FMZ Quant

406 posts

FMZ Quant

@FMZQuant

Quantitative Trading For Everyone Telegram:https://t.co/zBdP27IqO0 中文电报群:https://t.co/SKXsmTombA

Singapore Entrou em Şubat 2022

71 Seguindo1.2K Seguidores

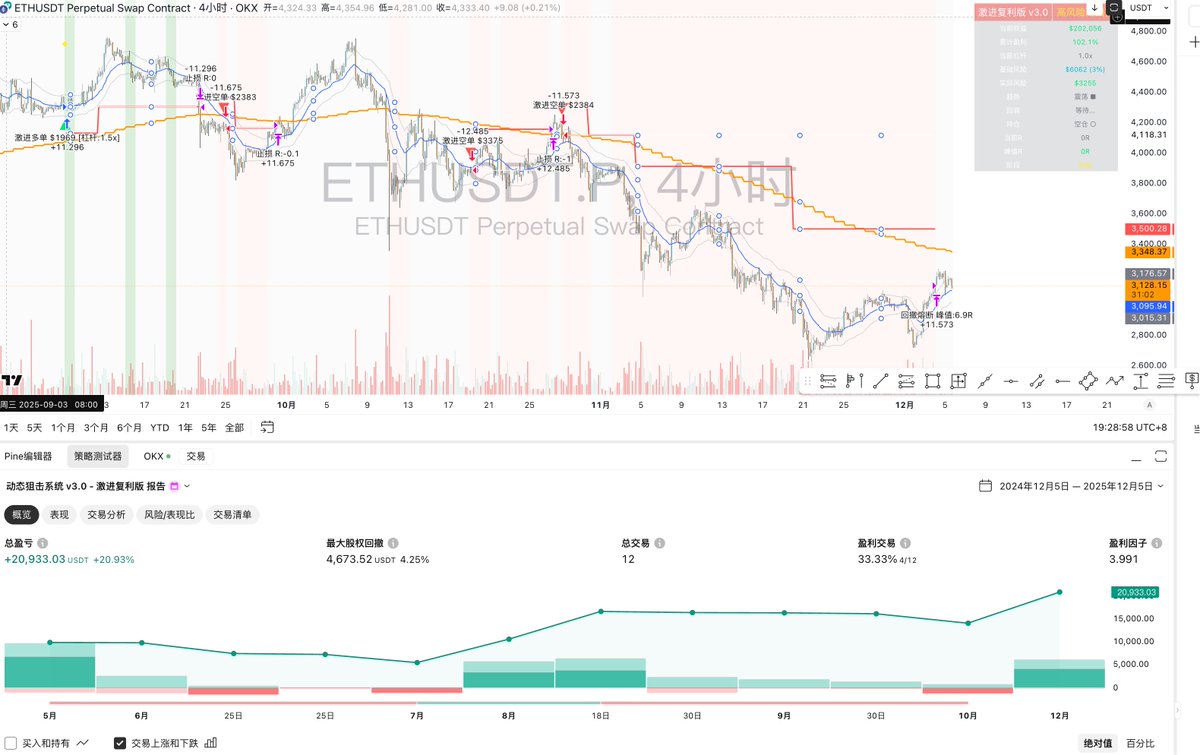

把这个代码公开了,因为okx信号策略不知道在干啥,给我断了,这个是今天刚把上面开的空单平掉了。

目前我继续跑吧,后面有变动会更新。

最近主要精力会放在搞把我的交易系统搞成《AI+交易》效果。就是各种写,把我能想到的全部写出来,顺便把我之前发布在推特的单子全部搞出来整理一下。

说一下效果:

默认名义本金10w💲,名义仓位1.5w💲,最高可开到2.5w💲

也就是1w💲十倍杠杆。理论上运气好第一单赚钱的话,2k💲就能开这个策略赚钱

如果趋势强度高了,会开1.5倍杠杆,也就是来到了15万💲的本金。

最近一年效果:大概就是一年2.5w仓位,赚2w💲。

盈利因子接近4

不说其他的了,你们自己看设置吧,反正是中文,自己调试去,希望大家一起搞一个好用的策略吧。

以下是代码👇:

//@version=5

strategy("动态狙击系统 v3.0 - 激进复利版",

overlay=true,

initial_capital=100000,

default_qty_type=strategy.fixed,

commission_type=strategy.commission.percent,

commission_value=0.075,

slippage=3,

pyramiding=0,

calc_on_every_tick=true,

process_orders_on_close=false,

max_bars_back=500)

