Raj A

1.2K posts

Raj A

@RealYuvaraj

Learn, adapt, apply, discuss, debate, explore, cherish - ramble, offer opinion when not solicited

Entrou em Aralık 2020

2.2K Seguindo459 Seguidores

Guys, I became a father yesterday.

The birth was not what we hoped for as my wife lost a lot of blood and went through emergency cesarean section.

She stayed very composed while she laid our future in the hand of science and doctors we never met. Apparently, a mother knows what she has to do.

My wife and son are in great condition now.

Incredible grateful for all the doctors and nurses who helped during surgery.

English

@jbelizaireCEO John are you guys using autonomous energy nodes to manage renewable power source? This seems to be an emerging trend with DOE supporting development of this technology. Do you have a partner?

English

😍

McNallie Money@McnallieM

✅ Big move: @SolunaHoldings recently acquired the 150MW Briscoe Wind Farm in West Texas for $53M — powering data centres directly from owned renewable generation. ✅Why it matters: The old model of leasing energy via power purchase agreements may be losing ground. Soluna is embedding generation into its data centre stack for tighter control over supply. 🔋 ✅The numbers: The wind farm is projected to generate $20M–$24.4M in annual revenue in year one — with upside tied to Texas electricity prices. 📈 ✅The vision: @jbelizaireCEO says it best: "Energy sovereignty is the key durable moat in the AI infrastructure race." As AI demand surges, owning your power isn't optional — it's strategic. 🌬️🏗️ $SLNH up today over 18%!!! 🔥🔥🔥

ART

Bitcoin miners to HPC/AI - my ramblings

1. $CLSK - steady accumulation in progress; are they close to announcing a deal

2. $RIOT - this could be the dark horse; the facility, energy management asset, $AMD pilot, $BTC holding and recent volumes look promising

3. $MARA - if they shake up the management including the board; this stock will rerate

4. $IREN - execution maybe their strength

5. $DGXX - would be a great acquisition for $IREN to add to their portfolio in uncovered geographies and power gen assets and modular concepts

6. $DMGGF - $IREN or $HIVE should acquire them

7. $HIVE - could be a differentiated play not getting publicity because of Canada focus

8. $CIFR - steady

9. $KEEL - blue state regulatory hurdle, but does have $VRT partnership for Rubin deployment (18MW)

10. $WULF - lots of strengths; approvals could trigger price

11. $APLD - do not know enough here

12. $BTBT - retrofit and speed promising but not clear how they will acquire long lead time items when they purchase new sites after North Caroline

English

Unfortunately, on my birthday (4/9), I was in a severe accident and fractured my pelvis in 6 places, which led to a 9 hour surgery. The last few days since have been completely unhinged. I’m recovering now and taking it day by day, and it definitely puts everything into perspective fast. Grateful to be here. 🌹

English

Primary sites in Blue states where permitting poses challenges. Supply chain disruptions and execution could push back revenue into 2028; they already announced delay from H1 to H2 2027. Permitting and supply chain risks a major concern although they have good partnerships established the delays will what will hurt them.

English

$KEEL One company has an awesome CEO who knows how to execute and run a business the other has Ben Gagnon with little to no experience as a CEO. $KEEL Could have been well on there way to matching WULF unfortunately they just can't seem to execute. Lots of yapping but ZERO contracts and nothing accomplished in 2026 as of yet. Hopefully things change later this year only time will tell.

Also half the data centers are being canceled and Maine just paused all data centers until 2027. Supply and demand here folks looks really nice for Keel. Hopefully by Q1 earnings next month we will get more good news on permits. Even though Keel is a little behind its peers, it looks like it will pay off with better deals. Just need to get the sites approved and this is a brand new stock.Tick tock...

Like if you STILL believe $KEEL.

Don’t just watch from the sidelines. Hit follow and let’s stack together.I'll always keep the $KEEL channel up to date.

