Eric Maina retweetledi

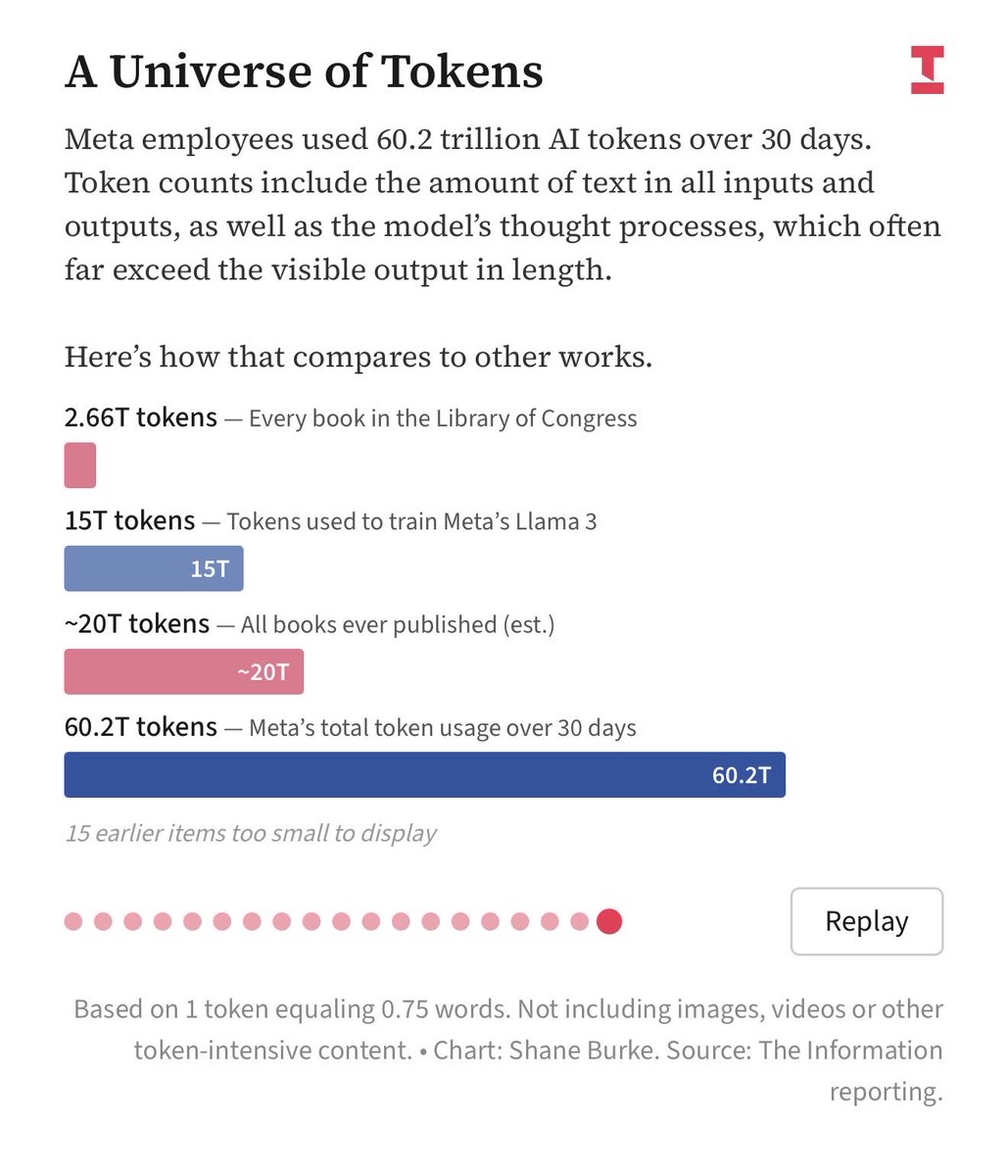

Meta is one third of Anthropic revenue?

60T tokens / mo = $900M / mo = $10B ARR for Anthropic 🤯?

This is also the largest enterprise contract in history.

English

Eric Maina

2.1K posts

@kahome_steve @MwangoCapital What do you think about about a company paying more dividends than profit made two years in a row?

