Almost Research

196 posts

Almost Research

@almost_research

Stock Market Commentary. Not Financial Advice.

Entrou em Ağustos 2021

495 Seguindo134 Seguidores

$DDOG platform tracks metrics like: CPU usage, memory, latency, request volume, error rates.

Given the current hardware shortages related to the above

Seems very key for keeping AI workloads efficient

Probably a big Q coming up this week, just as software is bouncing

English

@mathlonning Sadly, the numbers point to them losing market share.

English

$TMDX

Waleed says they’re maintaining and growing market share. That’s all I needed to hear.

English

@Andreaskjo @munster_gene 🎯

Amazon is effectively keeping that $30B spread inside the house. So freaking bullish.

English

@munster_gene You need to couple the report with the recent letter to shareholders as well as the recent Anthropic letter to shareholders. Basically Amazon could have made 50 billion this q if they had sold the chips Nvidia style. But they opt to rent for 20b instead. Also own 23% of Anthropic

English

$AMZN revenue up 15% in March vs. 12% in December.

AWS up 28% missed the whisper of 30%. Thats ok because the real number was likely much better. Have to wait for the call to hear more.

My take: Like Microsoft, Amazon needs to make a statement with investors that they have AI products consumers must have. It needs to be more than AWS growth to get the AMZN multiple to rerate.

English

@almost_research Thank you for correcting, never good to see work stolen. It’s a good analysis you did otherwise. Enjoyed it.

English

Thoughts on $TMDX

$TMDX has been a painful stock to hold since the war with Iran started. Flights were strong to start Q1 then slowed down a bit throughout the rest of the quarter, and we're seeing the same thing happen again in Q2. Earnings are next week, and today we saw a 2x to 3x spike in volume on a massive red candle. I see TMDX bulls on X writing off this price action as completely irrational. So let's unpack some facts that I believe to be driving it. I think it makes sense to break them down into two categories (1) Flight Tracking and (2) Oil Prices.

Flight Tracking:

First, some points to consider.

1. FY2026 revenue growth was set at 20-25% in the Q4 earnings report.

2. Flight tracking has historically been ~97% accurate in predicting revenue.

3. Q1 Flight Tracking Growth: 18.8% (2,535 vs. 2,133)

4. Q2 Flight Growth (Projected): 12.5% (2,708 vs. 2,408)

Q1 and Q2 mathematically cannot get them to their 20–25% full-year revenue guidance on their own.

However, recent OPTN data (see table below) is painting a different picture. Last year, DCDs made up 29% of all transplants. So far this year, they make up 38%. Overall YTD DCD growth is sitting at a massive 36%. That is a structural shift in how organs are procured in the US. TMDX’s OCS remains the gold standard for long distance DCD procurement. With national DCD heart transplants up 28% YoY, the TAM is aggressively expanding right into their strike zone. Even if NRP takes the short-distance routes, the sheer volume of national DCD expansion guarantees TMDX a massive revenue tailwind.

To recap:

- National DCD YTD growth is 36%,

- TMDX flights have historically been very accurate at predicting its revenue

- TMDX is guiding for 20-25% revenue growth

- Based on flight tracking alone annual growth looks to be 15.5%

It's pretty obvious what the elephant in the room is: if DCD YTD growth is 36% and TMDX flights are not enough to explain the growth nor meet it's annual guide - then where is the growth coming from?

I believe it's one of two things: Ground Transportation growing significantly this year or loss of market share.

The market seems to be casting votes for loss of market share, but TMDX bulls know that Waleed has been vocal about flight tracking not being a reliable way to predict it's revenue in the future and about ground transportation becoming a more meaningful part of it's overall missions.

Personally, I think it's more likely we see revenue "decouple" from being 97-98% correlated to flight tracking for this first time in this Q1 print and we hear Waleed confirm that ground transportation has increased meaningfully. The data supports this view.

Oil Prices:

TMDX has been trading like an inverse oil ETF since early March.

In Oppenheimer Healthcare conference last month, Waleed (TMDX CEO) dismissed the notion of fuel costs spikes having a meaningful adverse effect on the business and he confirmed that they utilize fuel surcharge pass-through mechanisms in addition to a rolling fuel hedge program. We've since seen numerous analysts confirm this to be true through channel checks. Interestingly, he did get a little defensive when questioned on the topic. This might be due to confidentiality agreements they have with hospitals.

This begs the question: why the F is TMDX trading like an inverse oil ETF if we know the business is insulated from oil shocks?

