Sabitlenmiş Tweet

Sequent

2.6K posts

Sequent

@Sequent_

Investor 🔬 | financial freedom is the goal | stocks 📈| real estate🏡 |Not financial advice!

Katılım Mayıs 2019

36 Takip Edilen251 Takipçiler

Sequent retweetledi

$SOFI with another outstanding quarter. The market playing games due to the beat and guidance not being large enough is ridiculous. 30% growth is 30% growth.

English

$intel growing revenue at 7% y/y

$AMD 35% y/y

for my birthday I need what this “analyst” is smoking.

Hence why analyst rating should be taking as grain of salt wether against or for your thesis.

Mike@MikeLongTerm

$AMD| Addressing Downgrade- Is "clueless" & wrong This downgrade is false and misleading, here is why I understand why he is bullish on $INTC, but there is no need to spread misinformation. 1. Intel "catching up" to TSMC is overblown / packaging overflow insignificant Intel claimed 18A node reached high-volume manufacturing (HVM) in 2025, with Panther Lake CPUs shipping and PowerVia backside power delivery providing real efficiency/clock advantages on paper. Yields have improved but still much lower than $TSM. However, TSMC maintains clear leadership in scale, yields at launch (75-80%+ for N2), ecosystem maturity, and external customer reliability. TSMC's N2 capacity is sold out through 2028 with aggressive expansions (3nm to ~180k wafers/month by end-2026; 2nm ramping to 120k+). Intel Foundry remains small, loss-making ($2.5B+ quarterly drag historically), and mostly internal. For AMD specifically, if any packaging (CoWoS overflow) to Intel is niche/insignificant TSMC dominates advanced packaging (CoWoS doubling+ to ~130k wafers/month by end-2026). 2. CY27 (FY2027) consensus is way too low! Not high with hyperscalers + CPU demand undercounted I been saying this since 2024/2025, and analysts are moving forecasts slowly to my projection. Subscribers and Followers already know. Dr. Su has guided data center >60% annual growth for 3-5 years, with AI scaling to "tens of billions" by 2027, and this was before $META and many other deals. Adding only OpenAI/Meta ignores Microsoft, Amazon, Oracle, Google, Meta expansions, plus J-Curve MASSIVE EPYC CPU demand (already ~30%+ share and climbing). Recent raises ( DA Davidson +$2B on 2026 rev) reflect this. Northland's "reset too high" assumes hyperscaler discipline bites hard but 2026 CapEx signals acceleration, this slowdown CapiEx been discussed since 2024 btw and all bears were wrong. FY2026 should have digits growth due to 2025 easy comp 3. AMD earnings far more robust than Intel's (fabless advantage shines) AMD non-GAAP gross margins hold 55-57%, likely expanding to 60-65% , vs. Intel's Q1 2026 non-GAAP GM at 41.0% (up but still dragged by foundry) and GAAP operating margin deeply negative (-23.1%) from restructuring/foundry costs. Intel's non-GAAP op margin hit 12.3% (better than prior), but it's nowhere near AMD's leverage. AMD went fabless to dodge this capital intensity. Intel's recovery is real (Data Center +22% YoY), but AMD's model scales cleaner on volume, this is why Street operating leverage forecasts favor AMD heavily. 