Tweet fixado

Tax Bro

3.6K posts

Tax Bro

@dee___why

🇳🇬 | Accounting | Tax | Compliance & Reporting | AAT, FMVA®, ACA, ACTi, CIMA Candidate

On a Mission Entrou em Aralık 2011

615 Seguindo1.4K Seguidores

Tax Bro retweetou

𝐌𝐚𝐲 𝐰𝐞 𝐚𝐥𝐰𝐚𝐲𝐬 𝐛𝐞 𝐰𝐨𝐫𝐭𝐡𝐲 𝐨𝐟 𝐭𝐡𝐞 𝐩𝐨𝐰𝐞𝐫 𝐰𝐞 𝐡𝐨𝐥𝐝.

- 𝓑𝒾𝓁𝓁 𝒞𝓁𝒾𝓃𝓉𝓸𝓃

English

Tax Bro retweetou

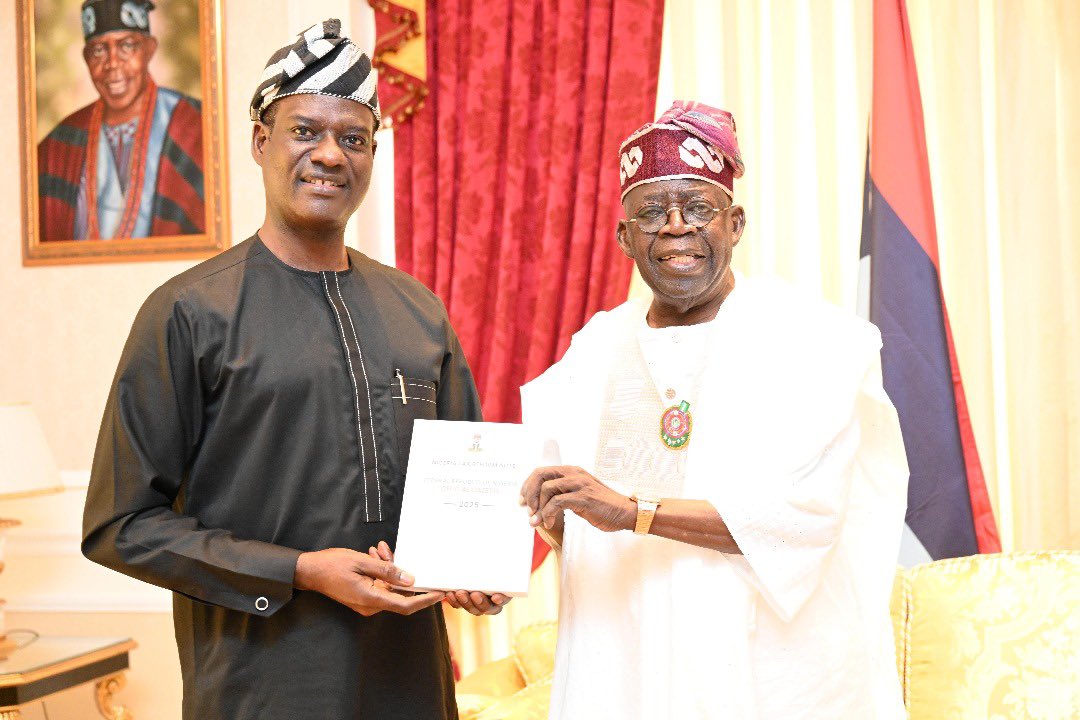

STATEHOUSE PRESS RELEASE

President Tinubu nominates Oyedele as minister of state for finance

President Bola Ahmed Tinubu has nominated Mr Taiwo Oyedele as the minister of state for finance, replacing Dr Doris Uzoka-Anite.

Uzoka-Anite will now move to the Ministry of Budget and National Planning, as the Minister of State, her third portfolio in the administration.

President Tinubu has today conveyed the nomination of Oyedele to the Senate for confirmation in a letter to the Senate President, Godswill Akpabio.

Until President Tinubu nominated him as a minister, Oyedele from Ikaram, Akoko, Ondo State, was the chairman of the Presidential Committee on Fiscal Policy and Tax Reforms, which overhauled Nigeria’s tax system.

Oyedele, 50, is an economist, accountant and public policy expert.

He attended Yaba College of Technology, where he obtained a Higher National Diploma (HND) in accountancy and finance. He attended Oxford Brookes University and earned a BSc in applied accounting.

He also completed executive education programmes at the London School of Economics, Yale University, the Gordon Institute of Business Science, and the Harvard Kennedy School.

Oyedele spent 22 years of his working career at PwC, joining in 2001 and rising to become the Fiscal Policy Partner and Africa Tax Leader.

Oyedele is also a professor at Babcock University in Ogun State and a visiting scholar at the Lagos Business School.

Bayo Onanuga,

Special Adviser to the President,

(Information and Strategy)

March 3, 2026

English

Thank you for all the love. I follow back everyone in the comments under this post.

