Van Zyl Fourie retweetledi

Van Zyl Fourie

697 posts

Van Zyl Fourie retweetledi

$META $12B deal with $NBIS implies ~200 MW of AI data center capacity — about $60M per MW.

If the additional $15B expansion option is exercised, total capacity rises to roughly 430–460 MW.

Now apply that same math to $IREN 🤯

$IREN is projected to have 1,400 MW of power capacity by 2026.

Using the same $60M/MW benchmark:

1,400 MW × $60M/MW = ~$84B implied AI capacity value

Estimated range: $82B–$88B

That’s the potential scale of hyperscaler AI infrastructure deals $IREN could support.

And remember — $IREN reaches 1,400 MW in 2026, not 2027 ✅

Even a $40B hyperscaler deal could materially re-rate the company.

An $80B+ scenario would be on an entirely different level.

English

Van Zyl Fourie retweetledi

$IREN just dropped the biggest news of 2026 for AI infrastructure.

50,000 NVIDIA B300 GPUs secured. Total fleet: 150,000 GPUs.

Let me walk you through why this is MORE bullish than the headline suggests:

The Texas angle nobody’s talking about:

A portion of these B300s are being deployed in Childress, Texas.

That’s where $IREN already has 450 MW of FULLY OPERATIONAL data center capacity sitting ready.

Here’s what makes this insane:

Most air-cooled data centers cap out at 20-30 kW rack density. That’s barely enough for Hopper-generation chips. B300s require 60-70 kW.

$IREN’s Canadian sites run at 80 kW rack density. Record-breaking.

Now they’re bringing that same air-cooled Blackwell capability to Texas.

That’s a capability almost NO other cloud provider can replicate at scale.

The $9.3B war chest signals everything:

$IREN secured $9.3 BILLION in funding over the last 8 months.

They’re buying 50,000 B300s BEFORE all the customer contracts are signed.

In a supply-constrained GPU market, you don’t pull that trigger unless:

> You have term sheets in progress with hyperscalers

> You have strong demand signals from enterprise clients

> You know something the market doesn’t yet

Early hardware procurement = guaranteed deployment timelines for future clients.

That’s the whole game in AI infrastructure right now.

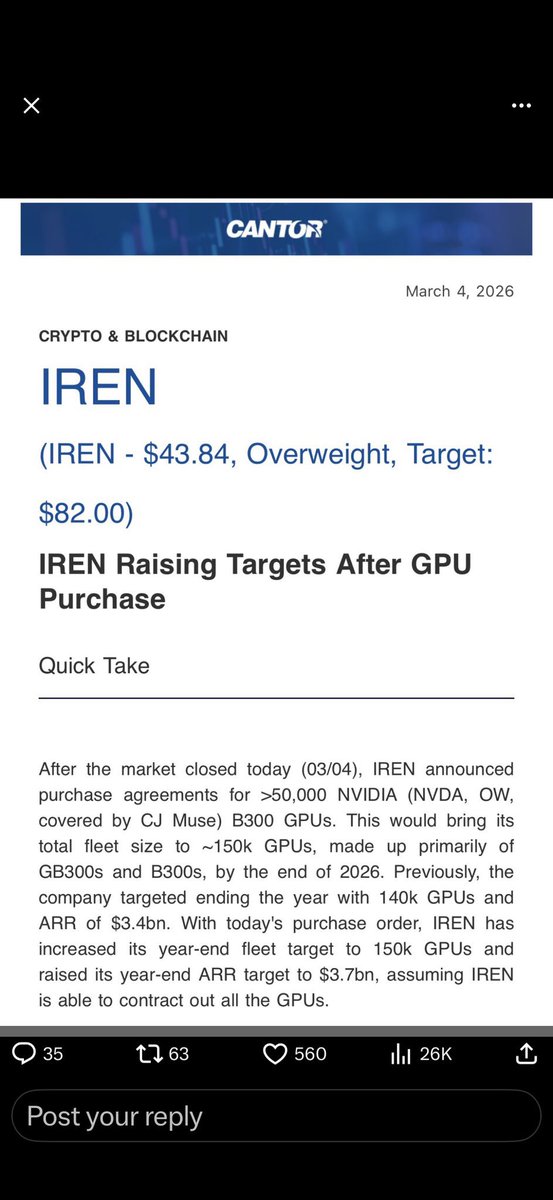

Cantor just raised their price target to $82 (Overweight).

From $43.84 today. That’s 87% upside from a bank that’s been right on $IREN before.