4. Higher R&D → superior chips; Jensen copying chiplets; AMD longevity, efficiency, lower TCO AMD's playbook is paying off. Aggressive R&D (as % of revenue) funded CDNA4 chiplet designs: MI350X/MI355X deliver 288GB+ HBM3E/HBM4 (vs. Blackwell ~192GB), competitive FP8/FP4, and air-cooled 750W options. Independent TCO studies show AMD 25-40% better tokens/$$ or 3-year cluster costs in inference (memory density + power efficiency). NVIDIA is shifting to chiplets (Rubin) is a direct validation. AMD GPUs often win on longevity/TCO in targeted deployments. NVIDIA still leads ecosystem/share (~80-85% AI accelerators; AMD 5-10% butdominating in inference, especially Agentic AI where Turin is a clear winner), with better MFU via CUDA. But hardware gap narrows, and AMD's price/performance edge is real. 5. AMD pricing power rising sharply (Intel hikes reversing Milan-era discounts; TSMC modest vs. Intel's big moves) Dynamic fully flipping in AMD's favor. TSMC raising advanced/sub-3nm prices 3-10% (some reports 3-7%) starting 2026, plus CoWoS hikes. Intel executed multiple server/CPU increases in 2026 (5-20%+ already; more in May and cumulative 30%+ planned). AMD following suit amid tightness, but TSMC has better cost control(only raise 3-7%), this will allow AMD to be more flexible and steal more market share Post-Milan, Intel's discounts eroded AMD's premium but they lost share anyway. Now Intel reverses while AMD benefits from TSMC efficiencies and superior products. This directly supports margin expansion and share gains in servers/AI. 6. NVIDIA supply control was 2023-2025; TSMC now separating capacity (2nm/3nm) for fairer allocation Peak shortages eased as TSMC expands aggressively (3nm/2nm sold out but ramping; CoWoS to 130k-150k wafers/month). NVIDIA/Apple take big early chunks, but TSMC allocates "fairly" to large loyal customers like @AMD (secured meaningful wafers for MI400; reports of 40-60% on certain lines). Node separation + Arizona fabs help. AMD's supply position has materially improved in 2026 toward 2030 7. OpenAI/Anthropic IPOs → push toward owning diversified hardware (including AMD) vs. pure NVIDIA rental; pressures NVIDIA margins long-term Both targeting 2026 IPOs (OpenAI potentially late-year at $800B-$1T; Anthropic earlier). NVIDIA has pulled back private investments as they go public. Hyperscalers already diversifying (Meta, Amazon, Google, Microsoft, Oracle deploying AMD Instinct at scale). IPO capital + discipline (usage caps, token pricing) will accelerate direct ownership due to lowest TCO, TDP, and $ per million token-efficient racks like AMD. OpenAI and Anthropic want to own the data center, while Jensen is pushing for more rental, which will increase Op Ex. Going public will mean more Op Ex control and rising Op Income. Conclusion: Dr. Lisa Su has delivered on both innovation and execution. Under her leadership, AMD has secured significant TSMC supply including scaled N2 capacity for MI400 series and strong CoWoS allocations starting Q1 2026 positioning the company to meet surging demand without the constraints Northland highlights. This supply security, combined with the fabless margin advantage, rising pricing power, TCO superiority, and hyperscaler diversification, directly dismantles the note’s core concerns around NVDA favoritism and 2027 resets. Northland’s caution is understandable given past cycles, but the data from capacity ramps and management commentary shows AMD is no longer the supply-constrained underdog. With MI350/MI400 ramps accelerating, EPYC share climbing, and hyperscaler CapEx still exploding, the multi-year AI + CPU opportunity looks intact and much larger than consensus assumes. May 5 earnings will likely provide fresh color on these ramps and 2026 guidance a potential catalyst for further upside. This is exactly the kind of high-quality compounder setup that rewards long-term conviction over near term noise. Not Financial Advice!

