Sabitlenmiş Tweet

poorlyRICH

1.2K posts

poorlyRICH

@TORROCRYPTO

CEO of risk management @ftx/@celsius/@lehman brothers CRYPTO &STOCKS

Katılım Ağustos 2020

710 Takip Edilen69 Takipçiler

poorlyRICH retweetledi

Took a list of all the S&P 500 PE multiples

Then asked AI:

Looking at this S&P 500 forward P/E heatmap through the lens of:

Highest expected growth for the next 2 years

Lowest forward valuation multiples

Most durable AI / infrastructure tailwinds

Here are the 4 companies that immediately stand out

English

poorlyRICH retweetledi

Overheard behind me while watching #H5N1 NAS workshop today: "You want to really make a pandemic, make hantavirus human transmissible"

English

poorlyRICH retweetledi

Our generation had 2 opportunities for generational wealth

The 1st one was buying crypto 10+ years ago

The 2nd one will be being on the right side of the trade when the biggest ponzi in history goes to zero

unusual_whales@unusual_whales

A mild morning.

English

poorlyRICH retweetledi

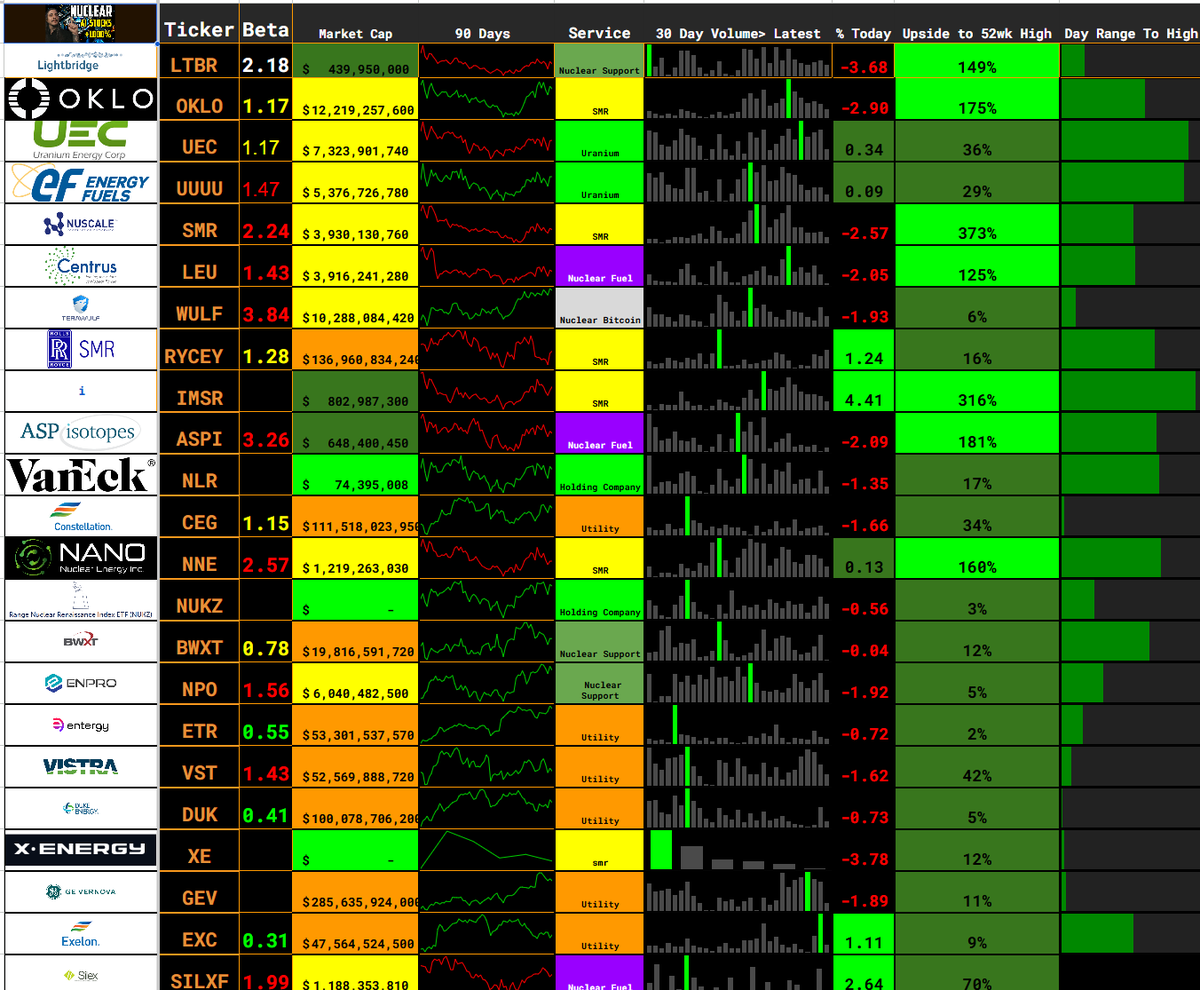

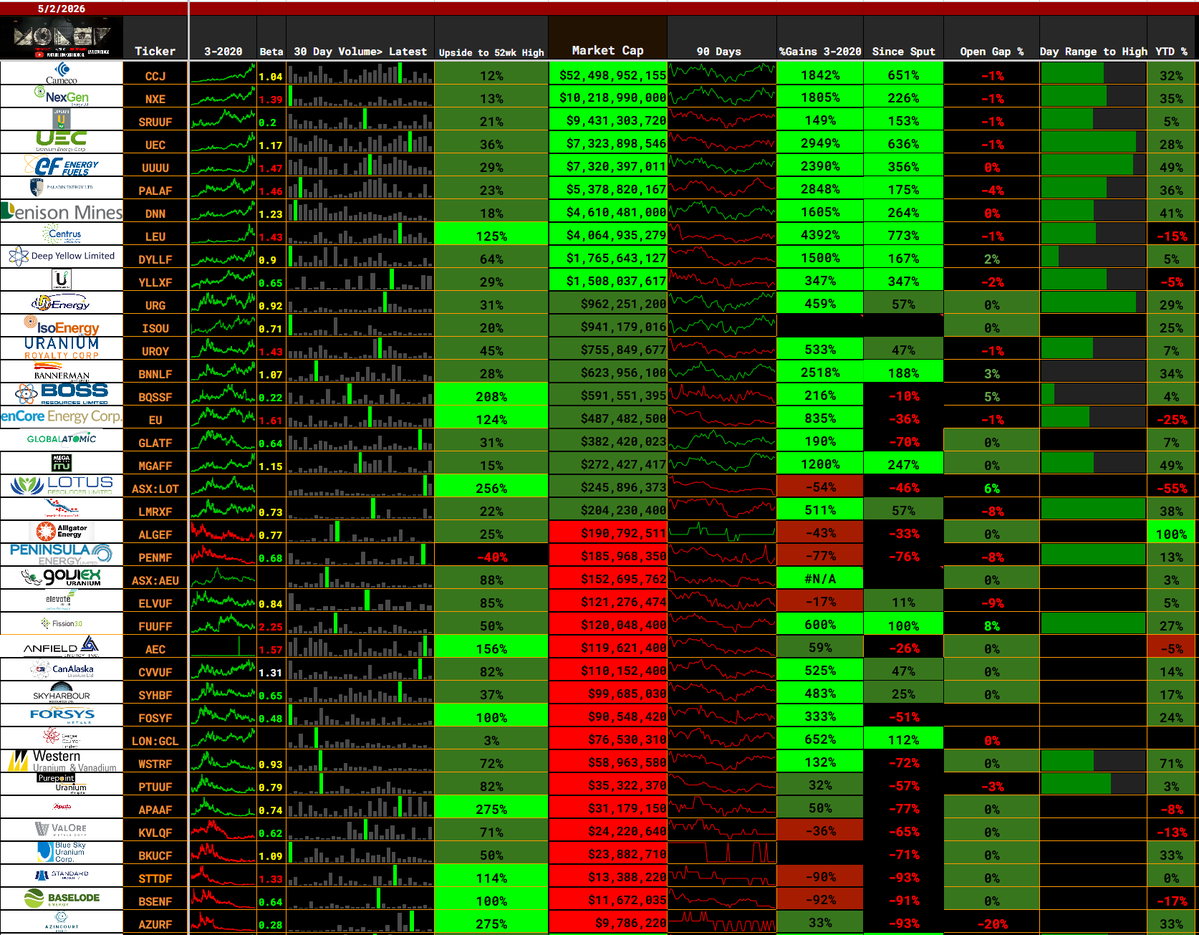

@InTheAssembly To fix your chart ;) Uranium & Nuclear Energy stocks. Been covering them for 6 years. The updated thesis. x.com/derekquick1/st…