Their reasoning? The 150k GPU fleet now supports $3.7B ARR by end of 2026.

Up from $3.4B previously.

Now let’s talk about the ATM offering and why bears are wrong about it:

$IREN filed a new At-The-Market equity program allowing up to $6 BILLION in share sales.

Bears see dilution. I see the playbook.

Here’s the thing:

ATM offerings aren’t dumping shares. They sell gradually, opportunistically, at market prices, usually in small tranches when the stock is strong.

$IREN already used the previous $1B ATM fully. They raised $1B without crashing the stock.

Why? Because the capital is immediately deployed into assets generating REAL cash flow.

The $6B ATM isn’t a red flag. It’s the funding mechanism for $3.5B in additional capex needed to deploy these 150,000 GPUs by year-end 2026.

You can’t build the largest AI infrastructure platform on the planet without capital. This IS the capital structure.

The bottom line:

$IREN went from Bitcoin miner → 150,000 GPU AI infrastructure giant in under two years.

They have the power. They have the hardware. They have $9.3B in funding.

And within the next few weeks (April/latest May), I’d expect a major new cloud contract announcement tied directly to these 50k B300s.

The hardware gets bought first. The deal gets announced second.

$IREN to $150 is no longer a moonshot. It’s the base case.

Note. This is not financial advice.

𝒰𝓂𝒷𝒾𝓈𝒶𝓂@Umbisam

$IREN Launching A Monster $6B ATM … Wow.