English

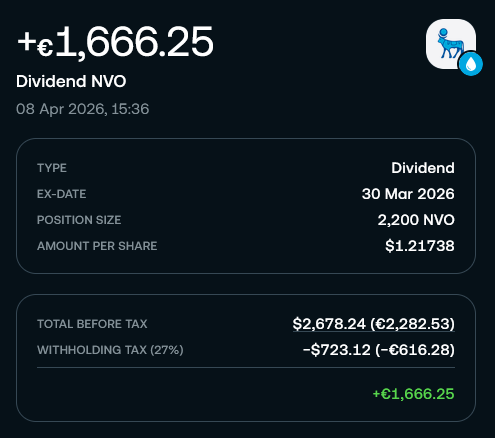

Did you get your $NVO dividend?

Did you got annihilated by the tax as well?

English

@DividendDynasty There’s hope, just give them time. Turn around is underway. Collect that dividend for your paytience.

English

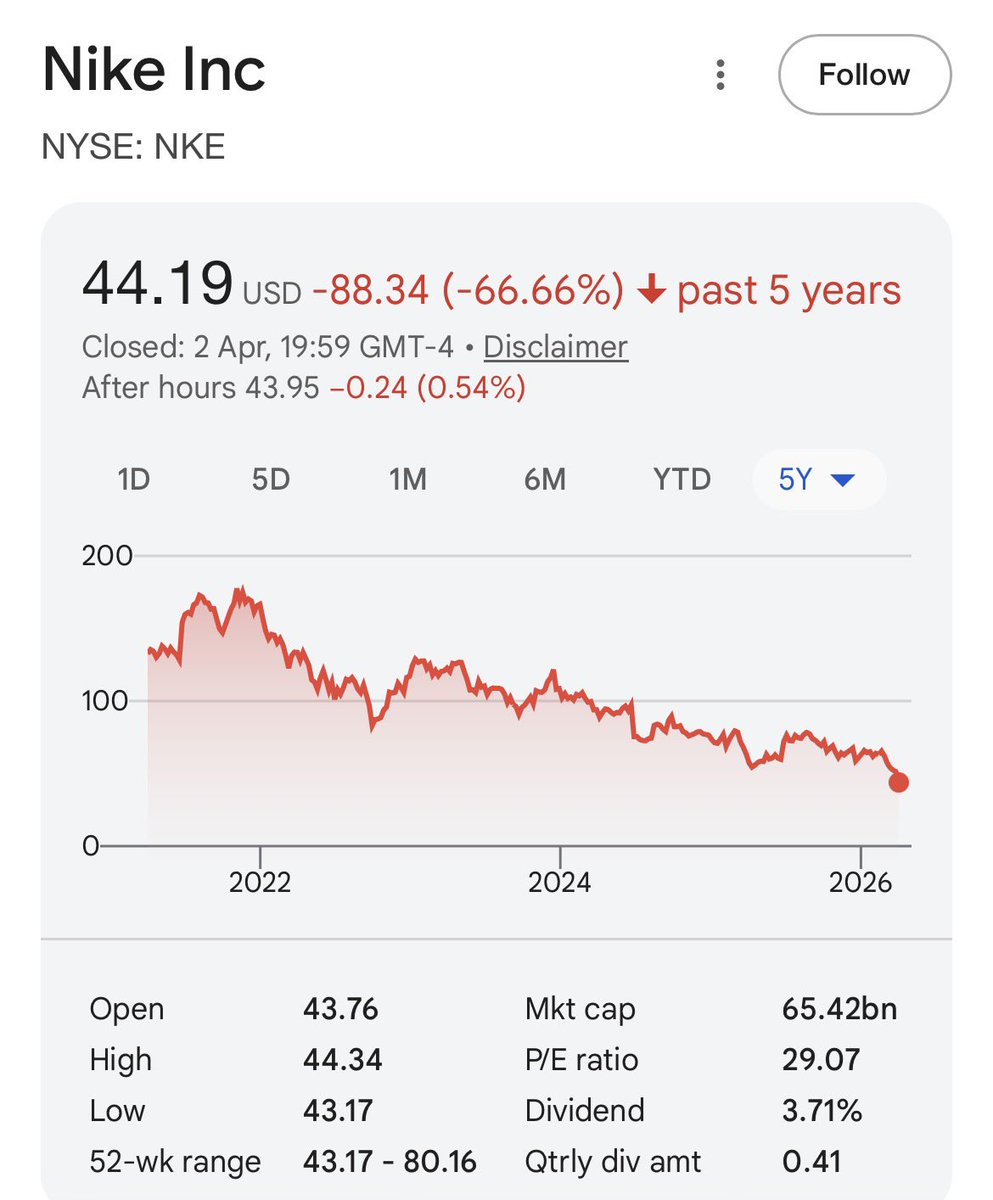

What the hell happened to $NKE 🤔

If you invested $10,000 into Nike 5 years ago, today that investment would be worth $3,530 down 64.7% 🔴

Is there any hope for $NKE shareholders here?

English

This is because I was posting about the yesterday's run-up.

Sorry $NBIS guys.

English

@DividendDynasty This isn’t the craziest thing they have posted. Thanks to all trump tards.

English

Enjoying life is more important.

Also moving to different where USD is worth more than local currency works.

The Money Buddy@The_Money_Buddy

I had a manager who said he “couldn’t afford to invest.” But he took a family $7,000 vacation every year. $7,000/year at 8% for 30 years? $792,000. We don’t lack money. We lack priorities.

English

Sequent retweetledi

BREAKING: Oil prices surge nearly +12%, to $75/barrel, as US stock market futures officially reopen.

English