Derek Quick@derekquick1

Uranium & Nuclear Energy Stock Squeeze via the Global AI Power Paradox is HERE, $1,000 Uranium is probable as it is the true bottleneck sector. U.S. Uranium producers have a smaller market cap combined than that of Dogecoin. Leopold Aschenbrenner dropped his Situational Awareness report in mid-2024 with charts that sounded insane about AI demand for power. He grew his fund from $225 million to $5.5 billion since investing in stocks related to the sector but he missed something. The real bottleneck is here, Uranium & Nuclear energy via baseload power. And that’s about to ignite the uranium/nuclear supercycle. The AI Power Paradox straight from the data. Page 77 in his report- by 2030 the largest single AI training cluster alone would need 100 GW >20% of total U.S. electricity production. Page 80-Table 5, overall AI compute training + inference across everyone hits 100% of current U.S. electricity and $8 T annual investment. Most people laughed. Now in 2026 the 2026 row he projected 1 GW clusters, 5% of U.S. power is already happening in real time. xAI Colossus, Meta Prometheus, Google campuses, Amazon nuclear-adjacent builds we’re living Leopold’s table. And the stocks that rode the first wave? Many are up 1,500% to $3500%. • NVDA GPU scaling is driving 300%+ increases in power needs every few years. H100 → Blackwell → Rubin racks now hit 100+ kW each. New chips are more efficient per FLOP, but cluster sizes are exploding so fast that total power draw still skyrockets. Some centers are postponed until they can find power. • Global data centers already consume 415 TWh annually. IEA base case: 945 TWh by 2030 which is double current levels. Some high-growth scenarios hit 1,000+ TWh even sooner. AI workloads -accelerated servers are growing 30% per year and driving almost half the increase. • Big Tech is dropping hundreds of billions in capex $130B+ in Q1 2026 alone from Microsoft, Google, Amazon, Meta. NVIDIA AI factories are city-scale: 100 MW to 1 GW+ per site. • Grids can’t keep up. Permitting, transformers 5-year backlogs, transmission bottlenecks, intermittent renewables all failing. Only reliable, always-on baseload works at this scale nuclear restarts + SMRs and nat gas. Renewables + batteries don’t cut it for 24/7 AI training/inference. Why Uranium & Nuclear Go Parabolic to $1,000/lb scenario, This is a tiny, supply-constrained market meeting explosive, urgent demand the classic squeeze setup as it has done in the cyclical past. • 85 million lb structural annual deficit (Goldman Sachs) from AI alone , 1.7B+ lbs over 20 years even with some new supply and no issues with current mines which is rare. The largest Uranium producer is establishing a reserve for new buildouts locking up cheap uranium the market expected. • U.S. reactors need 50M lbs/year. U.S. producers made <3% of that last year. Sprott Physical Uranium Trust alone now holds over 81 million lbs nearly 2 years of fuel for the entire U.S. fleet. There is a Russian Uranium ban now that really starts to take effect into 2027. • Mining lead times are 2+ years minimum even for permitted projects. You can’t just flip a switch. • Historically in the 1970s Big Oil flooded into uranium and mined hundreds of millions of lbs while America built 55 reactors in 10 years. Today? The Mag 7 and especially $NVDA ecosystem players have the capital to do the same, they’re already signing multi-GW nuclear deals Meta’s 6+ GW spree with Vistra/Oklo/TerraPower, Microsoft TMI restart, Amazon 1.9 GW PPA + SMRs, Google Kairos, etc. Securing power is now existential for AI growth. But we can now build nuclear FAR faster than the 1970s boom. SMRs (small modular reactors) are factory-built like Legos modules ship to site and assemble in 2–4 years vs 7–10+ years for traditional large reactors. -Global nuclear build out accelerating 70+ reactors under construction 400 operational 300+ permitting. DOE studies show 80% of retiring U.S. coal plants are perfect for coal-to-nuclear conversions, reuse the existing grid connections, cooling towers, switchyards, workforce, and sites for massive time/cost savings 15–35% cheaper. Advanced manufacturing, AI-optimized designs, 3D-printed components, and HALEU fuel make scaling even quicker. U.S. policy tailwinds are insane, Russian uranium banned, nuclear declared critical for national security and AI, funding for SMRs/fuel cycle, faster permitting. With U.S. national security at risk AI supremacy vs China, energy independence, powering the entire AI economy, the current administration in Washington is going all-in, executive orders streamlining NRC approvals, Defense Production Act on domestic uranium/fuel, co-locating SMRs with AI data centers, and treating nuclear as critical infrastructure. This is becoming a U.S. energy independence + GDP imperative. The Leverage Is Stupid At current $86.45/lb spot and $91.50 which is what matters most. Many U.S. producers are already profitable but have open contract windows like $UEC. • But when uranium moves to $120–$200 sustained (or higher in a true squeeze) margins explode. • $UEC at a $37 cost to produce Uranium-From $87 → $200 = +220% margin. From cycle lows? 4,000% increase in margins. • At $1,000/lb? Profit jumps to $964/lb +1,792% vs current in a 19× margin expansion. Even from low-cycle $40, it’s +24,000%. Equities will go nuclear long before the commodity fully reflects it. Uranium stocks are leveraged plays on the price of uranium- Like a 0DTE contract but more volatile. Now people hear $1,000 and think this is expensive, well Raw uranium is still a tiny fraction of total costs. Full front-end fuel, uranium + enrichment + fabrication is only 15-20% of total electricity cost for new nuclear plants and 17% for operating plants per NEI data. Raw uranium concentrate itself is less than 10% of overall generating costs (often 5-8% of LCOE or 0.377 ¢/kWh). Even at $1,000/lb, it barely moves the needle on total power price for reactors or AI data centers capital costs and buildout dominate. This is why hyperscalers and utilities can absorb parabolic uranium prices without killing economics. U.S. uranium producers combined are still smaller than meme coins. $UEC, $UUUU, $LEU and the handful with real assets/claims in Texas/Wyoming/West are sitting on billions of lbs of historic resources ready to restart once price justifies it. The 1970s Uranium claim maps are locked and loaded. This is the Global AI Power Supercycle, Leopold’s 2030 vision was the warning shot and everyone flooded to Semiconductors $SNDK +3,350% 1 year, and other forms of energy $BE+1,667% 1 year. But the market is still asleep to what baseload nuclear/uranium actually means for the next decade. Big Oil → Big Tech nuclear M&A wave incoming. Uranium equities will massively outperform the commodity itself even those that are not making any cashflow. A Uranium Squeeze is coming. The funny thing is, Leopold didn't get much traction either when he posted his paper for free, he did get hundreds of millions in funding to invest which paid off. Who else sees the power bottleneck as the next 10x leg? $NVDA made the chips. Now nuclear makes the baseload power. The Uranium squeeze is just getting started.