I follow straight🙏

English

Tax Bro retweetou

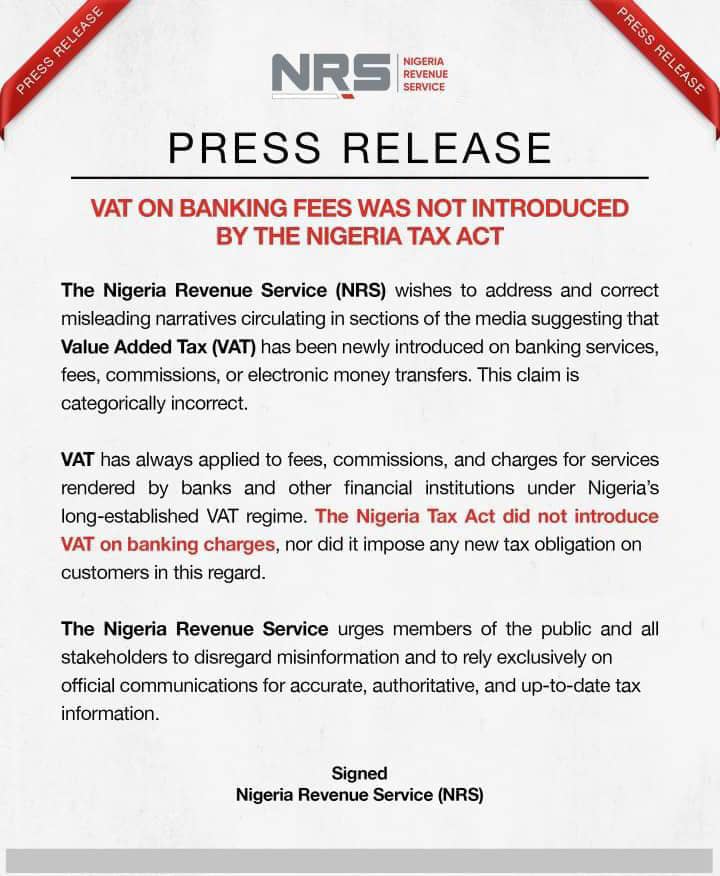

There is NO VAT on the money you transfer. VAT is only charged on the banking fee or commission which has been the case since VAT was introduced in 1993.

English

Tax Bro retweetou

Tax Bro retweetou

𝐑𝐞𝐬𝐩𝐨𝐧𝐬𝐞 𝐭𝐨 𝐊𝐏𝐌𝐆: 𝐎𝐛𝐬𝐞𝐫𝐯𝐚𝐭𝐢𝐨𝐧𝐬 𝐨𝐧 𝐍𝐢𝐠𝐞𝐫𝐢𝐚’𝐬 𝐍𝐞𝐰 𝐓𝐚𝐱 𝐋𝐚𝐰𝐬

---𝘉𝘺 𝘗𝘳𝘦𝘴𝘪𝘥𝘦𝘯𝘵𝘪𝘢𝘭 𝘍𝘪𝘴𝘤𝘢𝘭 𝘗𝘰𝘭𝘪𝘤𝘺 𝘢𝘯𝘥 𝘛𝘢𝘹 𝘙𝘦𝘧𝘰𝘳𝘮𝘴 𝘊𝘰𝘮𝘮𝘪𝘵𝘵𝘦𝘦

We welcome all perspectives that contribute to a shared understanding and successful implementation of the new tax laws. We acknowledge that a few points raised by KPMG are useful, particularly where they relate to implementation risks and clerical or cross-referencing issues. However, the majority of the publication reflected a misunderstanding of the policy intent, a mischaracterisation of deliberate policy choices, and, in several instances, repetitions and presentation of opinion and preferences as facts.

𝐆𝐞𝐧𝐞𝐫𝐚𝐥 𝐨𝐛𝐬𝐞𝐫𝐯𝐚𝐭𝐢𝐨𝐧𝐬

A significant proportion of the issues described as “errors,” “gaps,” or “omissions” by KPMG are either:

- the firm’s own errors and invalid conclusions,

- issues not properly understood by the firm,

- missed context on broader reforms objectives,

- areas where KPMG prefer different outcomes than the choices deliberately made in the new tax laws, and

- obvious clerical and editorial matters already identified internally.

While it is legitimate to disagree with policy direction, disagreements should not be framed as errors or gaps. KPMG would have been more effective if the firm adopted a similar approach like other professional firms who engaged directly providing the opportunity for clarifications and mutual-learning.

It is equally important to distinguish between policy choices designed to achieve the reform objectives and proposals that merely represent a firm's preference.

