Tweet fixado

📊 Late May 2026 Portfolio Update

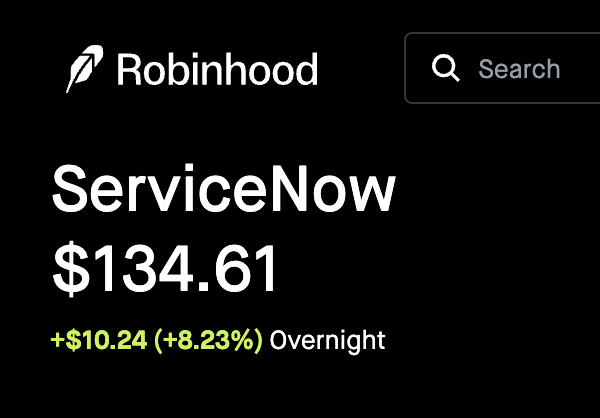

$AMD still anchors the portfolio at 51% of my individual holdings ! Added aggressively $NOW on weakness and now my second biggest position.

Full breakdown (Verified by Blossom):

• $AMD: 51% – Inference King. Unrealized gains sitting at +304%. Long-term this is a multi-trillion dollar company in the making

• $NOW: 14.5% – Massive 6-figure position. Took full advantage of the discounts/pullbacks in the last month; aggressively added on weakness. Anything below $110 is still a straight-up bargain. AI Control Tower for Enterprise; structural long-term winner.

• $JD: 10% – Global expansion/logistics powerhouse and China recovery play. Long-term conviction fully intact.

• $OSCR: 7.4% – Unbelievable moat in health insurance + AI. High-conviction long-term disruptor.

• $AMZN: 6% – Very long-term compounder. Keep adding on every dip.

• $ELF: 5% – Slowly building the position. Fundamentals, growth, and valuation still look like an absolute steal — anything below $100 is a massive bargain 💎

• $HIMS: 4.3% – Peptides anyone? 👀 Long-term personalized health leader.

• $ACHR: 1.5% – Speculative eVTOL play with enormous long-term upside optionality.

Long-term growth mode activated 💪

English