Diane Swonk retweetledi

Read our latest overview on the global economy, written by @benshoesmith @KPMG_US; he is a senior economist working with chief economist @DianeSwonk.

kpmg.com/us/en/articles…

English

Diane Swonk

44.6K posts

@DianeSwonk

Chief Economist, @KPMG_US. Briefs Federal Reserve. Labor economist with more than 40 yrs experience in financial services & consulting . RTs not endorsements.

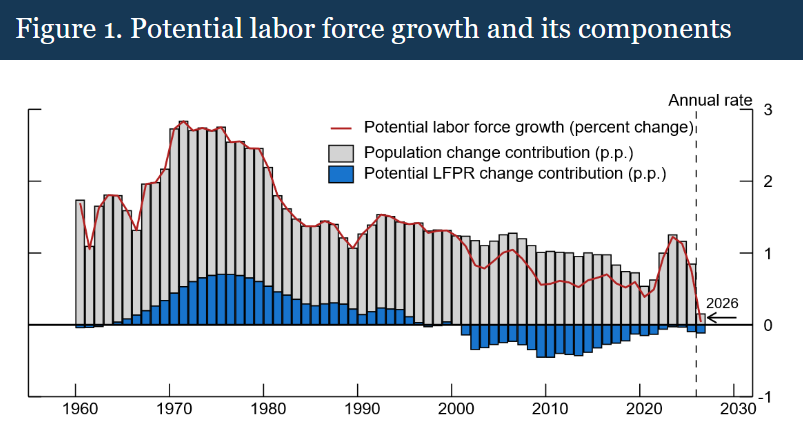

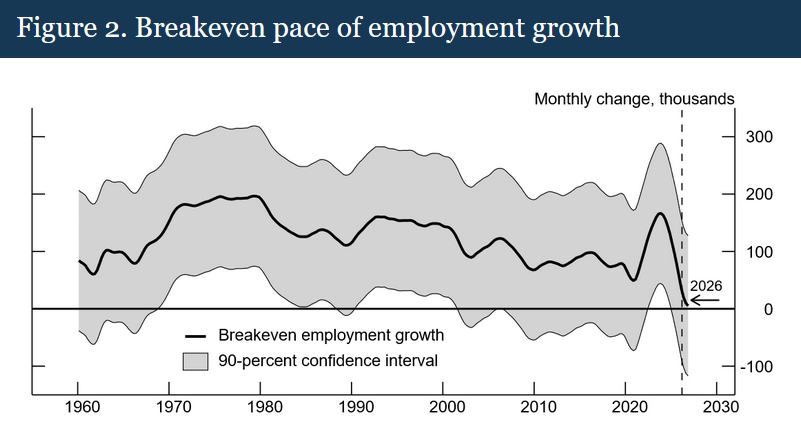

ICYMI: Labor force growth could be near-zero starting this year, due to weak population growth & declining labor force participation. Such weak growth is unprecedented in the United States’ recent history. This has significant economic implications: (1/2) federalreserve.gov/econres/notes/…

🔥The PCE index, which the Federal Reserve targets, rose 0.4% in Feb, up a tick from the 0.3% pace in Jan. That translates to 2.8% y/y, which is same as Feb. Measured of momentum accelerated. The 3 & 6-month annualized pace moved up, to 4.1% & 3.4 from 3.5% & 3.2% in Jan. Core PCE, which stips out food & energy, advanced 0.4% and cooled a bit on a y/y basis. That provide little solace to the Fed as the 3- & 6-mo annualized gains accelerated as well. Core goods prices jumped at their fastest pace since Jan 2022, as the pandemic-induced inflation gripped the economy. The jump in recreational goods - gaming and software mostly. Information goods jumped at their fastest monthly gain since December 1971. There is more in the pipeline. Import prices of computers surged in Feb. Those prices are recorded prior to tariffs, although many tech behemoths got waivers on computers and computer chips to compete better in the AI arms race. Service sector inflation cooled a bit but remains elevated and is still running more than a percent ahead of the pandemic. This is tough for the Fed. The minutes to the March meeting revealed that debate over whether the next move will be up instead of down intensified. Brace for a signal for that optionality following the Fed’s next meeting in April.

