🌐 AryaFin Alternative Asset Audit | Weekly Cross-Asset Comparison

Reporting Cycle: Monday, June 1 – Friday, June 5, 2026The macroeconomic landscape transformed into a one-way liquidity vacuum by the end of the week. Friday’s explosive +172,000 Nonfarm Payrolls labor shock shifted terminal interest rate projections onto a hawkish footing, driving a massive de-risking wave across alternative asset classes.

As real yields climbed, the U.S. Dollar emerged as the singular destination for capital, systematically draining liquidity from commodities, precious metals, and digital assets.

📊 Alternative Asset Performance Matrix

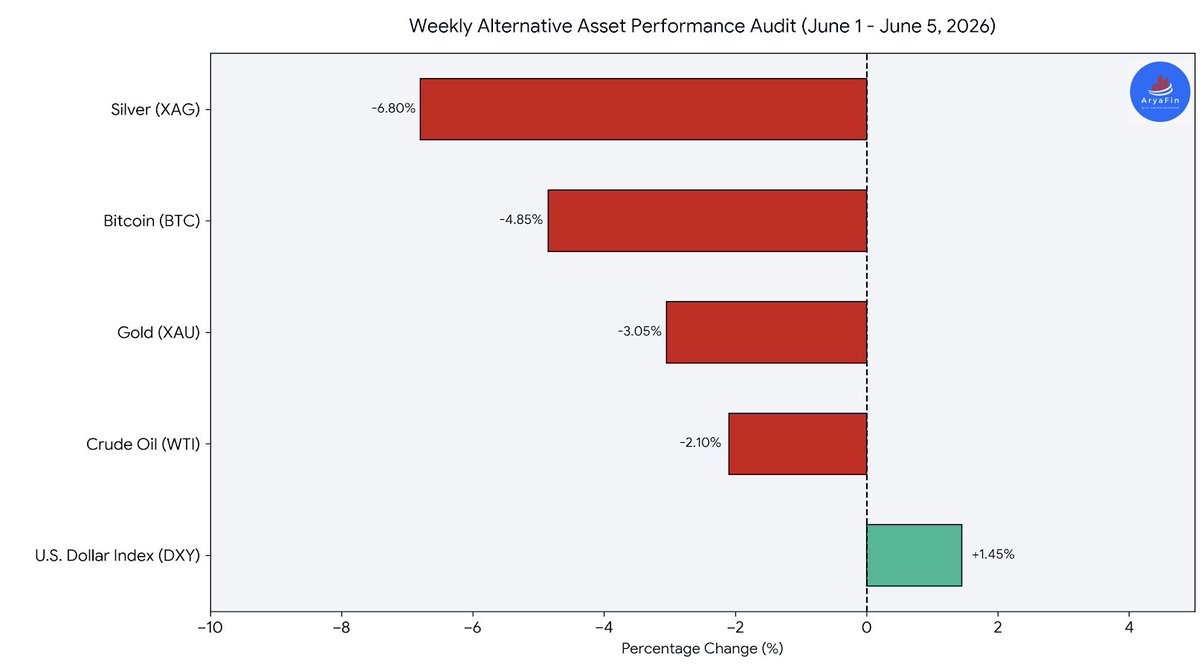

U.S. Dollar Index (DXY): 🟢 +1.45% (Weekly Leader)The greenback operated as a global liquidity vacuum. Friday's hot jobs data pushed the 10-year Treasury yield up to 4.54%, strengthening the dollar index as investors rapidly priced out near-term monetary easing.

Crude Oil (WTI): 🔴 -2.10%U.S. benchmark WTI Crude oil fell into the close, settling down at $90.54 per barrel. The combination of a stronger dollar and structural anxieties that higher interest rates would restrict intermediate industrial demand erased early-week geopolitical relief gains.

Gold (XAU): 🔴 -3.05%Spot gold faced steep liquidation, dropping over -3.2% on Friday alone to close the week at $4,331.19 per ounce. The surge in real yields severely increased the opportunity cost of holding non-yielding safe havens, breaking immediate support structures.

Bitcoin (BTC): 🔴 -4.85%The flagship digital asset extended its recent correction, down over 5% on Friday to finish at $61,897. Bitcoin's macro rate panic was compounded by an ongoing 13-day spot ETF outflow streak, sending high-beta crypto layers looking for a stable accumulation floor.

Silver (XAG): 🔴 -6.80% (Weekly Laggard)Silver functioned as a high-beta vehicle for the precious metals selloff, collapsing -7.05% on Friday to settle at $68.63 per ounce. Leveraged long positions unwound quickly despite long-term industrial demand baselines from components and solar technology.

The Read:When a single macroeconomic print blocks the path toward monetary relaxation, alternative assets re-correlate rapidly. Non-yielding tangibles (Gold and Silver), industrial growth commodities (Oil), and speculative digital stores of value (Bitcoin) all fell under pressure from the climbing dollar.

For intermediate portfolio management, preserving capital in liquid structures remains essential until real yields establish a firm equilibrium floor.

#MacroAudit #GoldPrice #SilverPlunge #BitcoinCorrection #CrudeOil #DollarStrength #AryaFin

English