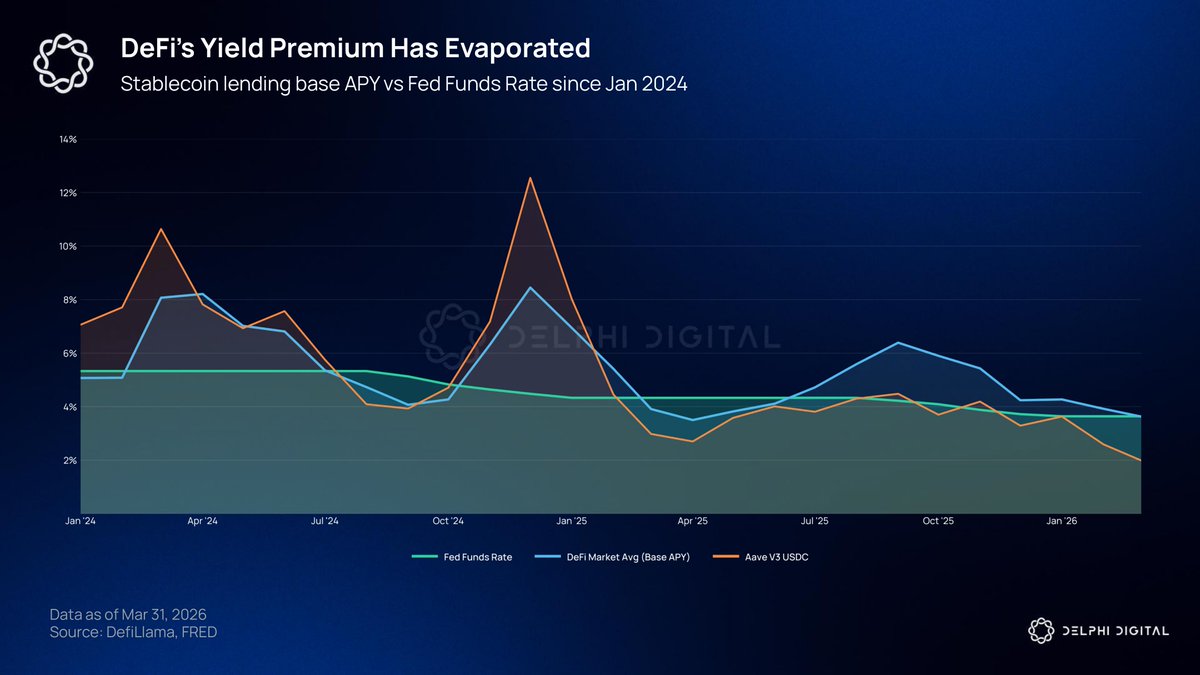

DeFi Yields Have Been Declining

DeFi spent stretches of the last two years outearning the Fed, and understanding why tells you how onchain credit markets work.

Lending rates on Aave are set algorithmically based on utilization. High utilization pushes rates up while low utilization drags them down. The rate you see is a live market price for crypto leverage.

The BTC ETF approval in early 2024 and the election later that year pulled traders into borrowing stablecoins to buy more of the assets they expected to climb. Aave V3 USDC pushed above 10% in 2024, and DeFi was paying meaningfully more than the Fed.

That premium has compressed. Stablecoin supply more than doubled from early 2024 to 2026. Borrowing grew too, but not in the concentrated bursts that pushed rates up the first time around. The market wide base APY hit parity with the Fed Funds Rate recently, leaving little premium for the smart contract risk of parking stablecoins onchain.

DeFi yields have not been a reliable premium over TradFi. They are a cyclical reflection of the demand for leverage.

Jason explains why he's not betting against Bitcoin.

"Saylor has a bazooka of cash that he hasn't yet deployed. If you short Bitcoin into Saylor buying, you're probably just going to get ran over. I'd much rather spend my risk elsewhere."