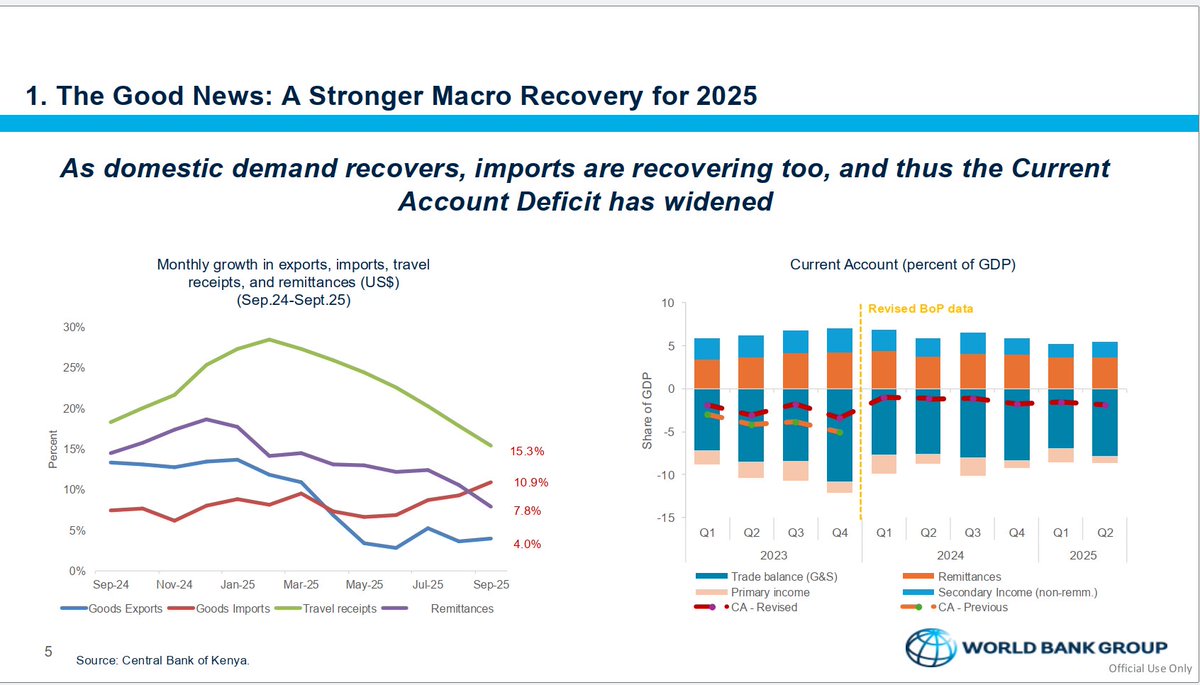

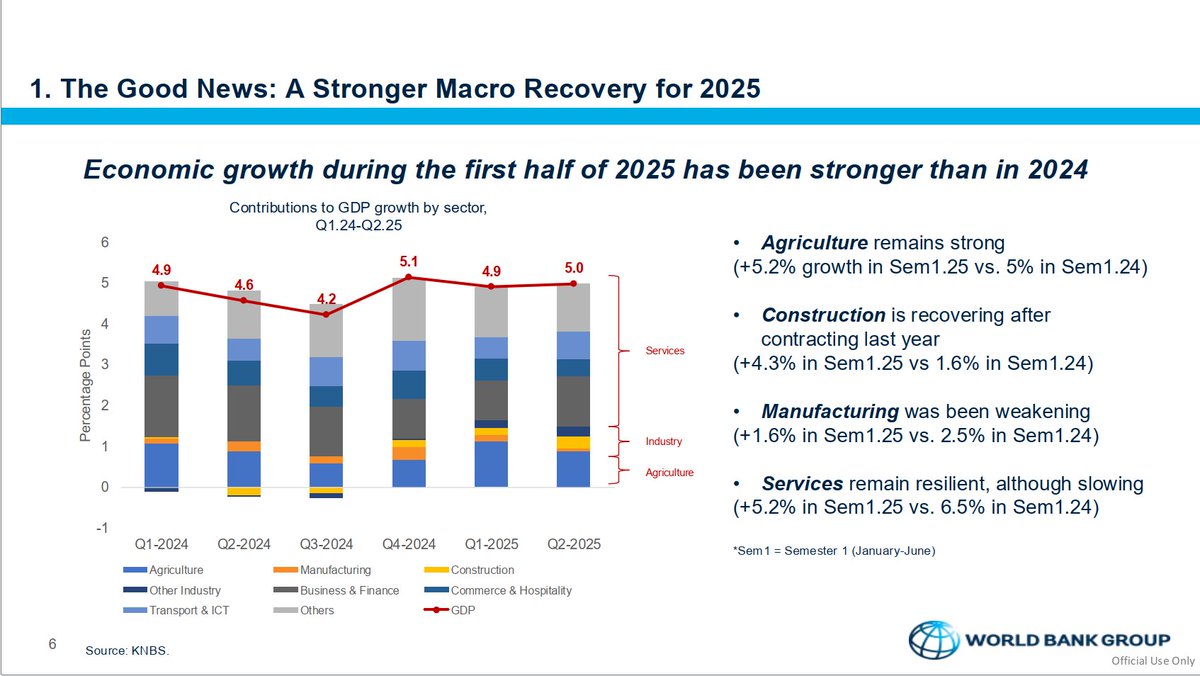

The World Bank on the good news about the Kenyan economy: —Private sector credit has improved from negative 2.9% in Feb 2025 to about 5% by Aug 2025, signalling that monetary policy transmission is working and credit conditions are normalising. —PMI recovered to above 50 in Oct 2025, ending four consecutive months of contraction and indicating a return to expansion in output, sales, and employment across surveyed firms. —Inflation has eased sharply from 6.9% in Oct 2023 to 4.7% in Oct 2025, with core components still trending downward even as volatile items (housing, utilities, transport) drive the recent uptick. —FX reserves climbed from about $7.1B to about $12.2B, lifting import cover to around 5.5 months, a historically strong position that lowers external vulnerability and boosts investor confidence. —As of Sep 2025, imports grew 10.9%, exports grew 4%, and travel receipts remained robust at 15.3%, reflecting a recovery in domestic demand and continued strength in the tourism sector. —Remittances rose 7% year-on-year as of Sep 2025, continuing to play a stabilising role for household incomes and the external account. —The current account deficit widened to 2.5% of GDP in Q2 2025, driven primarily by the rebound in domestic demand and stronger import growth rather than a deterioration in export performance. —GDP growth in the first half of 2025 was stronger than in 2024, with agriculture above 5%, services resilient, and construction posting a clear turnaround after last year’s contraction.