I have a theory: In the FY2025 10-K, management explicitly cites rising fuel costs as a material threat to gross margins and operating results. However, the filing completely omits any detailed language regarding the rolling fuel hedging program or the fuel surcharge pass-through mechanisms to transplant centers.

By failing to document these mitigants in their formal filings, TMDX mgmt have left the stock entirely exposed. Quantitative algos and automated trading systems parse the 10-K, classify TMDX as an unhedged aviation/logistics play, and aggressively sell the stock in close correlation with oil price spikes. Nobody invested in TMDX to hold an unhedged proxy on crude oil.

It looks like mgmt set it up so that the operational reality of the business is disconnected from their SEC filings with regards to oil and its hedging practices.

My hope for the Q1 report is we see (1) ground transportation meaningfully contribute to its topline (looks very promising) and (2) Waleed shutdown concerns about oil prices dragging down margins (close to guaranteed).

English

@POLR_Investing My mistake -- I didn't expect this post to get this much traction and grabbed the cropped screenshot from a discord. I just added the full image with your disclaimer and tagged you in the main thread. Great work pulling this data together.

English

@almost_research Cut off my copyright and an important disclaimer 😂

English

Adding the full uncropped table here with the proper copyright and disclaimer. Credit to @POLR_Investing for compiling this OPTN data. Excellent work putting these metrics together.

English

Worth noting Q2 2025 flights were meaningfully higher than Q4 2025 flights but Q4 2025 revenue was higher than Q2 2025 revenue. This shows that ground transportation is now gaining more traction.

English

@mathlonning Have your read their 10-K? The operational reality of the business is completely disconnected from their SEC filings.

English

As crude oil futures spiked, $TMDX dropped. Roughly the same percentage. Like clockwork.

Earnings may help mitigate this correlation as the company proves it is not affected by rising oil prices.

English

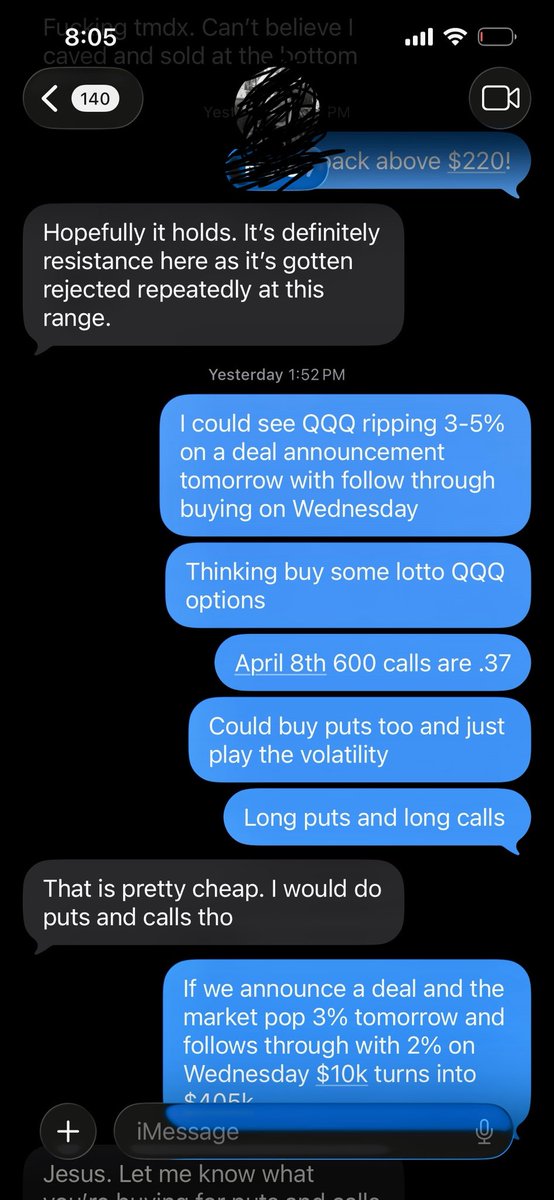

4/8 (today) $600 $QQQ calls is the most asymmetric bet I’ve seen in a long time. This text is from Monday. Anyone catch this?

English

Almost Research retweetou

NEW: In a letter to employees, United CEO Scott Kirby says the airline is prepping for oil to hit $175/barrel &

“doesn't get back down to $100/barrel until the end of 2027.”

United is shaving 3% of off-peak flights - “think redeyes, Tues/Wed/Sat flying” - this spring & summer.