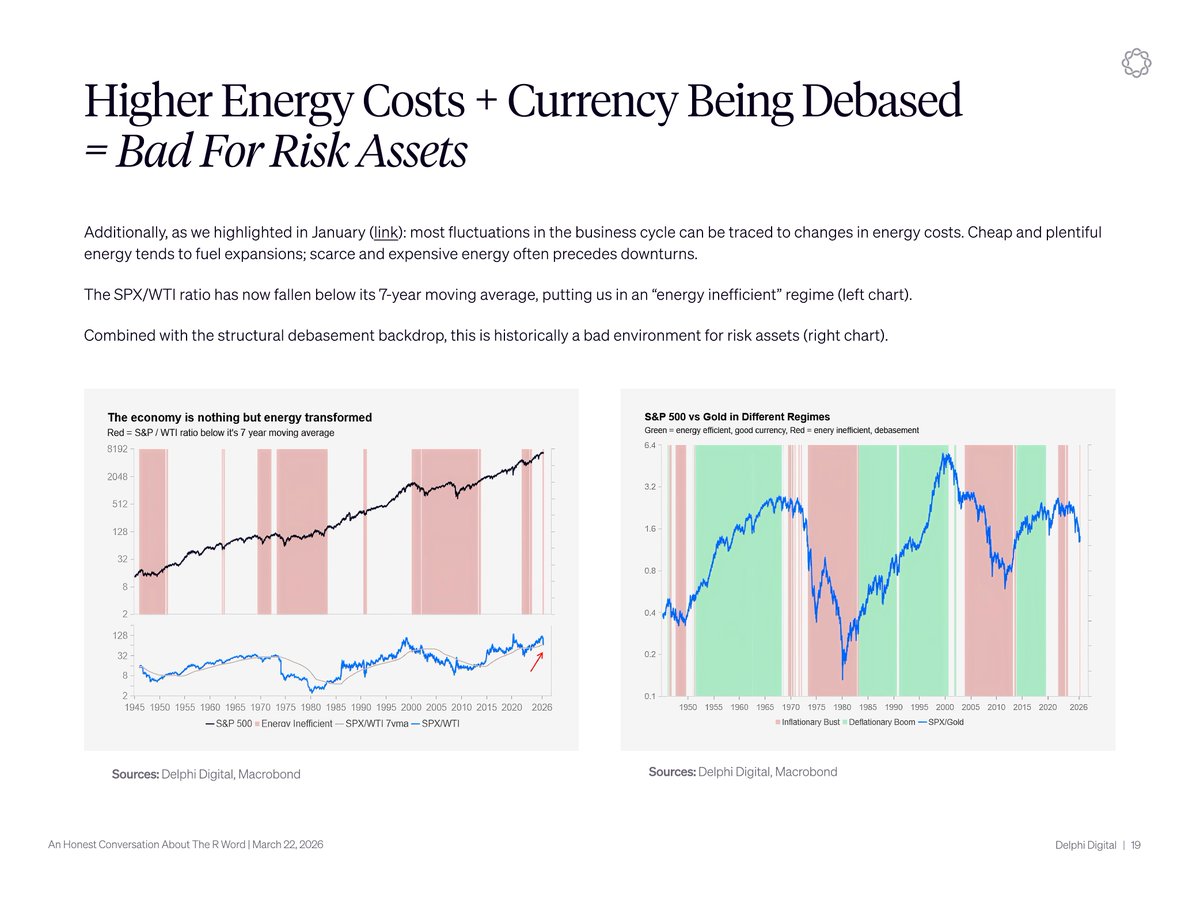

The SPX/WTI ratio fell below its 7-year moving average, flipping us into an energy inefficient regime.

Most fluctuations in the business cycle can be traced to one thing: the cost of energy.

Cheap and abundant energy fuels expansions while scarce and expensive energy precedes downturns.

Combined with the structural debasement backdrop we're already in, this is historically a bad environment for risk assets.

Inflation is settling above target, supply-driven and acyclical inflation are rising again, and the Gold/UST 10y total return ratio continues to trend in gold's favor.

Until that reverses, the bar for owning duration over gold remains high.

Excluding 2020, every recession since 1990 was preceded by an abrupt rise in energy prices.

Even an immediate ceasefire takes months to normalize flows.

We're in that regime now.

Jason notes that all of crypto has been in a brutal downturn outside a few outliers.

"L1s have mostly been slaughtered with Hype being the big outlier. There were a few resurgencies in DeFi with names like Morpho and everything else is pretty terrible."