𝐏𝐨𝐥𝐢𝐜𝐲 𝐂𝐡𝐨𝐢𝐜𝐞𝐬 𝐚𝐧𝐝 𝐂𝐥𝐚𝐫𝐢𝐭𝐲 𝐨𝐧 𝐑𝐞𝐟𝐨𝐫𝐦𝐬

1. Taxation of Shares and the Stock Market

Contrary to the presumption that the new tax provisions on chargeable gains would trigger a sell-off on the stock market, the fact is that the applicable tax rate on share gains is not a flat 30%. The tax framework is structured from 0% to a maximum of 30%, which is set to reduce to 25%. Furthermore, a significant majority of investors (99%) are entitled to unconditional exemption, with others qualifying subject to reinvestment.

The market's performance, which is at an all-time high with increased investment flow, demonstrates investors understanding that the tax changes will enhance the fundamentals of firms both in terms of profitability and cash flows. The sell-off narrative is unsubstantiated as any disposals in December 2025 would have benefited from the re-investment exemption or enhanced deductions under the new law.

2. Commencement Date and Transition

The suggestion to set the commencement date as the start of an accounting period (e.g., 1 January 2026) takes a narrow view of the complex transition issues. A wholesale reform affects myriad issues beyond the accounting period, spanning multiple periods, different bases of assessment (preceding year, actual year), as well as issues related to audit, deductions, credits, and penalties. Limiting the commencement to a single date for accounting periods would fail to address the intricacies of continuous transactions and other transition matters. KPMG’s proposal is therefore not a “gold standard” to be applied to all new laws as suggested.

3. Indirect Transfer of Shares

The new provision to tax indirect transfer of shares is a policy choice aligned with global best practices and BEPS initiatives. Its objective is to block a long-exploited tax loophole by multinationals and other investors, not to affect competitiveness. This is a common provision in international tax, and the assertion that it may affect the country's economic stability is disingenuous.

4. VAT Exemption on Insurance Premium

KPMG's point regarding a specific VAT exemption on insurance premium is technically unnecessary, as an insurance premium is not a "taxable supply" defined under the Nigeria Tax Act. Insurance relates to risk transfer, not the supply of goods or services subject to VAT. As this has always been the administrative and legal position, a specific amendment for exemption is academic. If it is not broken, don’t fix it.

𝐈𝐬𝐬𝐮𝐞𝐬 𝐑𝐞𝐟𝐥𝐞𝐜𝐭𝐢𝐧𝐠 𝐌𝐢𝐬𝐮𝐧𝐝𝐞𝐫𝐬𝐭𝐚𝐧𝐝𝐢𝐧𝐠 𝐁𝐲 𝐊𝐏𝐌𝐆

5. Inclusion of 'Community' in Definition

The concern about the inclusion of “community” in the definition of a ‘person’ but its omission from the charging section does not constitute a gap or ambiguity. In statutory interpretation, definitions provided in the law apply wherever the defined term appears, unless the context requires otherwise. Hence, ‘person’ and ‘taxable person’ are used in the charging section, and both definitions include ‘community.’ This approach is consistent with modern legislative drafting principles, which use comprehensive definitions to streamline operative provisions and avoid redundancy. This is similar to the inclusion of partnerships and executors in the definition but not under the charging section. The use of the word “includes” further signifies that the list of taxable persons is not exhaustive.

6. Joint Revenue Board (JRB) Composition

The composition and mandate of the Joint Revenue Board (JRB) are intentional. Its policy advisory role is specifically to provide a subnational tax and revenue perspective that complements the fiscal policy mandate of the Ministry of Finance. Its membership is appropriately limited to revenue-focused agencies, which is why it is called the Joint Revenue Board. This is a similar composition under which the former JTB operated effectively, and its functions remain consistent with the need for inter-agency coordination.

7. Distinction in Dividend Treatment

KPMG's analysis appears to mix the distinction between a foreign-controlled company and a foreign operation of a Nigerian company. Dividends distributed by a foreign company cannot be "franked" since no Nigerian Withholding Tax (WHT) would have been deducted. Section 162(1)(s) confers exemption on dividend, interest, rent, or royalty derived from outside Nigeria and brought into Nigeria through approved channels. The choice to treat dividends distributed by Nigerian companies differently from foreign companies is a deliberate policy choice, as they are fundamentally different for tax purposes.

8. Non-Resident Registration and Final Tax

The view that a payment subject to deduction as final tax should automatically exempt the non-resident recipient from tax registration misses a critical distinction. While the law conditionally exempts passive income from registration, the deduction of tax on non-passive income is not synonymous with an exemption from registration or filing of returns. The same way that residents are required to file returns on income such as interest (in the case of individuals) and dividend where WHT is final. Returns serve a broader purpose beyond solely generating tax revenue.