English

Van Zyl Fourie retweetledi

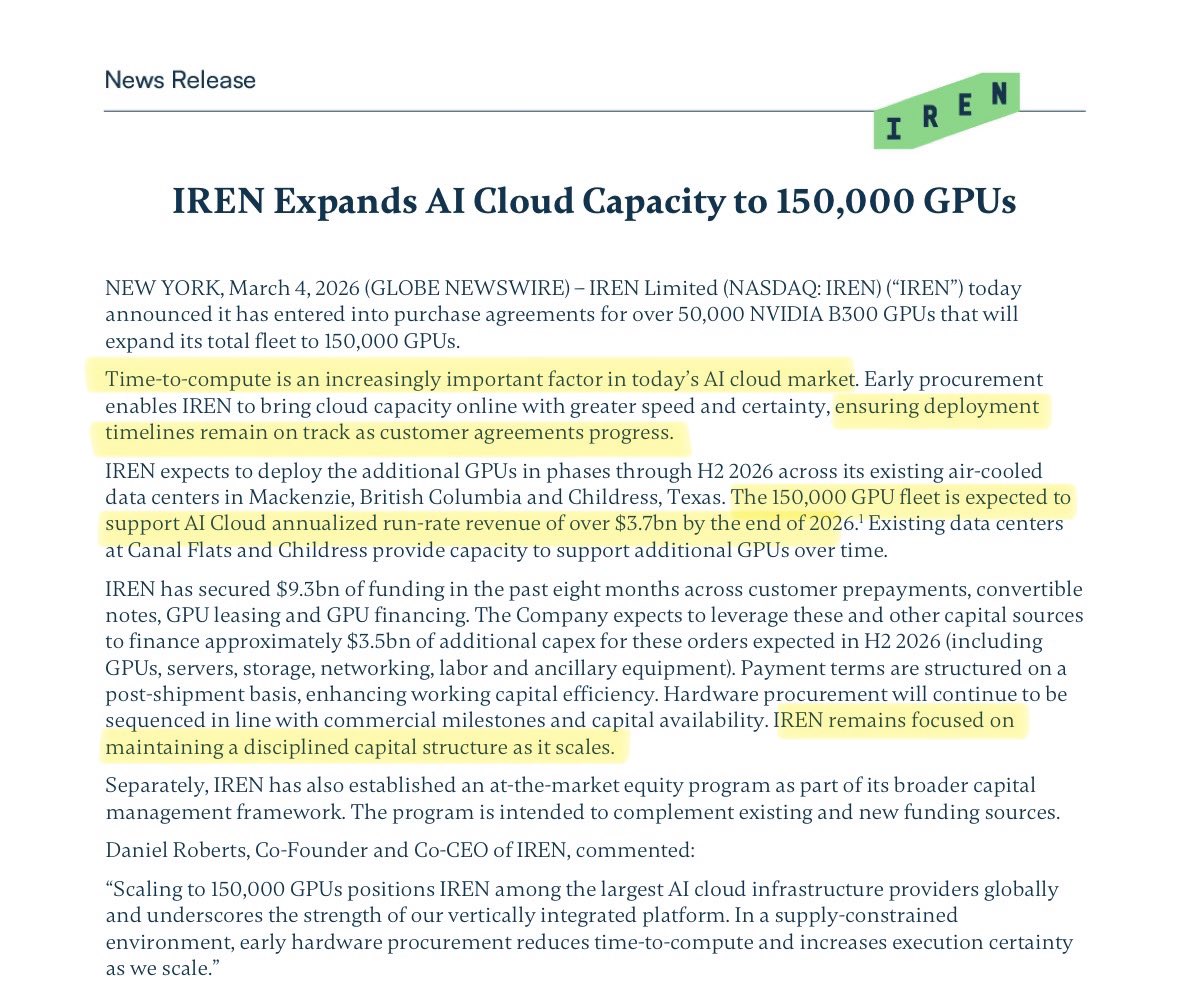

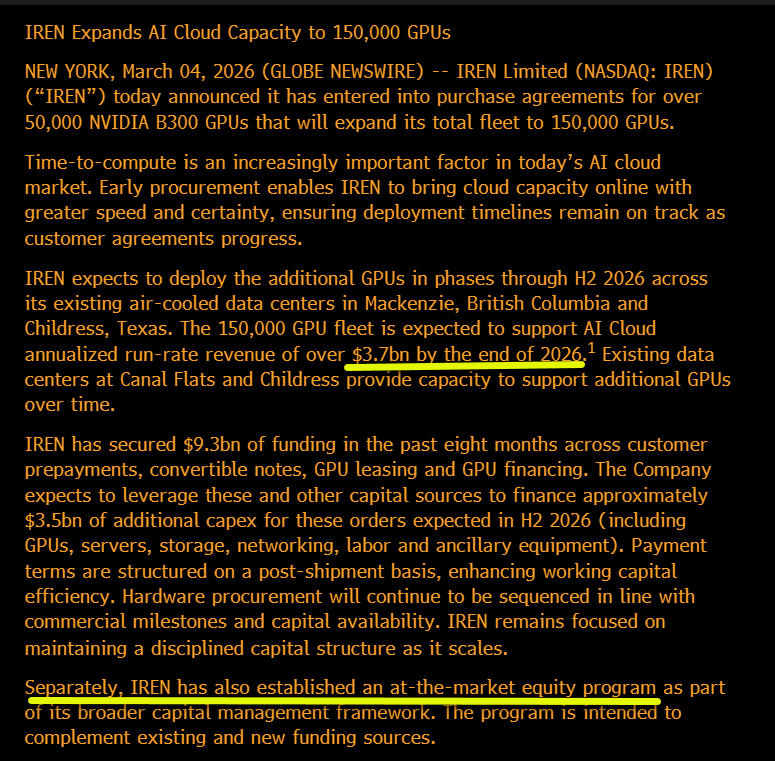

$IREN expands AI cloud capacity to 150K GPUs, says can support $3.7B ARR by end of 2026.

Also announces a new ATM but no details on size.