English

@ShabtaiYossi Need a contract and volume purchase...teasers followed by a raise...this pattern has to stop....

English

$SIDU & $MTEK

If one is running… why is the other still standing still?

When $SIDU is moving forward in the space market with its LizzieSat constellation —

how is it possible that $MTEK is still priced as if it’s not even part of the story?

Let’s talk facts.

🚀 This isn’t theory — this is real space integration

In January 2026, $MTEK completed a technology integration inside LizzieSat-4.

Not a paper concept.

Not a presentation.

👉 A real system inside an operational satellite.

🧠 What does $MTEK actually bring to the table?

Not “cameras” — but the brain.

Real-time video processing (EO/IR)

AI-based object detection

Smart data compression

Built for extreme environments (including space)

👉 Meaning:

The satellite doesn’t just capture data — it understands it.

📡 Why does this matter?

In the NewSpace era, data is king —

but the ability to process it onboard (Edge AI) is the real advantage.

Less reliance on bandwidth

Faster decision-making

Higher-quality actionable data

And that’s exactly what $MTEK delivers.

🤝 So what’s the relationship here?

Yes — $SIDU is the customer.

But it goes deeper:

👉 $MTEK is the AI layer inside the satellite

👉 $SIDU is building the platform

This isn’t just a supplier relationship.

This is a strategic value-driving partnership.

📈 What does this mean for investors?

$SIDU:

Building a constellation

Gaining traction

Capturing attention

$MTEK:

Already inside

Already integrated

Already proving capability

So the real question becomes:

👉 If $SIDU is running…

👉 and $MTEK’s technology is inside its satellites…

Why is $MTEK still priced like it’s standing still?

🔥 And this is just the beginning

As LizzieSat expands:

More satellites = more systems

More systems = more potential revenue

More missions = stronger proof of capability

That’s how companies transition from

“small cap”

to

“real growth story”.

🧩 Bottom line

$MTEK is no longer just a defense company.

It is:

Defense ✔️

Drones ✔️

Armored vehicles ✔️

And now… Space ✔️

And the market?

Still hasn’t connected the dots.

If there’s one question investors should be asking right now, it’s not:

“Does it work?”

It’s:

👉 How long until the market realizes that it already does.

English

Well o one thing I liked was how they talked about all the connectors they have with thousands of vendors to promote simplified expensing and how that is valuable and how that differentiates them from AGI that’s a plus. The main play here is the theses that it is significantly under valued here is putting his money to increase ownership and maybe take it private or sell. Could Navan be interested ?

English

$EXFY

March 3 and March 11, Steve McLaughlin bought roughly 2.26 million shares on the open market at an average price of around $0.94, spending over $2.1 million of his own money.

This isn't just any insider buying the dip. This changes the entire risk profile of the trade. Here is why your instinct that EXFY is a bargain is completely validated, and how it changes my recommendation on your MRAM rotation.

1. The "Steve McLaughlin" Factor

Steve McLaughlin is not just a random board member or passive investor; he is the Founder and CEO of FT Partners—arguably the single most powerful and connected boutique investment bank in the entire global FinTech space.

He facilitates the biggest mergers, acquisitions, and take-privates in financial technology.

• The Signal: When the premier FinTech M&A banker in the world steps into the open market and buys 2.26 million shares of a beaten-down expense management software company (bringing his total ownership to over 12 million shares, or ~12.5% of the company), it screams one thing: M&A or Take-Private Potential. * The Valuation Floor: McLaughlin clearly sees what you see. Expensify is currently trading at less than 1x Enterprise Value to Free Cash Flow (EV/FCF). For a SaaS company generating over $140M in revenue, that is an absolute fire-sale valuation. He knows the underlying asset is worth vastly more to a private equity firm or a larger competitor than its current $75M public market cap implies.