𝐊𝐏𝐌𝐆’𝐬 𝐏𝐫𝐨𝐩𝐨𝐬𝐚𝐥𝐬 𝐓𝐡𝐚𝐭 𝐖𝐨𝐮𝐥𝐝 𝐔𝐧𝐝𝐞𝐫𝐦𝐢𝐧𝐞 𝐊𝐞𝐲 𝐑𝐞𝐟𝐨𝐫𝐦 𝐎𝐛𝐣𝐞𝐜𝐭𝐢𝐯𝐞𝐬

9. Tax on Foreign Insurance Premiums

The proposal to exempt foreign insurance companies from tax on premiums from insurance written in Nigeria to deepen penetration, while local insurance companies continue to pay tax, would be detrimental to the domestic insurance sector. This would create an unfair and harmful competitive disadvantage for local firms in their own market. The current policy is designed to protect and promote local industry and ensure a level playing field.

10. Parallel Market Forex Deduction

The new law disallows tax deduction for the difference where a business buys foreign exchange in the parallel market at a premium over the official rate. This is a critical fiscal policy choice designed to complement monetary policy, strengthen, and stabilise the Naira. By removing the tax subsidy for patronage of the parallel market, the policy aims to reduce incentives for round-tripping and redirect legitimate FX demands to the official market. This is policy congruence, not an error.

11. VAT Compliance-Linked Deductibility

The non-tax deduction for taxable transactions on which VAT has not been charged is a necessary anti-avoidance measure. It removes the advantage that some taxpayers previously enjoyed by patronising suppliers who evade VAT. This is a matter of fairness and is squarely within the control of a business to manage, especially given the provision for the self-charge of VAT. It also ensures that responsible businesses play their part in promoting voluntary tax compliance across the ecosystem.

12. Progressive Personal Income Tax

While KPMG acknowledges the reform objective of fairness and progressivity, the firm disagrees with a top marginal tax rate of 25% for the highest earners. In reality, the effective tax rate can be as low as 22% for an individual earning billions a year simply by contributing 10% to pension. This rate is competitive when compared to many other countries, including Angola 25%, Egypt 27.5%, Ghana 35%, Kenya 35%, the U.S. (Federal) 37%, South Africa 45%, and the U.K. 45%. So, the rate is not “oppressive” or one that will negatively affect economic growth as claimed, rather it ensures progressivity without compromising competitiveness. From a broader policy objective perspective, the increase in top marginal rate for high income earners and the reduction in corporate tax rate is designed to address the existing higher tax burden associated with business formalisation.

𝐅𝐚𝐥𝐬𝐞 𝐈𝐧𝐜𝐥𝐮𝐬𝐢𝐨𝐧 𝐚𝐧𝐝 𝐅𝐚𝐜𝐭𝐮𝐚𝐥 𝐄𝐫𝐫𝐨𝐫 𝐛𝐲 𝐊𝐏𝐌𝐆

13. Police Trust Fund

The Police Trust Fund was signed into law on May 24, 2019, with a six-year lifespan under section 2(2) of the Act, which ended in June 2025. Therefore, KPMG's point that the new tax law should be amended to repeal the taxing section of the Police Trust Fund Act is needless, as the provision no longer exists.

14. Small Company Verification

The analysis concerning the tax exemptions for small companies affecting large companies' obligations is not a new issue or an inconsistency in the new law. The small business threshold was introduced via the Finance Act 2021. This issue pre-dates the current tax laws and should not be presented as an error or omission simply by virtue of a higher tax exemption threshold under the new law.

𝐖𝐡𝐚𝐭 𝐊𝐏𝐌𝐆 𝐋𝐞𝐟𝐭 𝐎𝐮𝐭

While acknowledging the objectives of the reform, KPMG could have highlighted the major structural improvements under the new laws, including:

- simplification and tax harmonisation,

- the scope for reduction in corporate tax rate from 30% to 25%,

- expanded input VAT credits for businesses,

- tax exemption for low-income earners and small businesses,

- elimination of minimum tax on turnover and capital, and

- improved investment incentives for priority sectors.

A balanced assessment would have recognised these transformative elements, among others.

𝐂𝐨𝐧𝐜𝐥𝐮𝐬𝐢𝐨𝐧 𝐚𝐧𝐝 𝐖𝐚𝐲 𝐅𝐨𝐫𝐰𝐚𝐫𝐝

The tax reform is the result of an extensive consultation with various stakeholder groups in addition to the legislative process that included widely publicised public hearings, avenues intended for all stakeholders including international firms to provide technical expertise at the formative stage.

In any comprehensive overhaul of a nation’s tax framework, clerical inconsistencies or cross-referencing gaps may occur, and these are already being identified within the government. The tax reform represents a bold step toward a self-sustaining and competitive Nigeria.

An effective review needs to connect identified gaps to clear policy intents and the reality of modern-day tax systems within the context of economic development and global competitiveness.

At this stage, the effectiveness of the tax law depends on administrative guidance, clarifications from the tax authority, and regulations to complement precise statutory provisions where necessary pending future amendments.

We urge all stakeholders to pivot from a static critique to a dynamic engagement model, which allows for clarifications and a productive partnership in the implementation of the new tax laws.