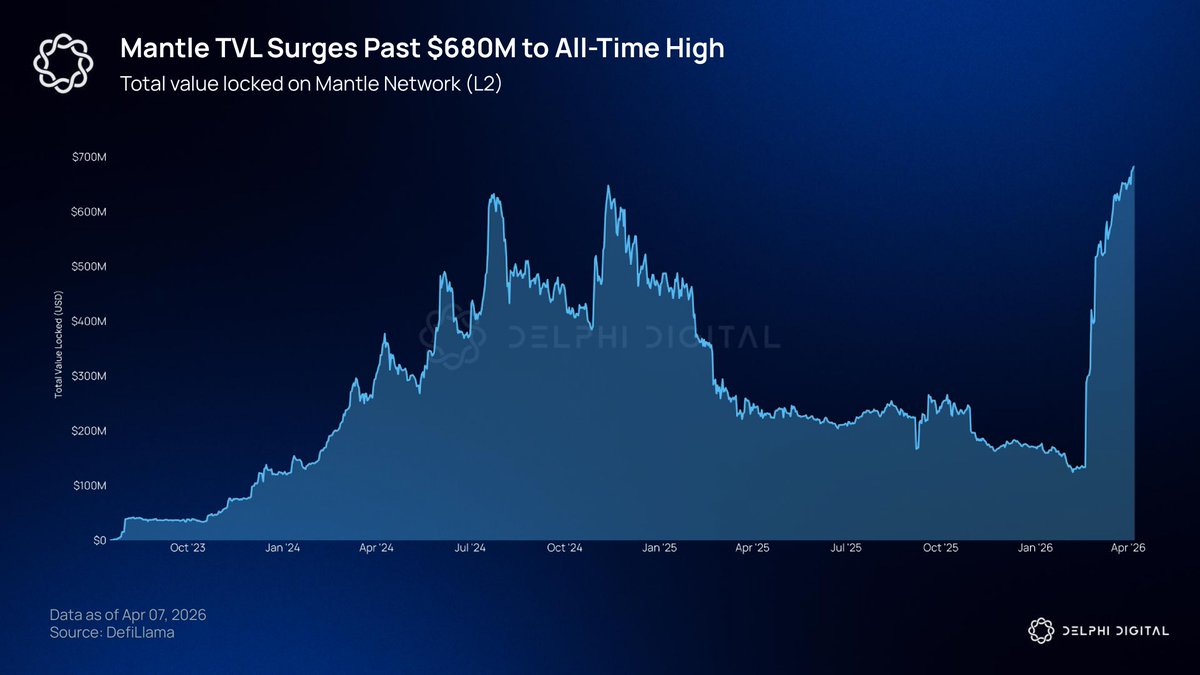

Mantle has become one of the fastest growing L2s of 2026.

TVL has climbed from around $135M to a $682M all-time high.

The catalyst was Aave's deployment paired with an 8M MNT incentive program from Mantle. Demand has been deep enough that supply caps have been raised repeatedly on Mantle markets.

Every major exchange has talked about bridging users into DeFi for years. Mantle and Bybit are aiming to make this happen end to end.

If the capital stays once the rewards end, Mantle could be the proof case for turning exchange users into onchain users at scale.

