…. retweetledi

….

5.3K posts

…. retweetledi

…. retweetledi

…. retweetledi

Monty Python will always be timeless.

cinesthetic.@TheCinesthetic

What movie scene do you constantly rewind and rewatch?

English

…. retweetledi

…. retweetledi

why is no one talking about this…

@

S&P 500 relative to M2 Money Supply 🚨 Dot Com Bubble vs. Now 😱👀

English

…. retweetledi

…. retweetledi

Jack Sparrow’s entrance in Pirates of the Caribbean (2003) is still one of the greatest character introductions ever.

cinesthetic.@TheCinesthetic

What is the greatest character entrance into a scene?

English

…. retweetledi

…. retweetledi

…. retweetledi

…. retweetledi

…. retweetledi

🚨: A rare blue Hibiscus has appeared in Hawaii for the first time in TEN years🪻

English

…. retweetledi

…. retweetledi

…. retweetledi

…. retweetledi

yeah im ngl the 3/3 3:33am Blood Moon Fire Horse Purim Lunar Eclipse WWIII AGI moment is frying me a lil bit

English

…. retweetledi

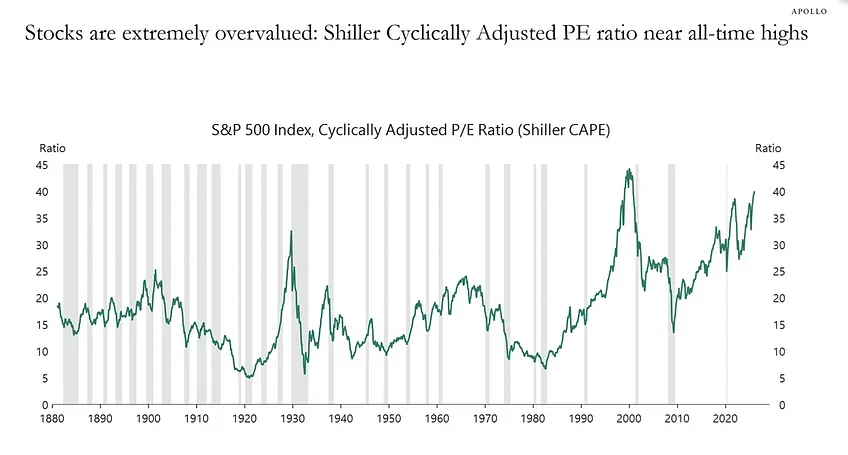

Just your daily reminder that stocks are expensive.

To put it in the context of my recent “Fee Fi FOUR Umm…” post, specifically the expected return discussion surrounding FISV, the difference between a 20% expected annualized long-term return on a common stock and an 10% one is logarithmic. The 20% return price can be 4x times the 10% expected return price and 8x the 8% expected return.

This also explains why value investors look like idiots for extended periods. When a stock trading at the 8% expected return price ($160) falls to the 10% return price ($93), it's down 42% and everyone assumes something is broken. To get to the 15% price ($38), it needs to fall 76% from that $160 level. At that point, the business is being treated as terminal. The 20% price is just where everyone wants to give up and go home. And we only see that in any widespread fashion when everyone is indeed giving up and going home - like the 2008-2009 bottom and the second half of 2002. 2020 early in COVID got close but not like that. It’s been a long, long time since it got like that.

Value investors have looked like idiots for a long, long time. Adjust the PE correctly for SBC, Depreciation, Amortization, Fixed/Capital Leases, etc, and it gets worse.

open.substack.com/pub/michaeljbu…

English

…. retweetledi

…. retweetledi