// ==================== 激进版核心参数 ====================

// 你的激进风控配置

riskPercentage = input.float(3.0, "单笔风险比例(%)", minval=1.0, maxval=5.0, step=0.1, group="激进风控")

maxLeverage = input.float(1.5, "牛市最大杠杆倍数", minval=1.0, maxval=2.0, step=0.1, group="激进风控")

compoundingMode = input.bool(true, "启用复利模式", group="激进风控")

maxPositionPct = input.float(15.0, "最大仓位占比(%)", minval=10, maxval=25, group="激进风控")

// 你的激进止盈配置

breakEvenR = input.float(1.2, "延迟保本触发R", minval=0.8, maxval=2.0, step=0.1, group="激进止盈")

lockSmallR = input.float(3.0, "延迟锁利触发R", minval=2.0, maxval=5.0, step=0.1, group="激进止盈")

lockSmallLevel = input.float(1.0, "锁利位置R", minval=0.5, maxval=2.0, step=0.1, group="激进止盈")

lockBigR = input.float(6.0, "大利润触发R", minval=4.0, maxval=10.0, step=0.1, group="激进止盈")

lockBigLevel = input.float(3.0, "大利润位置R", minval=2.0, maxval=5.0, step=0.1, group="激进止盈")

// 利润回撤保护(激进版放宽)

useGivebackKill = input.bool(true, "启用利润回撤熔断", group="激进止盈")

givebackStartR = input.float(4.0, "回撤监控起始R", minval=3, maxval=8, step=0.5, group="激进止盈")

maxGivebackR = input.float(2.0, "最大允许回撤R", minval=1.0, maxval=4.0, step=0.5, group="激进止盈")

// 趋势过滤

trendEmaLength = input.int(50, "日线EMA周期", minval=20, maxval=100, group="趋势过滤")

trendLookback = input.int(20, "动量回看周期", minval=10, maxval=50, group="趋势过滤")

trendThreshold = input.float(5.0, "趋势阈值(%)", minval=2, maxval=15, group="趋势过滤")

// 入场设置

valueEmaLength = input.int(20, "4H EMA周期", minval=10, maxval=50, group="入场设置")

atrLength = input.int(14, "ATR周期", minval=7, maxval=21, group="入场设置")

pullbackAtrMult = input.float(1.2, "回调区ATR倍数", minval=0.5, maxval=2.0, group="入场设置")

// 止损设置

stopAtrMult = input.float(3.0, "止损ATR倍数", minval=2.0, maxval=5.0, group="风险管理")

// 激进版熔断(放宽限制)

dailyLossLimit = input.float(5.0, "日亏损熔断(%)", minval=3, maxval=8, group="熔断保护")

totalDrawdownLimit = input.float(25.0, "总回撤防御(%)", minval=15, maxval=35, group="熔断保护")

// ==================== 数据获取 ====================

// 日线数据

dailyClose = request.security(syminfo.tickerid, "D", close, lookahead=barmerge.lookahead_off)

dailyClose20Ago = request.security(syminfo.tickerid, "D", close[trendLookback], lookahead=barmerge.lookahead_off)

dailyEma50 = request.security(syminfo.tickerid, "D", ta.ema(close, trendEmaLength), lookahead=barmerge.lookahead_off)

// 当前周期数据

h4Ema20 = ta.ema(close, valueEmaLength)

h4Atr = ta.atr(atrLength)

// ==================== 趋势过滤器 ====================

trendMomentum = (dailyClose - dailyClose20Ago) / dailyClose20Ago * 100

isBullishEnv = dailyClose > dailyEma50 and trendMomentum > trendThreshold

isBearishEnv = dailyClose < dailyEma50 and trendMomentum < -trendThreshold

isNoTradeZone = not isBullishEnv and not isBearishEnv

// ==================== 回调区识别 ====================

distanceToEma = math.abs(close - h4Ema20) / h4Atr

isBullPullback = isBullishEnv and close <= h4Ema20 + pullbackAtrMult * h4Atr and close >= h4Ema20 - pullbackAtrMult * h4Atr

isBearPullback = isBearishEnv and close >= h4Ema20 - pullbackAtrMult * h4Atr and close <= h4Ema20 + pullbackAtrMult * h4Atr