English

@value_invest01 Execution risk, delays due to long lead time items, and push out of revenue to second half of 2027 should be concerns but all that could change if they announce a deal and the stock will re-rate as co-location should bring money up front ; 2X in price a reality until they execute

English

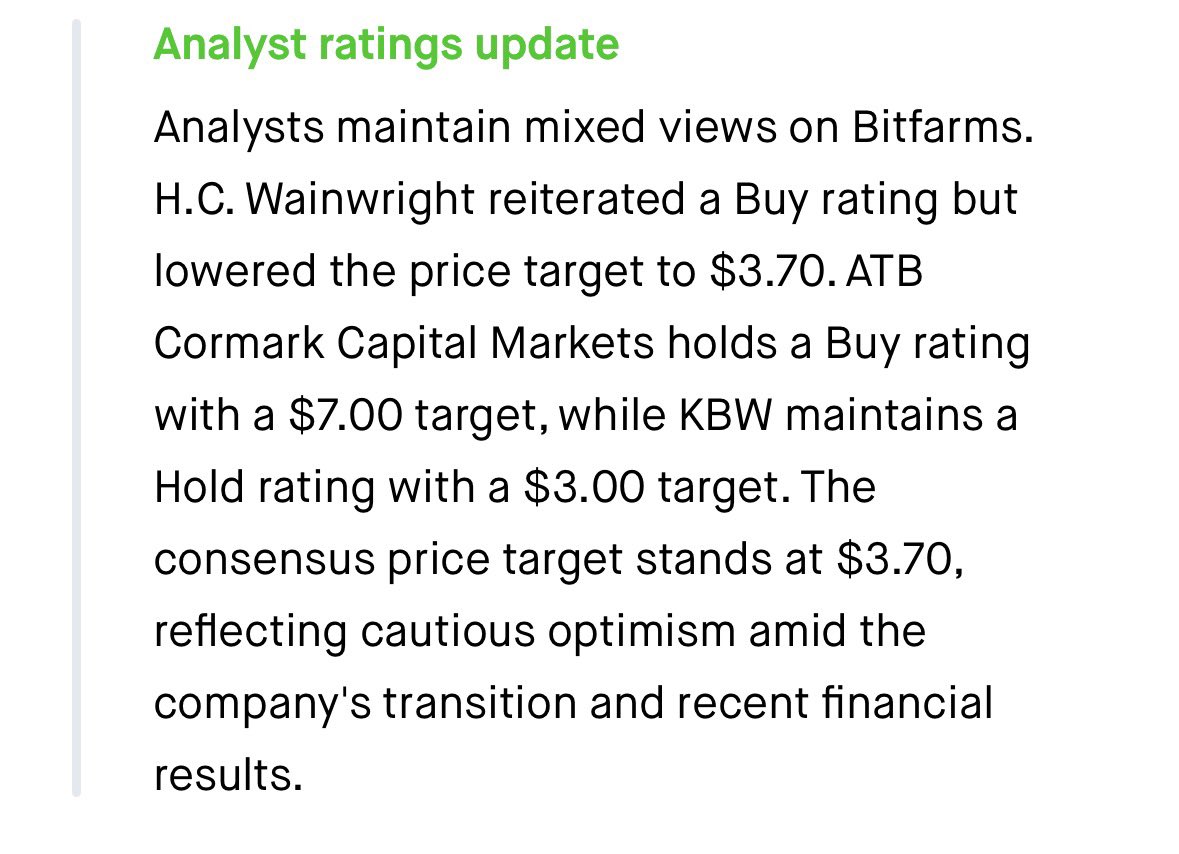

🚨 🚨 $BITF analyst updates are mixed, which pretty much matches where the story is right now.

• H.C. Wainwright: Buy, PT lowered to $3.70

• Cormark: Buy, $7.00 target

• KBW: Hold, $3.00 target

Consensus sits around $3.70.

That spread tells you everything:

There’s upside if the pivot works,

But conviction isn’t fully there yet.

The transition to HPC / AI is what analysts are betting on.

Until there’s clearer execution (tenants, deals, timelines), expectations stay cautious.