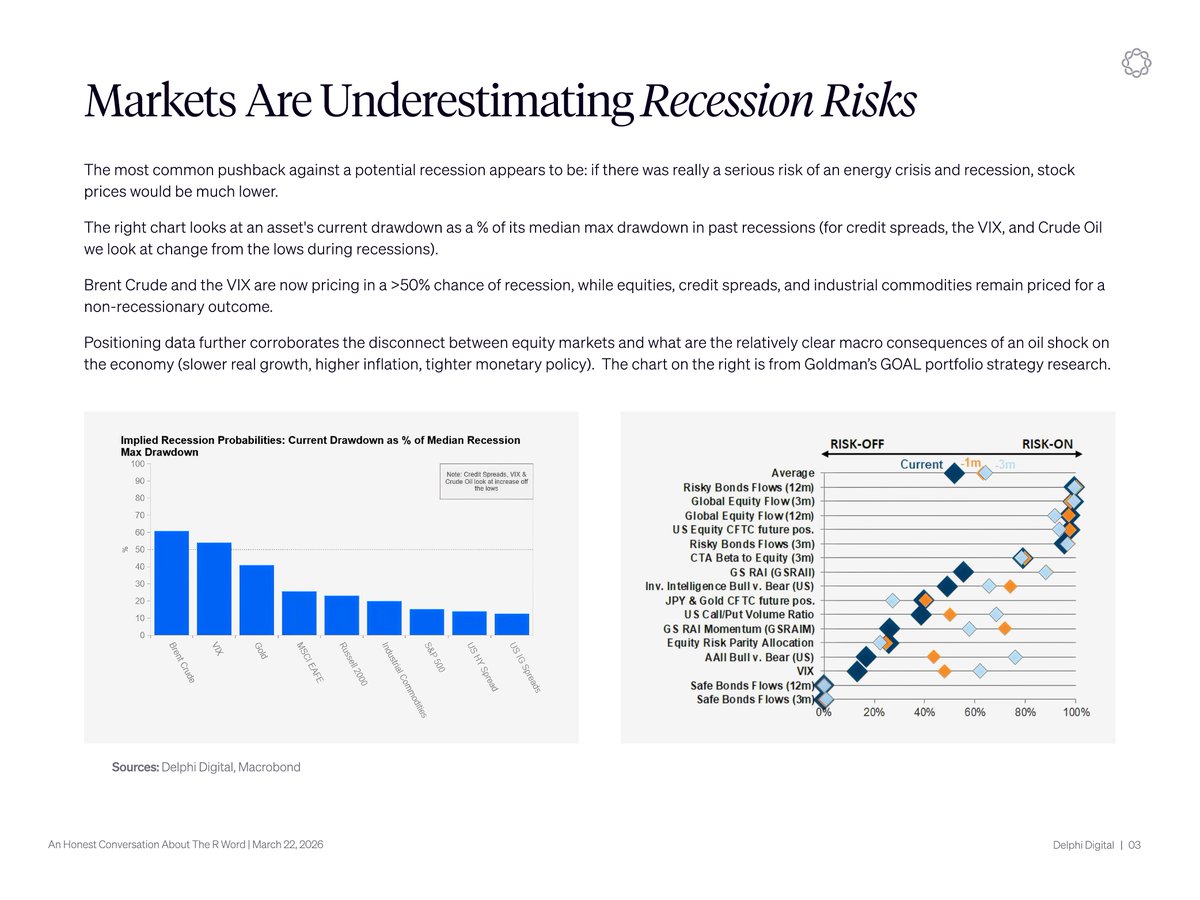

Our updated deck for our “An Honest Conversation about the R Word” report is now live.

Since our original publication on March 22, there has been no sign that the ongoing conflict in the Persian Gulf is set to end quickly. Despite this, implied recession probabilities across assets have actually fallen over the past two weeks.

Our recession framework is simple: Fragile Conditions + Trigger = Recession.

The conditions are in place. Fiscal impulse is negative and set to worsen as most benefits from the OBBBA are front-loaded into the first half of this year. Global easing is fading, with central bank policy breadth already rolling over. Liquidity offers little margin of safety for anyone to backstop a selloff. And supply-driven inflation is rising again.

The trigger is here. Roughly 20 to 30% of crude, LPG, LNG, and refined products flow through the Strait of Hormuz. Even an immediate ceasefire would take months to normalize flows and prices.

Yet recent BofA fund manager survey's had just 5% expecting a hard landing. Equity positioning has barely pulled back. Markets have a well-documented inability to price tail risks until they become the base case.

The recession probability is now at least a coin flip and rising every day. The largest hit to risk assets has always come at the beginning of recessions - the part markets refuse to price until it's too late.

Jose discusses the secondary consequences of the war.

"There's a lot of second and third world consequences from having the Strait closed this long. From oil and gas facilities getting bombed. Some of this may be offline for years. We've never seen this level of supply destruction."

Jason remains cautious about equities.

“I still feel like equities haven’t priced in a lot of what’s going on. I’m still cautious. I don’t really trust either side right now.