English

Tax Bro retweetou

Hello NIUK Self Employed and Business Owners,

2024/25 self assessment is due by 31st January 2026. I am just a DM away.

Filing of self assessment, corporate tax returns, VAT returns and PAYE to the HMRC, my DM is opened.

Thank you.

Tax Bro@dee___why

Gentle reminder NIUK, I am a Professional Accountant and Tax Consultant. I can help you manage your business financials and taxes with the HMRC. I am just a DM away. Filing of self assessment, corporate tax returns, VAT returns and PAYE to the HMRC, my DM is opened. Thank you.

English

English

Tax Bro retweetou

𝐇𝐚𝐩𝐩𝐲 𝐍𝐞𝐰 𝐘𝐞𝐚𝐫, 𝐍𝐢𝐠𝐞𝐫𝐢𝐚

2026 is not just another new year, it marks a new chapter for Nigeria’s tax system as the remaining tax reform laws come into effect. This is a significant step toward building a simpler, fairer, and more growth-oriented tax system.

Wishing Nigeria a year of fiscal success, and Nigerians a year of shared prosperity.

#HappyNewYear2026 #TaxReforms #SharedProsperity

English

Tax Bro retweetou

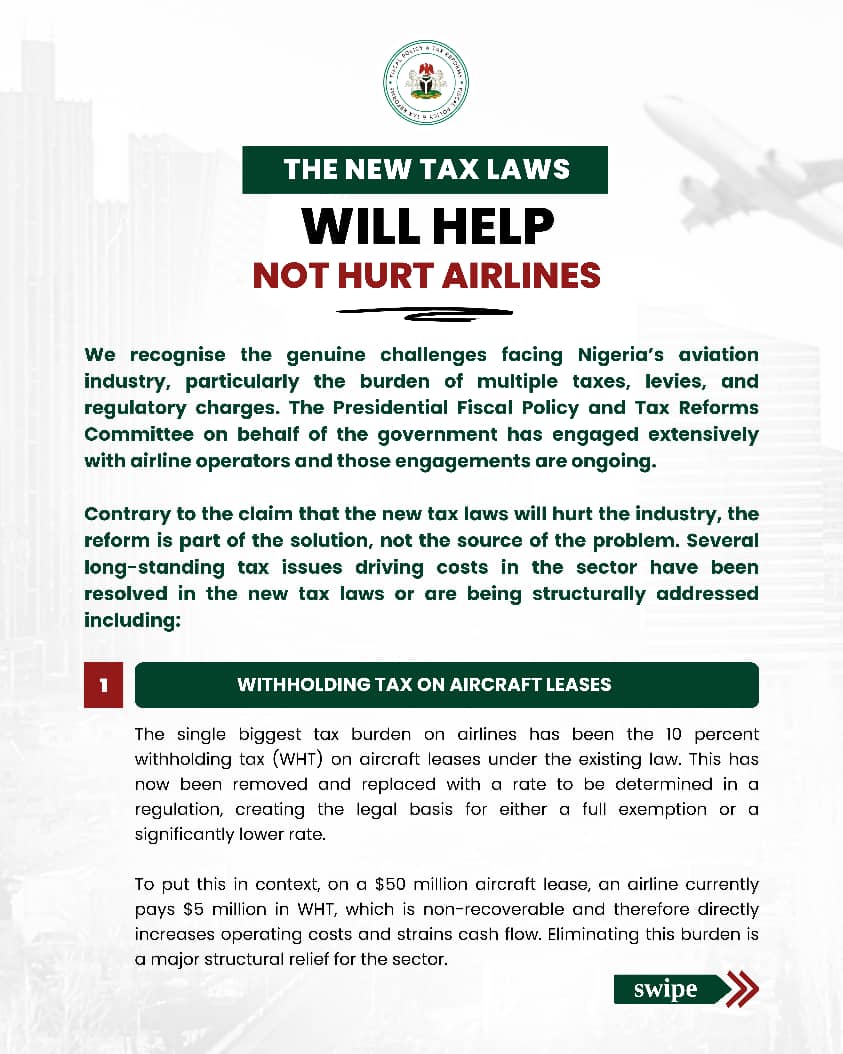

𝐓𝐇𝐄 𝐍𝐄𝐖 𝐓𝐀𝐗 𝐋𝐀𝐖𝐒 𝐖𝐈𝐋𝐋 𝐇𝐄𝐋𝐏, 𝐍𝐎𝐓 𝐇𝐔𝐑𝐓 𝐀𝐈𝐑𝐋𝐈𝐍𝐄𝐒

We recognise the genuine challenges facing Nigeria’s aviation industry, particularly the burden of multiple taxes, levies, and regulatory charges. The Presidential Fiscal Policy and Tax Reforms Committee on behalf of the government has engaged extensively with airline operators and those engagements are ongoing.