English

Here is my Fintech list. If you are interested in Fintech and would like to participate, just post here and I will add you.

x.com/i/lists/203900…

English

@Billerrr1 Along with a $3M raise… every news item followed with a raise… not a fan of management at all… teasers with no real POs

English

$MTEK

Maris-Tech Expands into the Ukrainian Drone Video Payload Market

Bull Case:

+ Direct expansion into the highly demanding and active Ukrainian drone video payload market, suggesting high demand for their "AI-powered edge video solutions."

+ Leverages "AI-powered edge computing technology" and "real-time video processing and AI at the edge," aligning with strong market hype in the AI/tech sector.

+ Official press release via GLOBE NEWSWIRE, released pre-market, indicating credibility and potential for significant intraday price action.

Bear Case:

− The announcement mentions an "initial transaction," implying the immediate scale of revenue might be small, and not a large, guaranteed contract.

− Transactions are conducted through a "third-party Israeli company," which adds a layer of indirectness to sales and could imply less control over direct market penetration.

This news is a significant bullish catalyst for MTEK, strongly aligning a penny stock with critical defense technology and the red-hot AI sector. The pre-market release via a reputable newswire suggests strong intraday momentum potential as active day traders are likely to bid up the stock based on this positive development and sector relevance. While the initial revenue scale is unclear, the strategic market entry into a high-demand environment presents a compelling short-term trading opportunity.

#pennystocks #daytrading

Not financial advice. DYOR.

English

Have you assessed this risk below-

The 2021 Peak: During the zero-interest-rate tech boom of 2021, Ethos raised a massive Series D from heavyweights like SoftBank, Sequoia, and Accel at a staggering $2.7 billion private valuation.

• The 2026 IPO (January 29, 2026): When Ethos finally went public earlier this year, the market forced them to take a massive "haircut." They priced their IPO at $19.00 a share, giving the company a fully diluted market cap of roughly $1.3 billion—less than half of what it was worth in the private markets three years prior.

July IPO unlock concern:

Ethos only offered about 10.5 million shares to the public during the IPO. Meanwhile, entities like Sequoia and Accel hold nearly 20 million shares combined. Because these venture funds have been trapped in this investment since 2019/2021, there is a very high probability they will use the July unlock as a liquidity exit. When tens of millions of shares suddenly flood a market that only has a ~10 million share float, the downward pressure on the stock can be violent.

English

My $LIFE Notebooklm Framework:

Based on the provided sources and the Fintech Framework, here is the fundamental score analysis for Ethos Technologies Inc. ("Ethos").

I. Fundamental Score: 10 / 10

Ethos receives a perfect fundamental score, placing it in the "Category-defining, elite, investable" bracket (8–10 points).

1. Revenue Growth (2 / 2 points)

Analysis: Ethos reported revenue of $388 million for the year ended December 31, 2025, a 52% increase over the $255 million reported in 2024. This significantly exceeds the framework's >25% threshold for 2 points.

Quarterly Performance: Q4 2025 revenue grew 65% YoY.

2. 3–5 Year CAGR (2 / 2 points)

Analysis: The company has demonstrated a consistent long-term compounding engine. Its three longest-tenured carriers grew annual premiums at a 64% CAGR from 2021 to 2024. Total revenue grew at a 60% rate from 2023 to 2024.

Future Outlook: 2026 guidance projects total revenue of $510M–$514M, a 32% YoY growth at the midpoint, maintaining the >25% trajectory.

3. Profitability (2 / 2 points)

Analysis: Ethos is already profitable with expanding margins. It achieved GAAP profitability in 2023.

Earnings Quality: For 2025, the company reported a net income of $71.2 million (18% margin) and an Adjusted EBITDA of $89.0 million (23% margin).

Gross Margin: The company maintains elite unit economics with a 98% gross profit margin in 2025.