English

The moment daddy stopped supplying money to her she went out to expose and exaggerate

James Tate@JamesTate121

BREAKING NEWS 🆘The daughter of U.S. Republican Senator Jay Block: 🆘 "Israel pays money to my father, and he spreads propaganda. I am deeply ashamed of this situation. I believe my father has sold his soul to the devil. I hope his career ends!"

English

poorlyRICH retweetledi

Banks went from an honest speech to scamming with ansem in 25minutes

Ansem@blknoiz06

Market Bubble: EP 1 — Presented by @Polymarket x.com/i/broadcasts/1…

English

So everybody in russia korea or every other country that they live in and can do nothing about politics are bad people

Maarten Boudry@mboudry

A Belgian professor at @UGent, Marc Burgelman, answering a simple request from an Israeli colleague. No comment.

English

poorlyRICH retweetledi

Why $NOK is my next 1000% play 🎯

Listen up, while everyone’s still chasing the same 5 AI names that are already priced to perfection, Nokia just quietly turned itself into the ultimate picks-and-shovels play for the entire AI infrastructure boom. And the market is finally waking up.

Here’s why I’m calling this my biggest 10-bagger opportunity right now:

• AI-RAN + NVIDIA partnership is the real deal.

Nokia’s deep integration with NVIDIA (yes, the same NVIDIA that just dropped a massive stake) is turning radio access networks into AI-native platforms. This isn’t hype, it’s already live with BT, Elisa, NTT DOCOMO, Vodafone, and more. AI-RAN is the bridge from 5G to true AI-native 6G, and Nokia is years ahead.