Contrary to the claim that the new tax laws will hurt the industry, the reform is part of the solution, not the source of the problem. Several long-standing tax issues driving costs in the sector have been resolved in the new tax laws or are being structurally addressed including:

1. 𝐖𝐢𝐭𝐡𝐡𝐨𝐥𝐝𝐢𝐧𝐠 𝐓𝐚𝐱 𝐨𝐧 𝐀𝐢𝐫𝐜𝐫𝐚𝐟𝐭 𝐋𝐞𝐚𝐬𝐞𝐬

The single biggest tax burden on airlines has been the 10 percent withholding tax (WHT) on aircraft leases under the existing law. This has now been removed and replaced with a rate to be determined in a regulation, creating the legal basis for either a full exemption or a significantly lower rate.

To put this in context, on a $50 million aircraft lease, an airline currently pays $5 million in WHT, which is non-recoverable and therefore directly increases operating costs and strains cash flow. Eliminating this burden is a major structural relief for the sector.

2. 𝐕𝐀𝐓 - 𝐅𝐫𝐨𝐦 𝐇𝐢𝐝𝐝𝐞𝐧 𝐂𝐨𝐬𝐭 𝐭𝐨 𝐓𝐫𝐮𝐞 𝐍𝐞𝐮𝐭𝐫𝐚𝐥𝐢𝐭𝐲

While the temporary VAT suspension introduced in 2020 following COVID-19 was attractive, it came with a hidden cost. Airlines could not recover input VAT on non-exempt items including certain assets, consumables, and overheads, meaning VAT became embedded in costs.

Under the new tax laws, airlines become fully VAT-neutral. Any VAT paid on imported or locally procured assets, consumables, and services will become fully claimable. Where an airline has excess input VAT, the law mandates a refund within 30 days, supported by a fully funded tax refund account and the option to offset VAT credits against other tax liabilities. This directly reduces cost pressure and improves liquidity.

3. 𝐈𝐦𝐩𝐨𝐫𝐭 𝐃𝐮𝐭𝐢𝐞𝐬

Existing exemptions on commercial aircraft, engines, and spare parts remain fully in place. There is no reversal or new burden introduced under the tax reforms.

4. 𝐈𝐦𝐩𝐚𝐜𝐭 𝐨𝐧 𝐓𝐢𝐜𝐤𝐞𝐭 𝐏𝐫𝐢𝐜𝐞𝐬

Airline operations are inherently low-margin. A 7.5 percent VAT on tickets, within a system where input VAT is fully recoverable, results in a significantly lower net impact than the headline rate suggests. Even in a worst-case scenario where VAT were not claimable, the maximum impact would still be 7.5 percent, not the price increases being suggested. That is, a N125,000 ticket becomes not more than N134,375 and a N350,000 ticket not more than N376,250.