4. Competitive Advantage / Moat (1 / 1 point)

Analysis: Ethos possesses a strong data moat and network effects. Its proprietary underwriting engine ingests 250,000 data points per application, allowing 95% of applicants to receive instant decisions.

Ecosystem Lock-in: The three-sided platform creates a flywheel where more consumers attract more carriers, providing agents with more products to sell, which in turn attracts more agents and scales fixed costs.

5. TAM (1 / 1 point)

Analysis: The realistic economic TAM is far greater than $1 billion. Existing products (Term, Whole, and IUL) represent an aggregate of $12.6 billion of annual new policy premiums.

Expansion Potential: Expanding into products like Variable Universal Life and Annuities could grow the market opportunity to over $140 billion in new premiums annually.

6. Management (2 / 2 points)

Analysis: The co-founders (Peter Colis and Lingke Wang) have a proven track record, having scaled the platform from one product in 2019 to ten by late 2025 and achieving over 500,000 policy activations.

Execution: They have successfully transitioned the company to GAAP profitability while maintaining high double-digit growth.

Note: While management identified a material weakness in internal controls related to complex transactions (sale of commissions), they have implemented remediation measures and concluded that disclosure controls were effective at the reasonable assurance level by year-end 2025.

II. Contextual Landscape Analysis

Category Position: Challenger/Leader in the digital-first life insurance space.

Moat Type: Data advantage and network effects.

Threats: Incumbent carriers (many 100+ years old) with large capital but legacy technology.

Market Structure: Highly fragmented, providing a massive runway for a tech-enabled consolidator.

III. Preliminary Red Flag Assessment

Concentration Risk: Revenue is highly concentrated, with the top three carrier relationships accounting for 88% of total revenue in 2025 (down from 98% in 2024).

Dual-Class Structure: Holders of Class B stock (founders and VCs) hold 95.5% of the voting power, limiting the influence of public Class A stockholders.

Fundamental Score Interpretation: With a score of 10/10, Ethos is considered "Category-defining and elite." Based on the reference stock price of $10, which is significantly below the $19.00 IPO price, the company would likely screen very highly on the framework's Value Score as well (to be calculated separately), potentially making it a "priority buy" on a two-axis framework.

English

The FDA's Allegations

The FDA's Office of Prescription Drug Promotion flagged a recent TV advertisement and a podcast (titled "Is the FDA BLOCKING Life Saving Cancer Treatments?") featuring Executive Chairman Dr. Patrick Soon-Shiong and CEO Richard Adcock.

The agency stated these materials were "false or misleading" because they vastly overstated Anktiva's approved capabilities. Specifically, the FDA called out claims that Anktiva:

• Could "treat all cancers" or act as a broad "cancer vaccine."

• Could prevent cancer in individuals exposed to radiation.

• Could function as a standalone, single-injection treatment.

Currently, Anktiva is only approved for a very specific, narrow indication: treating BCG-unresponsive non-muscle invasive bladder cancer (NMIBC) in combination with BCG therapy.

The Regulatory Threat

The FDA has given ImmunityBio 15 working days to respond in writing, pull the non-compliant marketing, and issue corrective messaging to the audiences who saw the ads. If they fail to comply, the FDA threatened formal legal enforcement. Compounding the issue, the FDA noted this is essentially ImmunityBio's third strike regarding promotional compliance, following earlier untitled letters sent to its subsidiary in September 2025 and January 2026.

English

$IBRX the FDA letter is a hard read, and honestly it feels like a lot of us may have been misled, me included.

A lot of claims were repeated with confidence, but now the FDA is laying out specific examples saying the company overstated or misrepresented parts of the science. That deserves real attention, not blind deflection.

Wanting a breakthrough in cancer treatment is understandable. That hope pulls people in. It pulled me in too.

But this is the point where emotion has to step aside and the actual statements from the FDA need to be examined one by one.

Anecdotes are not evidence.

Belief is not evidence.

And hope is not evidence.

If the FDA is right, then this was not just overpromotion.