English

Van Zyl Fourie retweetledi

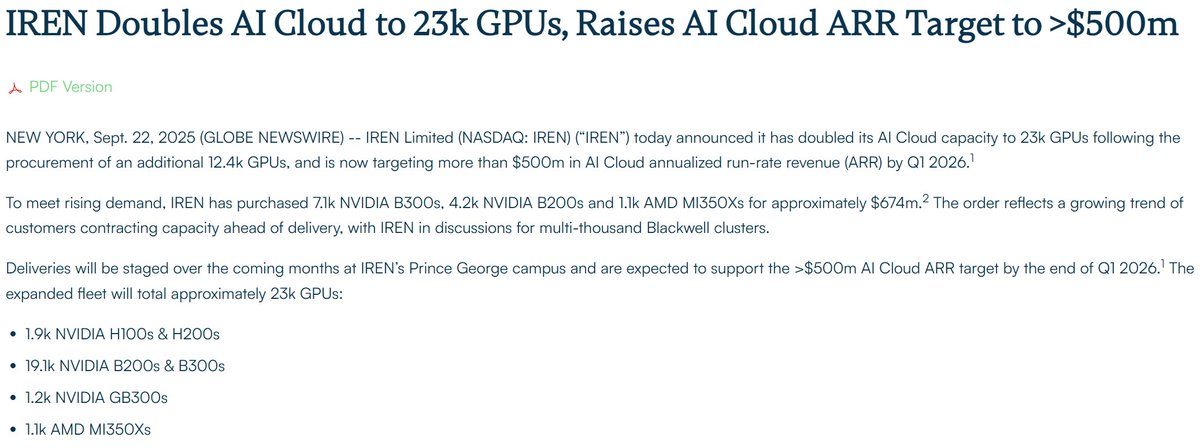

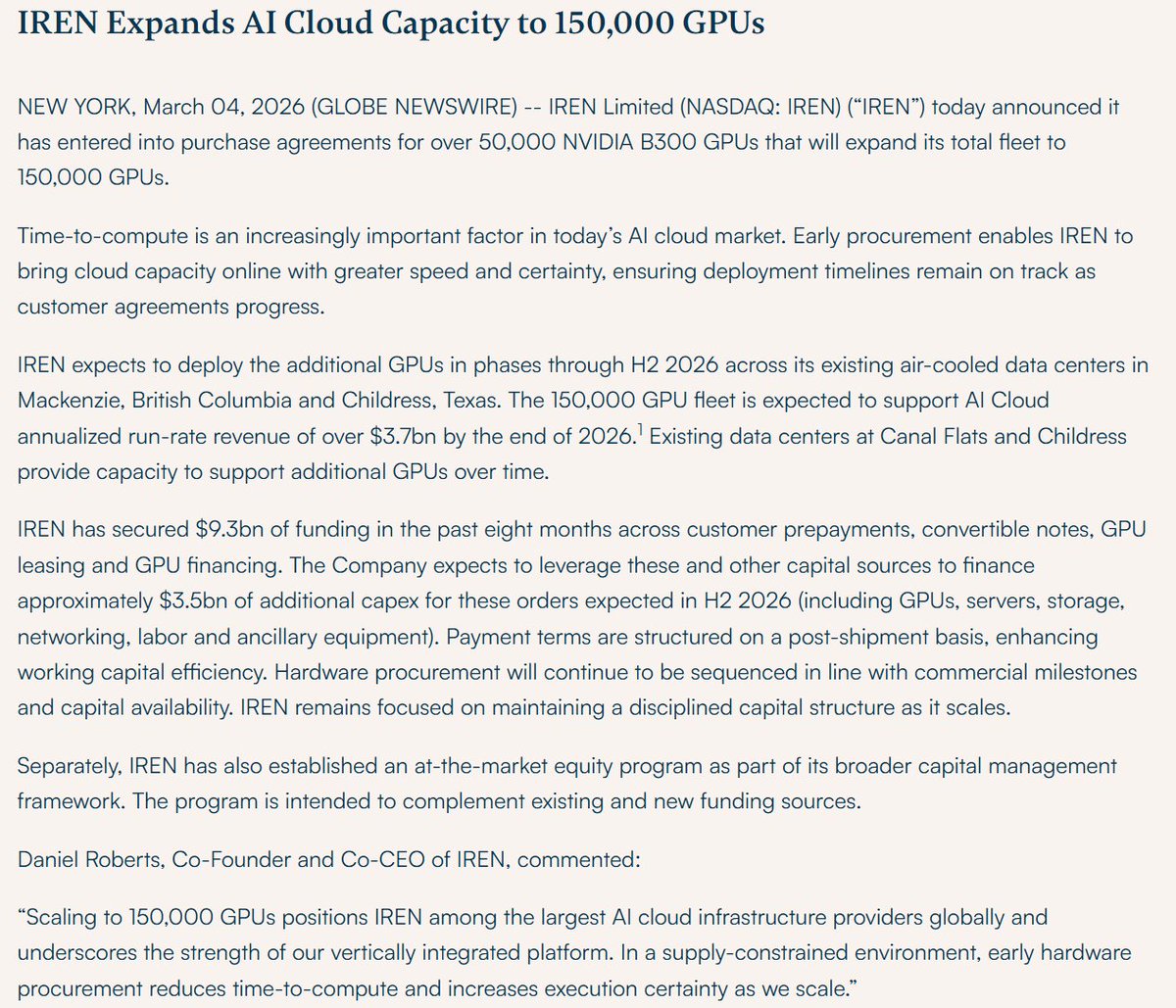

$iren Press Release Reaction 3.04.25

1. 50,000 B300s purchased; note that as of 9/22/25 the company had just under 24k GPUs to go with the 76k GPUs for the $msft deal on 11/3/25 for ~100k total.

2. Company previously guided $3.4B for 140k GPUs for 2026, but this now increases guidance to $3.7B for 150k GPUs. There's a net increase of $300m ARR and 10k GPUs.