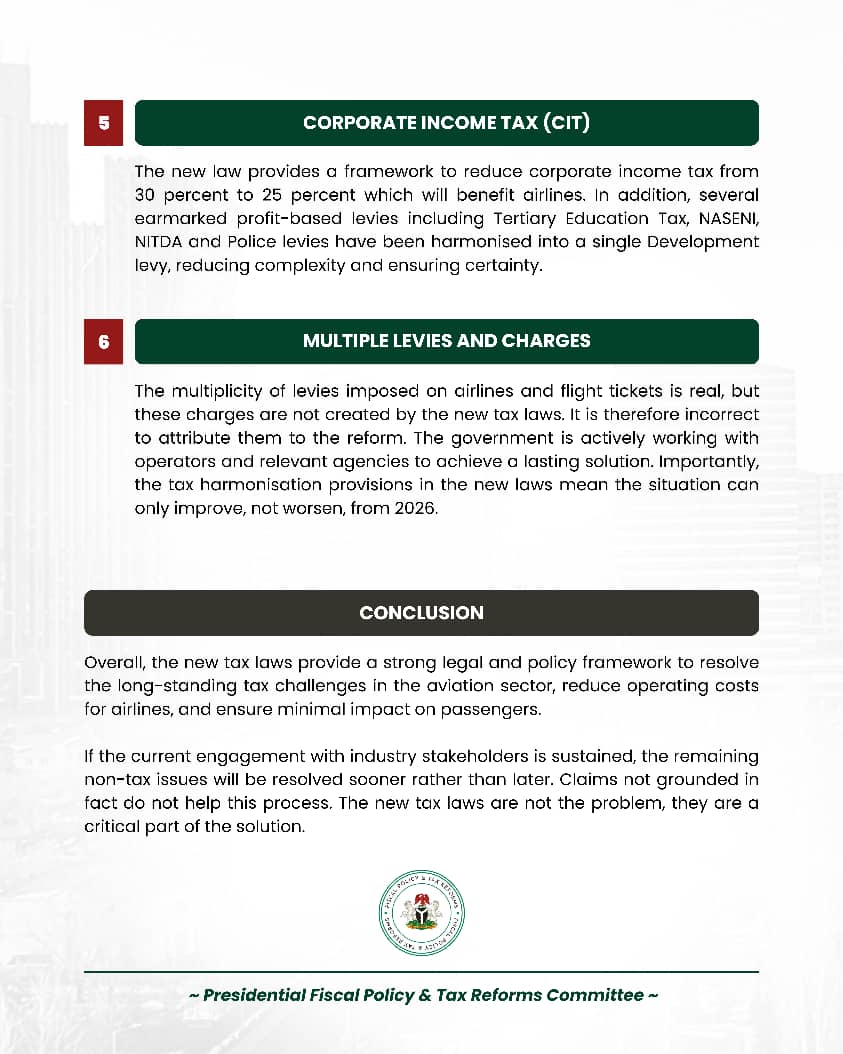

5. 𝐂𝐨𝐫𝐩𝐨𝐫𝐚𝐭𝐞 𝐈𝐧𝐜𝐨𝐦𝐞 𝐓𝐚𝐱 (𝐂𝐈𝐓)

The new law provides a framework to reduce corporate income tax from 30 percent to 25 percent which will benefit airlines. In addition, several earmarked profit-based levies including Tertiary Education Tax, NASENI, NITDA and Police levies have been harmonised into a single Development levy, reducing complexity and ensuring certainty.

6. 𝐌𝐮𝐥𝐭𝐢𝐩𝐥𝐞 𝐋𝐞𝐯𝐢𝐞𝐬 𝐚𝐧𝐝 𝐂𝐡𝐚𝐫𝐠𝐞𝐬

The multiplicity of levies imposed on airlines and flight tickets is real, but these charges are not created by the new tax laws. It is therefore incorrect to attribute them to the reform. The government is actively working with operators and relevant agencies to achieve a lasting solution. Import𝐓𝐇𝐄 𝐍𝐄𝐖 𝐓𝐀𝐗 𝐋𝐀𝐖𝐒 𝐖𝐈𝐋𝐋 𝐇𝐄𝐋𝐏, 𝐍𝐎𝐓 𝐇𝐔𝐑𝐓 𝐀𝐈𝐑𝐋𝐈𝐍𝐄𝐒

We recognise the genuine challenges facing Nigeria’s aviation industry, particularly the burden of multiple taxes, levies, and regulatory charges. The Presidential Fiscal Policy and Tax Reforms Committee on behalf of the government has engaged extensively with airline operators and those engagements are ongoing.

Check photos for more...

English

The Students’ Union appreciates everyone who joined the Naija Tax Shift: Student Edition X Space.

We sincerely thank our speakers for their time, insights, and clarity, and all participants for engaging in a meaningful conversation.

English

Tax Bro retweetou

We also appreciate Mr. Adedayo @dee___why for his kind support in offering to cover the application fee for students who participated in the Space and are interested in joining the KWASU Tax Club.

Interested participants are encouraged to send us a DM for further details.