English

I’ve been calling it insane too. But could the market be pricing in a dystopian outcome where AI does result in mass unemployment? The Fed would step in with QE, but it doesn’t work? Companies would use the cheap financing to spend more on compute instead of hiring more people? This would be the first time in history where QE doesn’t result in meaningful job hiring? If monetary policy can’t fix the labor market, fiscal policy has to step in and UBI makes the most sense. How much do you think that amount will be? $15k per year? Idk. In this hypothetical scenario, which companies benefit? Walmart seems to be a clear winner as people trade down and spend a disproportionate amount of their low income on low cost items at a Walmart or a dollar store. 🤷🏻♂️

English

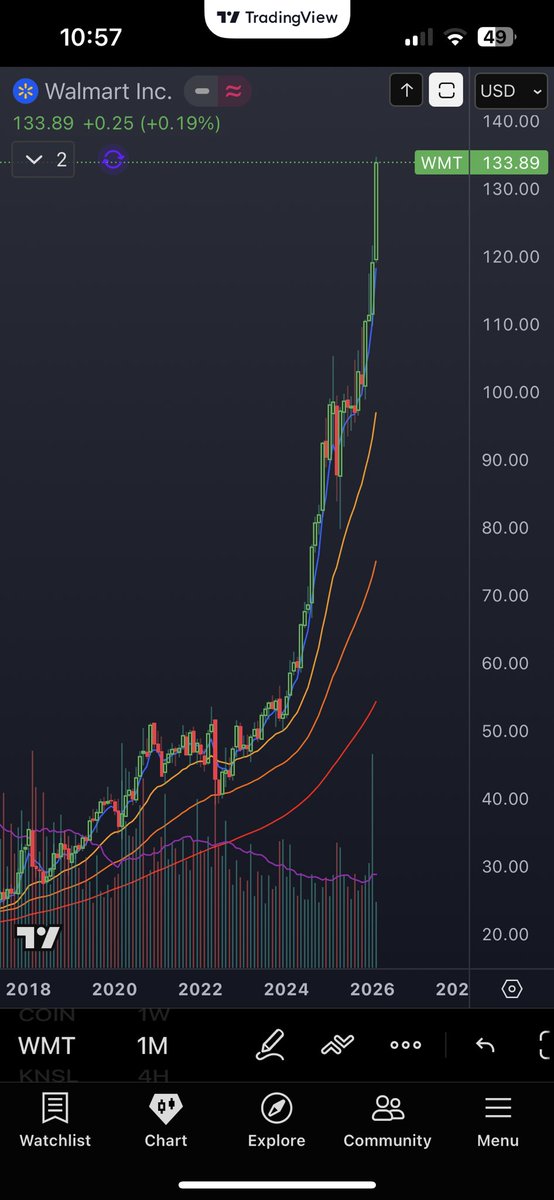

Can someone explain how $WMT can trade at 46x earnings while $AMZN is at 28x?

Retail? Amazon marketplace is growing faster than Walmart.

Ads? Amazon’s ad revenue is 10x that of Walmart.

Plus, Amazon has the dominant cloud business.

Make it make sense?

English

Commenting on the $HIMS x $NVO partnership news that came out late yesterday.

I think it makes complete sense and I can’t wait to see how Monday plays out!

My opinion is that HIMS is transitioning away from GLP1s and will go all in on other less competitive peptides that can be produced in their peptide facility now that those peptides are moving from category 2 to category 1. I think HIMS could be the leader in those peptides and they’re fine letting NVO focus on GLP1s and using sales on their platform as an additional revenue stream while they focus on the other peptidws that will presumably be in house and have higher margins.

If I were Andrew:

Partner with both NVO & LLY and sell their GLP1s and not even compete with either company in that realm. Continue selling hair loss, erectile dysfunction, testosterone, menopause, etc. and shift all focus to peptides coming off the category 2 list and become the leader in peptides. Allows HIMS to focus on a category they can win and also helps cross sell NVO & LLY customers other peptides making those customers super sticky the HIMS eco system.

bloomberg.com/news/articles/…

English

@Brian_Stoffel_ @AlejoBusMur91 Tmdx uses fuel surcharge thresholds in its customer contracts

English

@AlejoBusMur91 Don't disagree, but outside fuel costs, the underlying business isn't really affected by macro much, it more has to do with FDA approvals

English

Kind of hilarious how investors can't decide how they feel about $TMDX on a daily basis

English

@Apollo_21mil Same, impossible to say when but it’s safe to say a brutal correction on the name will take place at some point

English

@almost_research Definitely, I wonder when they get added to the list of “quality” companies that lose their premium multiple.

English