3. Existing data centers at Canal Flats and Childress provide capacity to support additional GPUs over time.

Yes! Air cool DCs in Texas for B300s likely for inference and RDHx or liquid cooled racks will maximize the cooling to accompany the fan cooling. This is the most under appreciated part of the release. Likely $3-4m/MW retrofit vs $9-11m/MW for a brand new liquid cooled DC. No teardown and rebuild; just a retrofit before plugging in the GPUs

4. $3.5B purchase price equals $70k per GPU for B300, well over the historical prices of ~$55-60k but the company addresses GPU sourcing concerns and the rate environment is favorable for pricing.

Per 8-K, it appears $2.3B will be sent to Canada while the remaining $1.2B will be sent to Childress.

5. Separately, IREN has also established an at-the-market equity program as part of its broader capital management framework. The program is intended to complement existing and new funding sources.

A lot of investors are spooked by the $6B ATM which does represent a substantial portion of $iren market cap. This replaces the previous $1B ATM from August 2025 that got fully utilized. Notice how the press release reads separately, meaning the GPUs are not associated with the ATM.

An ATM of that size can only mean one thing to me; Sweetwater. Why else would @danroberts0101 @mikealfred subject themselves and IR to the burden of explaining funding of this magnitude without a good reason?

I personally believe this serves as some sort of assurance to their prospective partner that a new deal will not get off track if debt cannot be immediately secured.

Let the skeptics chirp. Head down and keep moving forward.

Deal(s) soon.

English

Van Zyl Fourie retweetledi

🚨 $META SIGNS MULTI YEAR DEAL WITH $AMD TO BUILD OUT 6 GIGAWATTS OF AMD GPUS

AI INFRASTRUCTURE 📈

English

Van Zyl Fourie retweetledi

🚨JUST IN: WELLS FARGO EXPECTS HYPERSCALER COMPUTE CAPACITY TO DOUBLE BY 2027

2027: 98 GW

2028: 125 GW

English

Van Zyl Fourie retweetledi

🚨 Citi, Goldman Sachs, and Morgan Stanley joined the top 5 largest shareholders of $IREN for the first time in the company’s history.

Q4:

$C: $415M > Increased by 53%.

$GS: $309M Increased by 233%.

$MS: $308M Increased by 63%

🔥🔥🔥

English

Van Zyl Fourie retweetledi

$IREN at $45: The setup everyone's missing while waiting for "The next deal".

Seeing so much impatience in $IREN replies lately.

Stock went from $70 ATH to $30, recovered to $45, and now everyone's sitting around waiting for "the next Microsoft deal."

Meanwhile, they're COMPLETY MISSING what's actually happening:

Microsoft didn't pay $9.7 BILLION over five years because they're uncertain about AI demand.

Think about what that deal actually means:

$MSFT is literally PRE-PAYING for GPU capacity that doesn't even exist yet.

They're not buying chips from $NVDA. They're buying POWER + INFRASTRUCTURE + LIQUID-COOLED DATA CENTERS.

Why? Because they've done the math:

• You can order 100,000 H100s from Nvidia tomorrow

• But you CAN'T build a GW data center in 6 months

• It takes 3-5 YEARS to get power infrastructure built

• And you need liquid cooling for Blackwell (120-140kW per rack)

The Microsoft deal uses only 10% of IREN's 4.5GW secured power capacity.

Let me repeat that.

They signed a $9.7 BILLION contract using 10% of their total capacity.

That means they have 90% MORE room to sign similar deals AFTER Microsoft.

The real constraint isn't GPUs, it's POWER:

BlackRock literally said it themselves: "The real constraint isn't chips, it's LAND and ENERGY."

$IREN controls:

> 4.5GW of secured power (largest in the sector)

> 100% renewable energy (ESG moat for hyperscalers)

> Freehold land with grid connections already built

> Liquid-cooled infrastructure ready for GB300/Blackwell Ultra

You can't just "build more power" in 6 months. This takes YEARS.

Meanwhile AI compute demand is exploding and every hyperscaler needs capacity NOW.

While competitors lease space from third-party colos, $IREN owns the entire stack:

• Develops greenfield sites

• Engineers high-voltage infrastructure

• Operates proprietary liquid-cooled data centers

• Owns the GPU fleet (high margin GaaS model)

This isn't colocation. This is vertically integrated cloud infrastructure.

Childress: The 750MW AI Flagship

Phases 1-4 (500MW): Fully operational supporting 50 EH/s Bitcoin mining.

Horizon 1-4 (200MW IT load each): Liquid-cooled facilities supporting 200kW per rack.