// ==================== 入场信号识别 ====================

bodySize = math.abs(close - open)

upperWick = high - math.max(close, open)

lowerWick = math.min(close, open) - low

isBullishCandle = close > open

isBearishCandle = close < open

isHammer = lowerWick >= bodySize * 1.2 and upperWick < bodySize * 0.5

isShootingStar = upperWick >= bodySize * 1.2 and lowerWick < bodySize * 0.5

// 做多信号

bullSignal1 = isBullishCandle and low < h4Ema20 and close >= h4Ema20

bullSignal2 = isHammer and low < h4Ema20

bullSignal3 = isBullishCandle and close > close[1] and distanceToEma < pullbackAtrMult

bullEntrySignal = isBullPullback and (bullSignal1 or bullSignal2 or bullSignal3)

// 做空信号

bearSignal1 = isBearishCandle and high > h4Ema20 and close <= h4Ema20

bearSignal2 = isShootingStar and high > h4Ema20

bearSignal3 = isBearishCandle and close < close[1] and distanceToEma < pullbackAtrMult

bearEntrySignal = isBearPullback and (bearSignal1 or bearSignal2 or bearSignal3)

// ==================== 核心:激进复利仓位计算 ====================

// 计算累计盈利率(用于杠杆触发条件)

cumulativeProfitPct = (strategy.equity - strategy.initial_capital) / strategy.initial_capital * 100

// 复利基数:使用当前权益而非初始资金

capitalBase = compoundingMode ? strategy.equity : strategy.initial_capital

// 基础风险金额(你的3%配置)

baseRiskAmount = capitalBase * riskPercentage / 100

// 杠杆触发条件:累计盈利>10%且当前是牛市

useLeverage = compoundingMode and cumulativeProfitPct >= 10.0 and isBullishEnv

// 应用杠杆倍数

effectiveLeverage = useLeverage ? maxLeverage : 1.0

leveragedRiskAmount = baseRiskAmount * effectiveLeverage

// 止损距离

stopDistance = stopAtrMult * h4Atr

// 计算合约数量

contractSize = leveragedRiskAmount / stopDistance

// 仓位占比限制

nominalValue = contractSize * close

positionPct = nominalValue / strategy.equity * 100

// 如果超过最大仓位占比,强制缩小

if positionPct > maxPositionPct

contractSize := strategy.equity * maxPositionPct / 100 / close

// 最终合约数

finalContractSize = math.floor(contractSize * 1000) / 1000

actualRiskAmount = finalContractSize * stopDistance

// ==================== 风控熔断机制 ====================

var float dayStartEquity = strategy.initial_capital

if ta.change(time("D"))

dayStartEquity := strategy.equity

dailyPnL = strategy.equity - dayStartEquity

dailyPnLPct = dailyPnL / strategy.equity * 100

isDailyCircuitBreaker = dailyPnLPct <= -dailyLossLimit

var float peakEquity = strategy.initial_capital

if strategy.equity > peakEquity

peakEquity := strategy.equity

currentDrawdown = (peakEquity - strategy.equity) / peakEquity * 100

isDefenseMode = currentDrawdown >= totalDrawdownLimit

// ==================== 持仓状态管理 ====================

var float entryPrice = na

var float currentStopLoss = na

var float riskUnit = na

var int profitStage = 0

var float maxR = 0.0

bool hasPosition = strategy.position_size != 0

bool isLong = strategy.position_size > 0

bool isShort = strategy.position_size < 0

// ==================== 开仓逻辑 ====================

canOpenLong = bullEntrySignal and not hasPosition and not isDailyCircuitBreaker and not isNoTradeZone and not isDefenseMode

canOpenShort = bearEntrySignal and not hasPosition and not isDailyCircuitBreaker and not isNoTradeZone and not isDefenseMode

if canOpenLong and finalContractSize > 0

leverageText = effectiveLeverage > 1.0 ? " [杠杆:" + str.tostring(effectiveLeverage, "#.#") + "x]" : ""

strategy.entry("Long", strategy.long, qty=finalContractSize,

comment="激进多单 $" + str.tostring(actualRiskAmount, "#") + leverageText)

entryPrice := close

currentStopLoss := close - stopDistance

riskUnit := stopDistance

profitStage := 0

maxR := 0.0

if canOpenShort and finalContractSize > 0

leverageText = effectiveLeverage > 1.0 ? " [杠杆:" + str.tostring(effectiveLeverage, "#.#") + "x]" : ""

strategy.entry("Short", strategy.short, qty=finalContractSize,

comment="激进空单 $" + str.tostring(actualRiskAmount, "#") + leverageText)

entryPrice := close

currentStopLoss := close + stopDistance

riskUnit := stopDistance

profitStage := 0

maxR := 0.0

// ==================== 激进分级止盈逻辑 ====================

currentR = 0.0

if isLong and not na(entryPrice)

currentR := (close - entryPrice) / riskUnit

maxR := math.max(maxR, currentR)