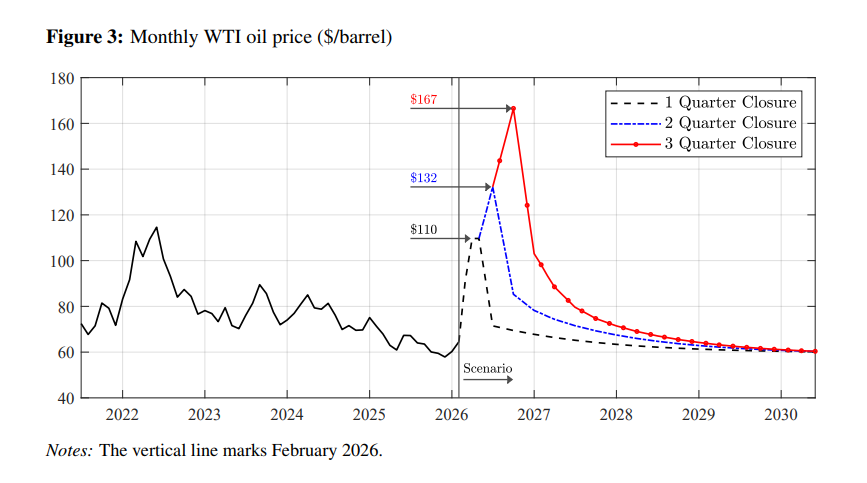

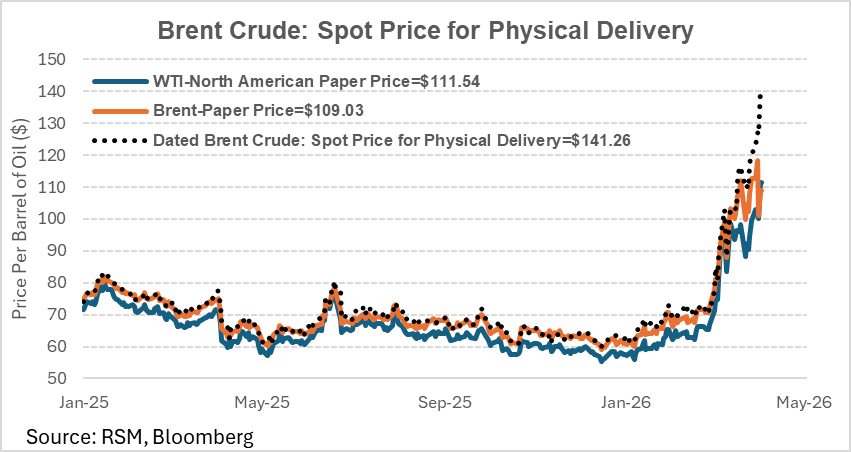

@KPMG US chief economist @DianeSwonk has crunched three different scenarios on how the oil crisis could play out for the US economy: kpmg.com/us/en/articles…

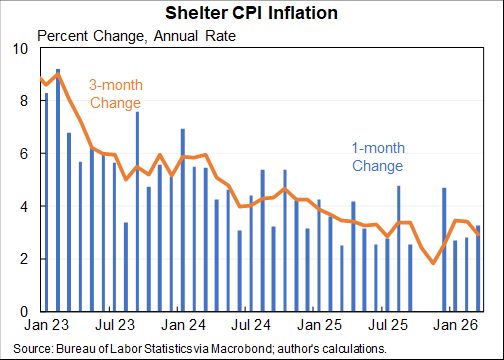

Fed research suggests the inflation engine may be running differently across advanced economies since the pandemic: 1/ More categories continue to see price growth above 3%, with broad-based wage growth in services appearing to be a key driver 2/ Even categories with flat or falling prices aren't pulling the overall number down the way they used to 3/ Pre-pandemic models consistently underpredict current inflation, suggesting the relationship between price dispersion and aggregate inflation may have shifted federalreserve.gov/econres/notes/…