The Horizon series is specifically engineered for NVIDIA GB300 Blackwell Ultra—the exact chips Microsoft needs for 100MW superclusters.

Traditional data centers struggle above 20kW per rack. IREN does 200kW per rack.

That's a 10x density advantage.

Sweetwater: The 2GW Hyperscale Monster

While everyone obsesses over the Microsoft deal, Sweetwater is quietly becoming the most important site:

• 2GW+ of secured grid connections

• 6ms latency to Dallas (critical for AI inference)

• 200+ days of free cooling per year (massively reduces PUE)

• Multiple high-bandwidth fiber paths

Sweetwater 1 (1.4GW): Substation energization April 26

Sweetwater 2 (600MW): Energization late 27

This is hyperscale infrastructure on par with anything $AMZN or $GOOGL operates.

Here's what bears don't understand:

Management just paused mining expansion at 50 EH/s because the risk-adjusted returns on liquid-cooled AI data centers are BETTER than additional ASIC deployments.

That's capital discipline, not weakness.

The revenue:

> FY24: $187M revenue

> FY25: $501M revenue (168% growth)

> Q1 FY26: $240M revenue (355% YoY growth)

> AI Cloud revenue in Q1 FY26: $7.3M

That number is going from $7M → hundreds of millions as the 140,000 GPU fleet scales through 2026.

Target ARR by end of 2026: $3.4 BILLION

That's not speculation. That's contracted revenue from Microsoft + Together AI + Fluidstack.

The GPU setup:

> Current fleet: 23,000 GPUs

> Target fleet: 140,000 GPUs by end of 2026

How they're funding it:

20% upfront prepayment from Microsoft ($1.94B)

$3.6B asset-backed GPU financing (below 6% interest rate)

Zero equity dilution or high-yield debt for the buildout

That prepayment covers 95% of initial GPU CapEx.

Microsoft is literally paying $IREN to build the infrastructure Microsoft needs.

The valuation disconnect:

At $3.4B ARR with 85% EBITDA margins (per management guidance): EBITDA: ~$2.89 BILLION annually

At 15-20x EBITDA (STANDARD for infrastructure):

> Market cap: $43B - $58B

> Current market cap: ~$13B

From $45/share, that's 5-6x upside if they execute.

And remember: the $3.4B ARR target ONLY uses 10% of their 4.5GW capacity.

What happens when they announce deal #2? Deal #3?

Each additional hyperscaler contract; $AMZN, $GOOG, $META could add BILLIONS more in ARR.

At the moment it's like everyone's waiting for the next deal announcement instead of realizing what they already have:

> $9.7B Microsoft contract (5 years of revenue visibility)

> $2.8B cash on hand (no liquidity risk)

> 4.5GW secured power (90% unutilized)

50 EH/s mining generating ~$588M EBITDA annually

Path to $3.4B ARR by end of 2026

The "next deal" isn't the catalyst. Execution on the existing backlog is.

As the 140,000 GPU fleet comes online through 2026, revenue will scale from hundreds of millions to BILLIONS.

THAT's when the market re-rates this from "Bitcoin miner" to "AI infrastructure platform."

And no, of course, this isn't risk-free:

> ERCOT grid regulation changes

> Construction delays (building 2GW is massive engineering)

> Technology obsolescence (Blackwell → Rubin risk)

> Execution risk (scaling from $500M to $3.4B ARR)

> Transformer delivery delays

But here's the thing:

The Microsoft contract is FIVE YEARS with prepayment protection.

Even if newer chips come out, Microsoft is locked in paying for capacity regardless of hardware cycles.

The bottom line:

> $IREN at $45.

> 2026 ARR target: $3.4B

> Only 10% of power capacity utilized)

> Cash: $2.8B (fully funded through buildout)

> EBITDA potential: ~$2.89B (85% margins on AI cloud)

> Bitcoin mining: ~$588M annual EBITDA (cash flow)

> Power capacity: 4.5GW secured

> 90% available for future deals

The market is pricing in execution risk.

I'm pricing in the fact that $MSFT, $META, $GOOGL, $AMZN are in a literal arms race for GPU capacity and there are only a handful of companies globally that can deliver gigawatt-scale, liquid-cooled infrastructure.

$IREN is one of them.

The Microsoft deal wasn't a one-time event. It was proof of concept that $IREN's vertical integration model works at hyperscale.

-BP

Note: This is NOT financial advice.