• Optical & data center explosion

Q1 2026 just showed it: AI + cloud revenue up 49%. They raised their addressable AI fiber/hyperscale market forecast from 16% to 27% CAGR through 2028. Hyperscalers are spending like crazy on optical networking for AI clusters, and Nokia’s Infinera acquisition just supercharged their ability to win big.

• Earnings momentum is insane

Beat Q1 estimates, operating profit up 54%, gross margins expanding, and they reaffirmed full-year guidance while the AI tailwinds get stronger every quarter. Shares just hit a 16-year high for a reason.

• Valuation still has rocket fuel

Even after the run, Nokia trades at a fraction of pure AI plays. If it gets even a modest rerating to where AI networking peers sit (20-30x forward), we’re looking at $20–$30+ per share in the next 12-24 months , and that’s before 6G really kicks in. From here? That’s multiple 100%+ legs higher. 1000% over the cycle isn’t crazy when you’re the infrastructure backbone of the AI supercycle.

This isn’t a meme. This is Nokia executing the biggest strategic pivot in its modern history, and the numbers are finally backing it up.

I’m loading the boat.

Are you in or still sleeping on $NOK

English

poorlyRICH retweetledi

> be Sam Altman

> email Elon "you're my hero" in February 2023

> get sued by Elon 18 months later

> get called Scam Altman to 200M followers

> get $97.4B hostile takeover bid

> reply at 4:11 PM "we'll buy twitter for $9.74B"

> 34M views in a week

> court date arrives

> show up. dark suit. front row. 10 feet from the bench

> your accuser stays home

> posts four tweets instead

> one of them spells your co-founder's name "Stockman"

$134 billion on the line and the man who filed the suit couldn't be bothered to walk through the door.

BP@everyonebpup

English

poorlyRICH retweetledi

Nick Lee officially stands with Israel 🇮🇱

"They lost way more people on October 7th than we lost on 9/11"

"If what happened to them happened to the US, we would have nuked someone!"

English

poorlyRICH retweetledi

this is fire

Whop@whop

Daniel Iles is building a marketing empire from the Alaskan wilderness.

English

I swear this brian dude is proof people are more retarded than ever bro went from pedophile to political expert 😂

Brian Krassenstein@krassenstein

@WhiteHouse Yeah. No one believes this. You think Iran is just gonna call up their enemy that they’re at war with and tell them that they’re in a state of collapse? This is you panicking.

English

poorlyRICH retweetledi

🚨 JUST IN: Anthropic's own team just showed how to actually prompt Claude.

24 minutes. FREE for you. From the people who built it.

Watch it. bookmark it.

English

poorlyRICH retweetledi

This is why you will lose all your money…. Unless you listen.

Weekly Wizdom

English

@wizardofsoho @LordMasterIvan Damn but those croatian girls are fine

English

@LordMasterIvan House on the coast of Croatia is for poors ldmao

Def not ideal to be poor

English

poorlyRICH retweetledi

🇺🇸 The full manifesto of WHCD gunman Cole Allen has been obtained by the New York Post. Key takeaways:

- A 31-year-old California teacher who described himself as "half-black, half-white"

- Sent the 1,052-word document to family 10 minutes before the attack

- Targeted Trump administration officials by rank, explicitly excluded Kash Patel

- Used buckshot deliberately to minimize collateral casualties

- Described Secret Service security as "actually insane" and said he walked in with multiple weapons undetected

- "If I was an Iranian agent instead of an American citizen, I could have brought a Ma Deuce in here and no one would have noticed"

- Ended the manifesto: "It's awful. I want to throw up. Can't really recommend it. Stay in school, kids."

Full manifesto:

"Hello everybody!

So I may have given a lot of people a surprise today. Let me start off by apologizing to everyone whose trust I abused.

I apologize to my parents for saying I had an interview without specifying it was for “Most Wanted.”

I apologize to my colleagues and students for saying I had a personal emergency (by the time anyone reads this, I probably most certainly DO need to go to the ER, but can hardly call that not a self-inflicted status.)

I apologize to all of the people I traveled next to, all the workers who handled my luggage, and all the other non-targeted people at the hotel who I put in danger simply by being near.

I apologize to everyone who was abused and/or murdered before this, to all those who suffered before I was able to attempt this, to all who may still suffer after, regardless of my success or failure.

I don’t expect forgiveness, but if I could have seen any other way to get this close, I would have taken it. Again, my sincere apologies.

On to why I did any of this:

I am a citizen of the United States of America.

