Tweet fixado

3 NSE picks for Feb-March 2026:

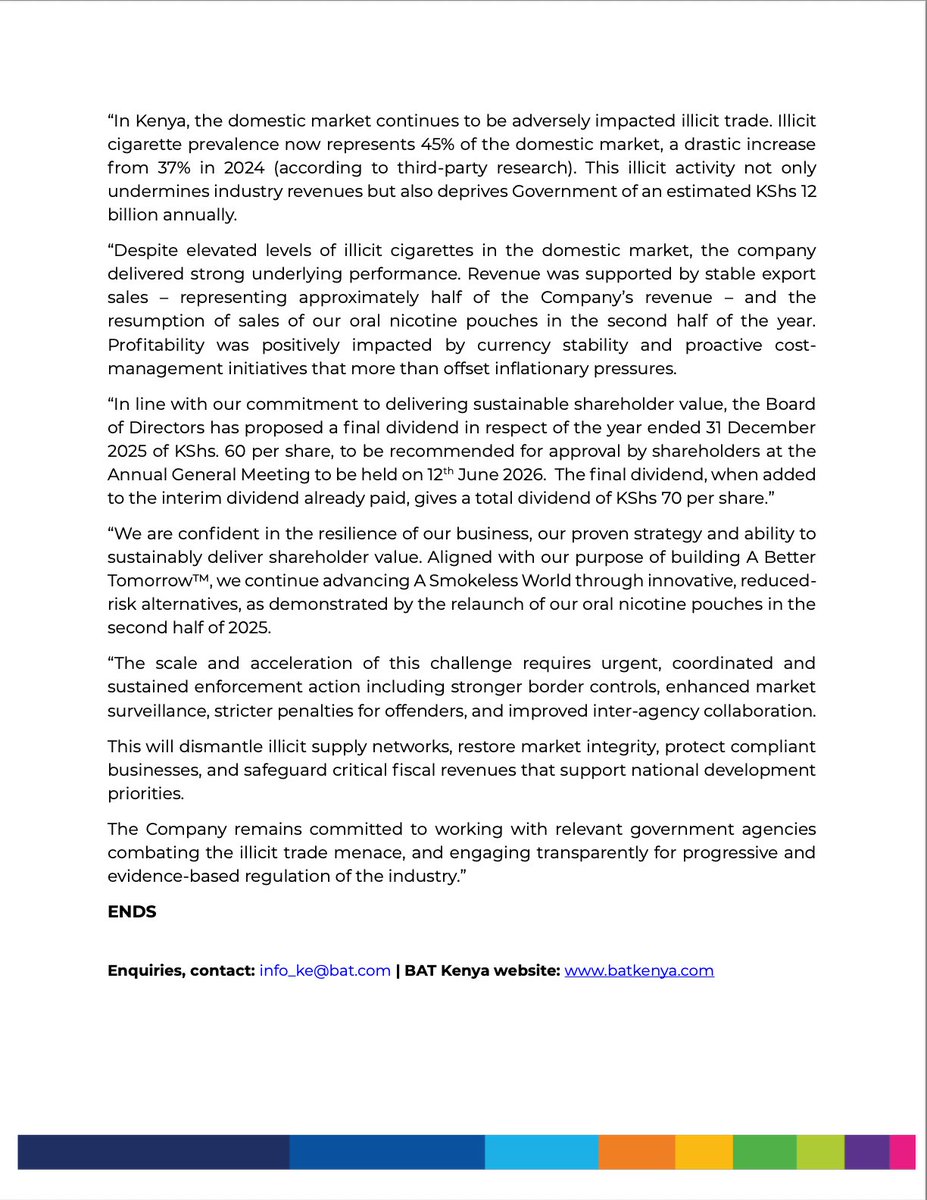

1. BAT - Likely final dividend Ksh 45-50 in a fortnight

2. NCBA - 9400 NCBA shares at ksh 105 + Final Dividends 2025 & H1 Interim 2026 dividends

3. KPLC - Undervalued especially when compared to KPC IPO

English