English

Van Zyl Fourie retweetledi

Here's the best stocks to buy for 2026

1. NuScale $SMR

2. Oklo $OKLO

3. IREN $IREN

4. Archer $ACHR

5. Richtech $RR

6. Plug Power $PLUG

7. Eos Energy $EOSE

8. BigBear $BBAI

9. Ondas $ONDS

10. Joby $JOBY

$BNRG $NRXP $WBA $DTIL $ANNA $MVST $ATIF $CEG $JYD $AMST $GDTC $AMPX $AXGN

TheRealShortSqueezy@TheShortSqueezy

$RXT moving higher after this AI headline 🚀 “Rackspace Technology Announces Strategic Partnership with Palantir to Deploy and Manage Foundry and AIP Across Private and Sovereign Clouds.” Rackspace will deploy/manage Palantir’s Foundry + AIP across private and sovereign clouds, scaling its Palantir-trained team from 30 to 250+ in 12 months. Impacts: • Expands deeper into enterprise AI services • Strengthens sovereign/regulatory cloud positioning • Potential for higher-margin, long-term contracts • Signals expected demand with aggressive team buildout 📈 1.00$ currently $AMZN $GOOGL $MSFT $IBM $ORCL $CSCO $NTNX $DELL $ACN $HPE

English

Van Zyl Fourie retweetledi

🚨Goldman Sachs & Morgan Stanley stakes in $IREN jumped from 2.2M to 7.3M shares and 4.5M to to 7.3M shares totaling over 14M shares this quarter.

The Tech Investor@TheTechInvest

🚨 BREAKING🚨 MAREX GROUP ADDS 4.4M SHARES TO ITS $IREN STAKE COMPARED TO 12.2K SHARES IN Q3. 🔥🔥🔥 Its top increases this quarter: $TSLA $BMNR $IREN

English

Van Zyl Fourie retweetledi

$IREN CEO Dan Roberts made clear: the 2,000MW at Sweetwater is secured.

Legacy grids were not designed for hyperscaler AI workloads. Interconnection timelines are taking years, at minimum, with most players still negotiating power access. Dan reiterated IREN is secure today.

English

Van Zyl Fourie retweetledi

$IREN added to the MSCI USA Index = this is bigger than most people realize.

MSCI USA is one of the most tracked U.S. stock indexes used by institutions, mutual funds, ETFs, and passive money to build portfolios.

So when a stock gets added, it’s not just “good news”… it creates a mechanical demand effect:

✅ Index funds that track MSCI USA now must buy $IREN

✅ Large institutions benchmarking to MSCI now have to include it

✅ This often leads to fresh inflows + higher volume + stronger liquidity

In simple terms:

$IREN just got added to the “institutional shopping list.”

What can happen next?

✅ Short term: price can get support (sometimes a pop) as funds rebalance

✅ Medium term: more analyst/institution attention

✅ Long term: better credibility + wider investor base

$IREN is slowly moving from a “high-growth niche play” into a stock that big money can’t ignore.

English

Van Zyl Fourie retweetledi

🚨BREAKING🚨

BNP PARIBAS, WOLVERINE ASSET MANAGEMENT, AND LEGAL & GENERAL GROUP JUST BOUGHT 7.7M SHARES OF $IREN

🔥🔥🔥

English

Van Zyl Fourie retweetledi

Van Zyl Fourie retweetledi

$GOOGL, $MSFT, $META & $AMZN just confirmed $600B+ in 2026 CapEx.

Here’s how that money flows through the AI stack:

GPUs, Accelerators

• $AMD provides second source AI GPUs with MI300 & MI400 series

• $NVDA powers the AI accelerator layer with Blackwell shipping & Rubin in production