// 阶段1:延迟保本(1.2R)- 你的配置

if currentR >= breakEvenR and profitStage < 1

currentStopLoss := math.max(currentStopLoss, entryPrice)

profitStage := 1

// 阶段2:延迟锁利(3R锁1R)- 你的配置

if currentR >= lockSmallR and profitStage < 2

currentStopLoss := math.max(currentStopLoss, entryPrice + lockSmallLevel * riskUnit)

profitStage := 2

// 阶段3:大利润锁定(6R锁3R)- 你的配置

if currentR >= lockBigR and profitStage < 3

currentStopLoss := math.max(currentStopLoss, entryPrice + lockBigLevel * riskUnit)

profitStage := 3

// 利润回撤熔断(4R后回撤2R就平仓)

if useGivebackKill and maxR >= givebackStartR and (maxR - currentR) >= maxGivebackR

strategy.close("Long", comment="回撤熔断 峰值:" + str.tostring(maxR, "#.#") + "R")

entryPrice := na

profitStage := 0

maxR := 0.0

// 实时止损检查

else if close <= currentStopLoss

strategy.close("Long", comment="止损 R:" + str.tostring(currentR, "#.#"))

entryPrice := na

profitStage := 0

maxR := 0.0

// 趋势终结强平

else if dailyClose < dailyEma50

strategy.close("Long", comment="趋势终结 R:" + str.tostring(currentR, "#.#"))

entryPrice := na

profitStage := 0

maxR := 0.0

if isShort and not na(entryPrice)

currentR := (entryPrice - close) / riskUnit

maxR := math.max(maxR, currentR)

if currentR >= breakEvenR and profitStage < 1

currentStopLoss := math.min(currentStopLoss, entryPrice)

profitStage := 1

if currentR >= lockSmallR and profitStage < 2

currentStopLoss := math.min(currentStopLoss, entryPrice - lockSmallLevel * riskUnit)

profitStage := 2

if currentR >= lockBigR and profitStage < 3

currentStopLoss := math.min(currentStopLoss, entryPrice - lockBigLevel * riskUnit)

profitStage := 3

if useGivebackKill and maxR >= givebackStartR and (maxR - currentR) >= maxGivebackR

strategy.close("Short", comment="回撤熔断 峰值:" + str.tostring(maxR, "#.#") + "R")

entryPrice := na

profitStage := 0

maxR := 0.0

else if close >= currentStopLoss

strategy.close("Short", comment="止损 R:" + str.tostring(currentR, "#.#"))

entryPrice := na

profitStage := 0

maxR := 0.0

else if dailyClose > dailyEma50

strategy.close("Short", comment="趋势终结 R:" + str.tostring(currentR, "#.#"))

entryPrice := na

profitStage := 0

maxR := 0.0

// ==================== 图表显示 ====================

plot(dailyEma50, "日线EMA50", color=color.orange, linewidth=2)

plot(h4Ema20, "4H EMA20", color=color.blue, linewidth=1)

upperBand = h4Ema20 + pullbackAtrMult * h4Atr

lowerBand = h4Ema20 - pullbackAtrMult * h4Atr

plot(upperBand, "回调上轨", color=color.new(color.gray, 70))

plot(lowerBand, "回调下轨", color=color.new(color.gray, 70))

plot(hasPosition ? currentStopLoss : na, "动态止损", color=color.red, style=plot.style_linebr, linewidth=2)

plot(hasPosition ? entryPrice : na, "入场价", color=color.white, style=plot.style_linebr, linewidth=1)