English

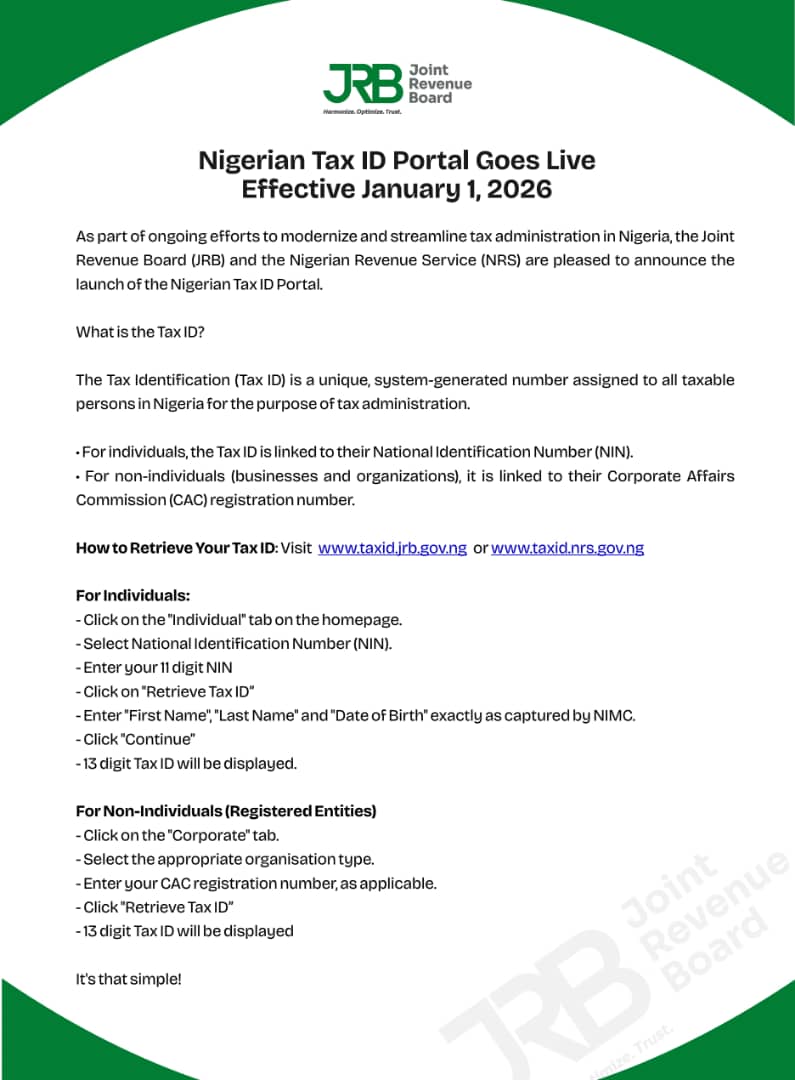

@TheKwasuSU Tax ID geenration link by Joint Tax Board.

taxid.jrb.gov.ng

English

Tax Bro retweetou

English

Tax Bro retweetou

𝐈𝐑𝐑𝐄𝐒𝐏𝐎𝐍𝐒𝐈𝐁𝐋𝐄 𝐉𝐎𝐔𝐑𝐍𝐀𝐋𝐈𝐒𝐌 𝐁𝐘 𝐏𝐄𝐎𝐏𝐋𝐄𝐒 𝐆𝐀𝐙𝐄𝐓𝐓𝐄

I usually ignore name calling because it is not worthy of attention that could otherwise be deployed productively. However, I am responding to this as a matter of public interest and hopefully to help other media organisations with similar tendencies.

Peoples Gazette published a malicious article claiming that I lied about certain provisions of the Nigeria Tax Administration Act. The accusation is false, reckless, and not supported by anything I said during the referenced TV interview.

It started with a WhatsApp message which I received from Peoples Gazette. Rather than wait for my response, they rushed to publish their accusation just after their first message below.

𝐏𝐞𝐨𝐩𝐥𝐞𝐬 𝐆𝐚𝐳𝐞𝐭𝐭𝐞: Good afternoon, Mr Ayodele. We followed your interview on Arise TV yesterday but found that you goofed and misrepresented the facts in the tax law. Contrary to your claims, Section 61 of the new law empowers the FIRS to seize Nigerians' money, properties without court order, for not paying taxes.

𝐓𝐚𝐢𝐰𝐨 𝐎𝐲𝐞𝐝𝐞𝐥𝐞: I will ignore your rude language since you obviously didn't understand my simple explanation. Send a screen recording of where I said what you claim. And my name is Oyedele, not Ayodele.

𝐏𝐞𝐨𝐩𝐥𝐞𝐬 𝐆𝐚𝐳𝐞𝐭𝐭𝐞: I know that your name is “Oyedele,” that was probably a typographical error. However, I wasn’t being rude to you, Mr Ayodele. During your December 24th interview on Arise TV, you claimed that the tax man (FIRS) cannot just seize people’s assets or money. This claim is contrary to the provisions in Sections 61 and 43 of the tax law. Here’s a clip from your interview: x.com/onejoblessboy/…

𝐓𝐚𝐢𝐰𝐨 𝐎𝐲𝐞𝐝𝐞𝐥𝐞: You can check the meaning of goof if that helps. If you're truly a professional journalist you won't jump into conclusion without due diligence. All you needed to do was watch about 2 minutes in the interview before the clip you shared, from the point the question was asked.

𝐖𝐡𝐚𝐭 𝐭𝐡𝐞𝐲 𝐜𝐨𝐧𝐯𝐞𝐧𝐢𝐞𝐧𝐭𝐥𝐲 𝐥𝐞𝐟𝐭 𝐨𝐮𝐭

My explanation clearly stated that enforcement actions do not arise in a vacuum. There is a process under the existing law which hasn’t changed – a taxpayer is entitled to self assessment, while the tax authority may issue an additional assessment to which the taxpayer has the right of objection, until the tax becomes final and conclusive under an appeal framework that involves the courts, up to the Supreme Court where applicable.

Peoples Gazette’s allegation relies on a short excerpt taken mid-response, stripped of the question and the explanation that immediately preceded it. Here is the full interview: youtu.be/GqhHq5XKr6A?si…

Responsible journalism requires due diligence, full context, and professionalism especially on a matter that is capable of misleading the public. Even if I said what they claimed, someone acting in good faith could have said “wrong” instead of “lied” but it was obviously intentional to gain the attention of their unsuspecting followers and get the clicks.

Falsehood may travel fast but only the truth can go far.

YouTube

English

Tax Bro retweetou

Meet our Professional Guest Speaker for #NaijaTaxShift (Student Edition): Adedayo Adebisi, ACA, ACTI.

He brings professional insight into Nigeria’s tax reforms and their practical implications.

December 29, 2025 | 🕗 8:00 PM

📍 X Space

#PeoplesEra #Tax

English