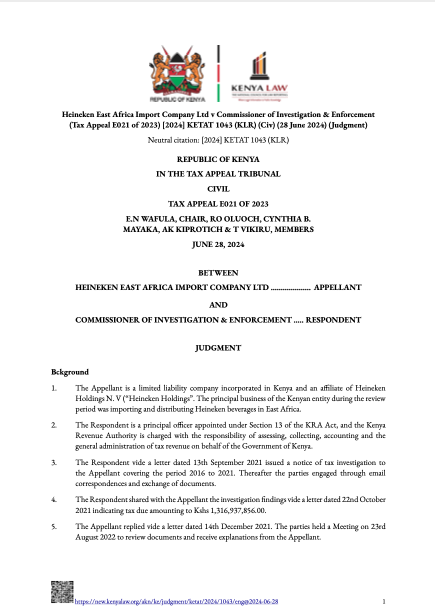

In what circumstances can KRA deem all deposits into your bank account as income & therefore taxable? The judgement on appeal E1116/2024 (Kirin Pipes Limited vs KRA Commissioner Intelligence Strategic Operations Investigations & Enforcement) before the Tax Appeals Tribunal is one I think every Kenyan needs to read. The Big Issue: · The issue at hand is a crucial one - In what instances can KRA deem all deposits into a bank account as income & therefore taxable? The Contention: · KRA conducted an investigation into Kirin Pipes Limited's tax affairs for the period 2019 - 2022 & issued assessments for income tax of Kes 34,300,288 & VAT of Kes 22,687,105 · Kirin Pipes Limited went before the Tribunal arguing that KRA made an error by assuming that every deposit made into its bank accounts amounted to income capable of being charged tax Kirin Pipes Limited's argument: · The company commenced its operations in 2019 during which shareholders injected share capital. The ordinary share capital was Kes 10.0 Million but the company required further capital & therefore shareholders deposited a further Kes 29,425,495.45 into its bank account · The company therefore argues that the deposit of Kes 29,425,495.45 was not income but capital injection · During its formative years, the company required funds to help cover the initial setup costs & operating expenses & sought for a Kes 31,697.392 loan from Nanchang Municipal Engineering Development · The company therefore argues that this deposit ought not be subjected to income tax by KRA since it was a loan · The company also argued that it received funds from its shareholders totalling Kes 24,619,662 to fund its operations & that the said amounts were not income but shareholders deposits The Verdict: · The Tax Appeals Tribunal held that Kirin Pipes Limited failed to provide an analysis of the specific deposits which related to capital injections & to link the deposits to the shareholders who are indicated in the Official Company Search (form CR12). · The Tribunal observed that Kirin Pipes Limited provided uncertified bank statements & swift confirmation slips which could not be attributed to capital deposits in the absence of other corroborative documents such as an analysis & description of the deposits, Meeting Minutes/ Resolutions or any other document to demonstrated that indeed the amounts in question were capital injections · The Tribunal held that it was incumbent upon Kirin Pipes Limited to demonstrate the flow of capital from its shareholders & how the same was eventually accounted for by the company · The Tribunal also held that Kirin Pipes Limited failed to provide evidence of the resultant shareholding structure after deposits by the said shareholders. Whereas Kirin Pipes Limited submitted form CR12, it only showed the initial capital of Kes 10.0 Million · Tribunal found that Kirin Pipes Limited failed to prove that deposits worth Kes 54,045,101.45 in its bank accounts during the period under review were attributable to capital injection from its shareholders · The Tribunal established that whereas Kirin Pipes Limited argued that a deposit worth Kes 31,697,392 was a loan from Nanchang Municipal Development Corporation, the documents indicated that it was interest free & the same could be repaid at any time at the discretion of Kirin Pipes Limited · The Tribunal held that such open terms in the loan agreement made it difficult to verify whether the amount was indeed a loan, given that there was no interest charged & neither was there a repayment period · Tribunal also pointed out that from the date the loan agreement was signed in 2019 to the date of assessments in 2024, Kirin Pipes Limited did not provide proof of any repayments it made towards the said facility · The Tribunal therefore found that the documents tabled by Kirin Pipes Limited to support its claim that Kes 31,697,392.00 of the deposits in its accounts were proceeds of a loan advanced were insufficient & did not meet the evidential threshold of disproving that the loan was income chargeable to tax · In sum the Tribunal found that KRA did not err in treading all deposits into Kirin Pipes Limited's bank account as income & therefore taxable