What my representatives do reflects on me.

And I am no longer willing to permit a pedophile, rapist, and traitor to coat my hands with his crimes.

(Well, to be completely honest, I was no longer willing a long time ago, but this is the first real opportunity I’ve had to do something about it.)

While I’m discussing this, I’ll also go over my expected rules of engagement (probably in a terrible format, but I’m not military so too bad.)

Administration officials (not including Mr. Patel): they are targets, prioritized from highest-ranking to lowest

Secret Service: they are targets only if necessary, and to be incapacitated non-lethally if possible (aka, I hope they’re wearing body armor because center mass with shotguns messes up people who *aren’t*

Hotel Security: not targets if at all possible (aka unless they shoot at me)

Capitol Police: same as Hotel Security

National Guard: same as Hotel Security

Hotel Employees: not targets at all

Guests: not targets at all

In order to minimize casualties I will also be using buckshot rather than slugs (less penetration through walls)

I would still go through most everyone here to get to the targets if it were absolutely necessary (on the basis that most people *chose* to attend a speech by a pedophile, rapist, and traitor, and are thus complicit) but I really hope it doesn’t come to that.

Rebuttals to objections:

Objection 1: As a Christian, you should turn the other cheek.

Rebuttal: Turning the other cheek is for when you yourself are oppressed. I’m not the person raped in a detention camp. I’m not the fisherman executed without trial. I’m not a schoolkid blown up or a child starved or a teenage girl abused by the many criminals in this administration.

Turning the other cheek when *someone else* is oppressed is not Christian behavior; it is complicity in the oppressor’s crimes.

Objection 2: This is not a convenient time for you to do this.

Rebuttal: I need whoever thinks this way to take a couple minutes and realize that the world isn’t about them. Do you think that when I see someone raped or murdered or abused, I should walk on by because it would be “inconvenient” for people who aren’t the victim?

This was the best timing and chance of success I could come up with.

Objection 3: You didn’t get them all.

Rebuttal: Gotta start somewhere.

Objection 4: As a half-black, half-white person, you shouldn’t be the one doing this.

Rebuttal: I don’t see anyone else picking up the slack

Objection 5: Yield unto Caesar what is Caesar’s.

Rebuttal: The United States of America are ruled by the law, not by any one or several people. In so far as representatives and judges do not follow the law, no one is required to yield them anything so unlawfully ordered.

I would also like to extend my appreciation to a great many people since I will not be likely to be able to talk with them again (unless the Secret Service is *astoundingly* incompetent.)

Thank you to my family, both personal and church, for your love over these 31 years.

Thank you to my friends, for your companionship over many years.

Thank you to my colleagues over many jobs, for your positivity and professionalism.

Thank you to my students for your enthusiasm and love of learning.

Thank you to the many acquaintances I’ve met, in person and online, for short interactions and long-term relationships, for your perspectives and inspiration.

Thank you all for everything.

Sincerely,

Cole “coldForce” “Friendly Federal Assassin” Allen

PS: Ok now that all the sappy stuff is done, what the hell is the Secret Service doing? Sorry, gonna rant a bit here and drop the formal tone.

Like, I expected security cameras at every bend, bugged hotel rooms, armed agents every 10 feet, metal detectors out the wazoo.

What I got (who knows, maybe they’re pranking me!) is nothing.

No damn security.

Not in transport.

Not in the hotel.

Not in the event.

Like, the one thing that I immediately noticed walking into the hotel is the sense of arrogance.

I walk in with multiple weapons and not a single person there considers the possibility that I could be a threat.

The security at the event is all outside, focused on protestors and current arrivals, because apparently no one thought about what happens if someone checks in the day before.

Like, this level of incompetence is insane, and I very sincerely hope it’s corrected by the time this country gets actually competent leadership again.

Like, if I was an Iranian agent, instead of an American citizen, I could have brought a damn Ma Deuce in here and no one would have noticed shit.

Actually insane.

Oh and if anyone is curious is how doing something like feels: it’s awful. I want to throw up; I want to cry for all the things I wanted to do and never will, for all the people whose trust this betrays; I experience rage thinking about everything this administration has done.

Can’t really recommend it! Stay in school, kids."

Source: New York Post

Mario Nawfal@MarioNawfal

Cole Allen in his manifesto: "I am no longer willing to permit a pedophile, rapist, and traitor to coat my hands with his crimes."

English