// 背景色:杠杆模式用深绿,普通牛市浅绿,熊市红色

bgColor = useLeverage ? color.new(color.green, 80) :

isBullishEnv ? color.new(color.green, 95) :

isBearishEnv ? color.new(color.red, 95) :

color.new(color.gray, 97)

bgcolor(bgColor)

plotshape(canOpenLong, "做多", shape.triangleup, location.belowbar, color.lime, size=size.small)

plotshape(canOpenShort, "做空", shape.triangledown, location.abovebar, color.red, size=size.small)

// 杠杆启用标记

plotshape(useLeverage and not hasPosition, "杠杆模式", shape.diamond, location.top, color.yellow, size=size.tiny)

// ==================== 激进版Dashboard ====================

var table dashboard = table.new(position.top_right, 2, 12, bgcolor=color.new(color.black, 85), border_width=1)

if barstate.islast

// 标题

table.cell(dashboard, 0, 0, "激进复利版 v3.0", text_color=color.white, text_size=size.normal, bgcolor=color.new(color.red, 50))

table.cell(dashboard, 1, 0, "高风险高回报", text_color=color.yellow, text_size=size.normal, bgcolor=color.new(color.red, 50))

// 账户状态

table.cell(dashboard, 0, 1, "当前权益", text_color=color.white, text_size=size.small)

equityColor = strategy.equity > strategy.initial_capital ? color.lime : color.red

table.cell(dashboard, 1, 1, "$" + str.tostring(strategy.equity, "#,###"), text_color=equityColor, text_size=size.small)

// 累计盈利

table.cell(dashboard, 0, 2, "累计盈利", text_color=color.white, text_size=size.small)

profitColor = cumulativeProfitPct > 0 ? color.lime : color.red

table.cell(dashboard, 1, 2, str.tostring(cumulativeProfitPct, "#.#") + "%", text_color=profitColor, text_size=size.small)

// 杠杆状态

table.cell(dashboard, 0, 3, "当前杠杆", text_color=color.white, text_size=size.small)

leverageColor = effectiveLeverage > 1.0 ? color.yellow : color.gray

leverageStatus = effectiveLeverage > 1.0 ? str.tostring(effectiveLeverage, "#.#") + "x 🚀" : "1.0x"

table.cell(dashboard, 1, 3, leverageStatus, text_color=leverageColor, text_size=size.small)

// 基础风险(3%)

table.cell(dashboard, 0, 4, "基础风险", text_color=color.white, text_size=size.small)

table.cell(dashboard, 1, 4, "$" + str.tostring(baseRiskAmount, "#") + " (3%)", text_color=color.aqua, text_size=size.small)

// 实际风险(含杠杆)

table.cell(dashboard, 0, 5, "实际风险", text_color=color.white, text_size=size.small)

actualRiskColor = actualRiskAmount > baseRiskAmount ? color.orange : color.lime

table.cell(dashboard, 1, 5, "$" + str.tostring(actualRiskAmount, "#"), text_color=actualRiskColor, text_size=size.small)

// 趋势状态

trendText = isBullishEnv ? "多头 ▲" : isBearishEnv ? "空头 ▼" : "震荡 ■"

trendColor = isBullishEnv ? color.lime : isBearishEnv ? color.red : color.gray

table.cell(dashboard, 0, 6, "趋势", text_color=color.white, text_size=size.small)

table.cell(dashboard, 1, 6, trendText, text_color=trendColor, text_size=size.small)

// 回调状态

pullbackText = isBullPullback ? "回调区 ✓" : isBearPullback ? "反弹区 ✓" : "等待..."

table.cell(dashboard, 0, 7, "回调", text_color=color.white, text_size=size.small)

table.cell(dashboard, 1, 7, pullbackText, text_color=(isBullPullback or isBearPullback) ? color.yellow : color.gray, text_size=size.small)

// 持仓状态

posText = isLong ? "持多 ●" : isShort ? "持空 ●" : "空仓 ○"

posColor = isLong ? color.lime : isShort ? color.red : color.gray

table.cell(dashboard, 0, 8, "持仓", text_color=color.white, text_size=size.small)

table.cell(dashboard, 1, 8, posText, text_color=posColor, text_size=size.small)

// 当前R倍数

table.cell(dashboard, 0, 9, "当前R", text_color=color.white, text_size=size.small)

rColor = currentR > 0 ? color.lime : currentR < 0 ? color.red : color.gray

table.cell(dashboard, 1, 9, str.tostring(currentR, "#.##") + "R", text_color=rColor, text_size=size.small)