It means people were sold something bigger than what the science actually showed.

I hate cancer.

That is exactly why the truth matters so much.

English

@BullishNSassy I guess you have not seen the recent CEO interview. It was as transparent as it gets. @FrankCurzio did one last week.

English

$DGXX

DGXX dropping earnings soon and I gotta say… the lack of earnings calls is starting to stand out.

Not even trying to nitpick, but this is pretty basic stuff for public companies. Numbers + live Q&A = accountability.

You want institutional money? You’ve gotta play the institutional game.

Love the AI pivot, love the direction… but transparency needs to level up with the narrative.

Hard to take the next step without it.

How does everyone else feel about this or is it just me?

English

Energous has achieved AWS Independent Software Vendor (ISV) Accelerate status, with its partner profile now officially listed on the AWS Partner Network website. This designation recognizes Energous as a validated AWS partner, reinforcing the enterprise credibility of its Ambient IoT and wireless power end-to-end solutions and deepening its go-to-market alignment with

AWS.

Made in the U.S.A.

– Effective March 2026, the Company expanded its production capacity, launching a new contract

manufacturer based in the United States. This strategic initiative ensures Energous is better positioned to fulfill orders for its wireless power network solutions as well as service customers requiring that products be designed and manufactured in the

United States.

Energous strengthened its intellectual property portfolio with 15 new patents granted in 2025, supporting the Company’s long- term technology leadership in wireless power networks.

“Our customers need more than 'connected' environments—they need dependable infrastructure,

" concluded Burak.

"Wireless power networks are to battery-free IoT what WiFi was to mobile devices: necessary infrastructure that makes the ecosystem actually work, which

we are demonstrating Energous can deliver.

”

English

After the end of the year through March 23, 2026, the Company raised net proceeds of approximately $31.9 million from additional sales under its ATM program. As of March 23, 2026, our cash and cash equivalents were approximately $39.4 million.

We intend to use our available cash to pursue strategic acquisitions and investments, to invest in research and product development, other strategic initiatives, fulfillment of customer demand, and for operational and general corporate purposes.

A multi-billion-dollar, U.S. based subsidiary of a British parent company selected Energous’ end-to-end Ambient IoT solution for a large-scale proof-of-concept deployment that will modernize its semi-perishable inventory tracking across its production and

distribution operations. Continuing its goal of optimizing its existing processes at a key facility and improving visibility, this customer chose Energous to enable real-time inventory tracking using wireless power networks, battery-free sensors, gateways,

and cloud analytics.

Energous is currently engaged in a large-scale proof-of-concept with a Fortune 10 subsidiary focused on retail sales of bulk items.

A primary use case for this deployment is cold chain compliance monitoring at dock doors, tracking pallet dwell time from point

of entry through storage in freezer and cooler areas.

English

Energous Corp

$WATT

During 2025, the Company demonstrated its continued focus on growth and fiscal discipline, reporting its fourth consecutive quarter of growth, with revenue of approximately $3.0 million for the three months ended December 31, 2025, representing a 139% increase from

$1.3 million of revenue reported for the three months ended September 30, 2025.

Improvement from the third quarter to the fourth quarter

of 2025 was also evidenced by a narrowing net loss to $1.3 million for the three months ended December 31, 2025, representing a 37% improvement from a net loss of $2.1 million for the third quarter of 2025.

"We believe we have reached an inflection point investors have been waiting for—commercial deployments at scale, driving our highest

recorded annual revenue to date. Our fourth consecutive quarter of revenue growth, combined with over 25,000 PowerBridge transmitters deployed with zero returns, and a Fortune 10 retailer’s planned expansion from 410 to 4,700 locations, demonstrates that wireless power

networks have moved from technology validation to production infrastructure,

" said Mallorie Burak, CEO and CFO of Energous

Corporation.

"The fundamentals are increasingly being proven; enterprises are choosing wireless power networks over ambient harvesting

because they need guaranteed coverage.

”

English