ASICs, TPUs, Design Services

• $MRVL provides interconnect & custom silicon for AI racks

• $ARM supplies CPU architecture across hyperscaler server fleets

• $CDNS enables hyperscaler AI chip development through EDA tools

• $AVGO builds custom AI silicon & networking ASICs for hyperscalers

• $SNPS powers hyperscaler silicon roadmaps with chip design software

Memory

• $MU supplies HBM & advanced DRAM for AI accelerators

• $SNDK supplies NAND flash for hyperscaler storage layers

• $WDC provides high capacity storage for AI data pipelines

Networking

• $CRDO supplies high speed SerDes for AI interconnect

• $COHR provides lasers & photonics for optical networking

• $ALAB delivers connectivity silicon for rack scale AI systems

• $ANET powers high speed switching inside hyperscaler AI clusters

• $GLW supplies fiber & optical materials for data center connectivity

Foundry & Advanced Packaging

• $KLAC process control for yield & reliability

• $LRCX etch & deposition tools for chip scaling

• $TSM advanced logic manufacturing for AI chips

• $AMAT wafer fab equipment for advanced nodes

• $ASML EUV lithography enabling leading edge nodes

• $AMKR advanced packaging & test for AI accelerators

• $INTC domestic foundry & advanced logic manufacturing for AI chips

AI Utility Layer

• $IREN builds down into power + compute

• $NBIS builds across the software + developer layer

• $CIFR rents out the physical layer through long-term leases

• $CRWV provides on demand GPU cloud capacity for AI workloads

Energy & Power

• $FSLR adds incremental utility scale solar capacity

• $CEG delivers nuclear baseload for large data center clusters

• $NEE builds large scale renewable capacity for grid expansion

• $VRT controls cooling & power systems inside AI data centers

• $VST supplies dispatchable power for hyperscaler grid demand

• $BE provides on site power that bypasses the grid for AI clusters

• $EOSE enables long duration storage for 24/7 data center power

• $SMR develops small modular reactors for future nuclear buildouts

• $OKLO provides “local nuclear plant” that the AI economy will require

• $GEV supplies turbines, transformers & grid hardware for grid rebuild

English

Van Zyl Fourie retweetledi

Just finished listening to $IREN earnings call.

I do not find anything that justifies such wild price action.

1. Revenue miss: AI revenue increased, and bitcoins missing revenue declined because $BTC is crashing.

2. There were deal rumours and retails didn’t get deal so selling?

And decline in BTC revenue at this point is not even the part of thesis specially when BTC is crashing.

The major part of thesis is: power + execution + funding: all of them are on track

1. Power is the constraint for AI acknowledged by Sam, Elon, Jensen, Sunder. But it’s not constraint for $IREN

2. Execution: So far everything is on track and they are adding more to the portfolio.

Funding: $3.6B financing + $1.9B MSFT prepayment.

So, I’ll just ignore the noise here.

English

Van Zyl Fourie retweetledi

$610 BILLION OF CAPEX WILL BE SPENT IN 2026 BY JUST THESE 4 COMPANIES

- Amazon $AMZN just said it expects to spend more than $200 Billion on CAPEX in 2026

- Google $GOOGL said it expects to invest ~$180 Billion on Capital Expenditures (CAPEX) in 2026 above expectations of $120B

- Meta Platforms $META said it expects to invest ~$125 Billion on CAPEX in 2026 above expectations of $110B

- Microsoft $MSFT is expected to spend ~$105B on CAPEX in 2026

English

Van Zyl Fourie retweetledi

All the hyperscalers are massively cranking up their capex for AI, and you’re selling $IREN which now has >4.5GW of SECURED power???

Thank you to all the panic sellers… I’ll keep buying more at these Black Friday prices 👍

English

Van Zyl Fourie retweetledi

$IREN today reported its Q2 FY26 results.

Key highlights:

✔️$3.6bn GPU financing secured for Microsoft contract

- Interest rate of <6% p.a.

- Together with Microsoft prepayment ($1.9bn) covers 95% of GPU-related capex

✔️Targeted 140k GPU expansion on track to deliver $3.4bn ARR by end of CY26

- Horizon 1-4 construction progressing to schedule

- British Columbia AI Cloud expansion ongoing, with ~$0.4bn ARR now under contract for Prince George and remaining contract negotiations supporting >$0.5bn ARR

✔️New 1.6GW data center campus in Oklahoma

- Increases secured grid-connected power to >4.5GW

- Grid-studies complete, with power scheduled to ramp from 2028

- Large scale site (2,000 acres) with low latency network connectivity

@danroberts0101 Co-Founder and Co-CEO of IREN, commented

“Last quarter marked meaningful progress across capacity expansion, customer engagement, and capital formation, reflecting IREN’s progress as a scaled AI Cloud platform,” said Daniel Roberts, Co-Founder and Co-CEO of IREN.

“We are seeing the strongest demand environment to date, and importantly, that demand is being met by a proven execution capability. Over several years, we have consistently delivered data center capacity on time and at scale, and that delivery track record continues to resonate with customers who value reliability alongside performance.

With more than 4.5GW of secured power, we are able to advance a broad set of opportunities in our pipeline and support the next phase of growth. Our $3.4bn ARR target represents an early stage of monetization relative to the size of our secured power portfolio, highlighting the scale of the platform we are building.”

$IREN management will host a webcast to discuss these results at 5:00pm ET today, which can be accessed here: edge.media-server.com/mmc/p/pc7vqops

English