// 历史最高R

table.cell(dashboard, 0, 10, "峰值R", text_color=color.white, text_size=size.small)

table.cell(dashboard, 1, 10, str.tostring(maxR, "#.##") + "R", text_color=color.lime, text_size=size.small)

// 止盈阶段

stageText = profitStage == 0 ? "初始" : profitStage == 1 ? "已保本" : profitStage == 2 ? "锁小利" : "锁大利"

table.cell(dashboard, 0, 11, "阶段", text_color=color.white, text_size=size.small)

table.cell(dashboard, 1, 11, stageText, text_color=color.yellow, text_size=size.small)

trader-c@TradercBTC

无编程背景,手搓AI量化交易策略。(前提:我手动交易能稳定盈利) 这是我前几天一直调试的整体回测结果,很明显的是在 $xrp ,黄金上效果不好。 另外从曲线看22年到25基本不赚钱。 我去问AI,让AI给我看。(在下文) 看完之后我认为这个对我来说暂时够用,我打算直接扔给OKX去跑策略,然后再改正。 其次AI建议我搞一个震荡策略,但是震荡策略我认为网格是最牛逼的(另外哪有上下60%震荡的,AI懂个🥚) 我打算整一套高买低卖的这种中期波段,或者说流动性收割(均值回归?无所谓了),专门应对21年之后的行情。 所以这周干两件事: 1.扔给OKX跑这个趋势策略。Pine Script逻辑转换成Python代码,扔到币安。 2.搞一套21之后的这种均值回归的策略。 理论上把这些细节单独开发出来,AI可以识别且自主决策,使用哪一套策略从而实现80%的自主交易。 另外最大单笔开仓名义金额在3w💲,理论上3000💲十倍就可以跑,我设置的最大亏3500,因此合理来说保证金在1w就能run。(举例子) (有问题评论区问,代码我两个月内如果测试盈利,我就直接公开,业内管这叫啥?开源?) (其实考虑的很多,成本啊之类的,但是先说这么多,搞得东西太多了不知道说啥,慢慢发吧) 以下是AI评价👇: 本质:只干两件事 顺着大趋势,在回调的时候埋伏进去,吃那一大段。 所以: 有明显方向、能走大波段的币(ETH、BTC、SOL) → 很强 长期横盘、假突破一堆的标的(XRP、黄金) → 天然吃亏 我这套系统是「专门打趋势波段」的, 对象是 BTC / ETH / SOL 这种“大起大落”的币, 像 XRP、黄金这种天天阴间横盘的,本来就不是我的猎场。 2. 为啥 XRP、黄金这么拉胯? XRP: 长期就是:偶尔暴冲一下 → 又回去横 真正给你吃到的趋势很少 大部分时间都在区间里「上下一点点晃你止损」 → 这种“回调狙击 + 动量过滤”的逻辑,在 XRP 上就是被当韭菜晃。 黄金: 波动小 + 走得慢,适合传统机构那种长线、宏观交易 参数是按「加密币那种大起大落」调出来的 → 放到黄金上就是:要么信号很少 要么一进场就被正常波动扫止损 再加上动不动就被宏观数据、央行讲话反杀 → 回测长期看下来,亏是很正常的。 这套系统就是「加密趋势专用」, XRP / 黄金不适合,表现差反而证明它没有乱来。 3. 22–25 年为啥曲线变平? 核心:不是策略坏了,而是市场给你的“好球”变少了。 可以这样理解: 17–21:典型「狂牛 + 深熊」循环大涨大跌 → 你的趋势系统机会超级多 一波牛市能连吃很多 5R、8R、10R 的大单 22–25:整体是「阴跌 + 大震荡 + 假突破」真正干净的大趋势很少 你的「动量 + EMA50 过滤」一开,多数时间压根不开枪 偶尔有一波上涨,也是:拉一点 → 横很久 → 慢慢磨下来 你的分级止盈能锁一点,但很难再出现那种「一骑绝尘」的大波段 所以你看到: 曲线不再像 17–21 年那样狂飙 但也没有大幅回撤,而是「横着 + 轻微上下」→ 这其实说明:在不适合的行情里,你的系统选择「少出手」而不是「乱亏钱」——这是优点。 22–25 年这三年,本来就是「烂行情为主,趋势行情减少」的阶段, 系统在这段时间更多是保护本金 + 小打小闹, 真正的大爆发还得等下一轮像 17–21 那样的周期。

中文