@zebrahoofbeat bitch 40 lakh people own ITC shares, why singling out doctors. #MedTwitter whore

English

meow

392 posts

👉Mainboard stocks often get all the attention but some of the most compelling businesses are hiding in plain sight — on the SME Platform. 👉Smaller. Less covered, though noisy at times. Yet occasionally, genuinely exceptional. ——— 👉Introducing SME Gems — a new independent series on Hidden Champions of the SME Platform : 💠 OBSC Perfection 💠 Aimtron Electronics 💠 Yash Highvoltage 💠 CFF Fluid Control 💠 DSM Fresh Foods 💠 L.T. Elevator 💠 Monolithisch India 💠 GSM Foils 👉Across Different Sectors. One common place. 🔗 smeresearch.github.io/SMEGems 👉Stay tuned for more insights ——— ⚠️ For educational purposes only. Not investment advice. Please DYODD. #SMEGems #SMEPlatform #HiddenChampions #SME

GOVERNMENT TEMPORARILY WAIVES ALL CUSTOMS DUTIES ON COTTON IMPORTS FROM JUNE 1 TO OCTOBER 30, 2026 LOWER IMPORT COSTS EXPECTED TO EASE RAW MATERIAL PRICES FOR TEXTILE AND APPAREL COMPANIES

Crazy dust storm in Bikaner, Rajasthan.

Le pire j’pense c’est les mecs qui vont a la salle pour faire ca

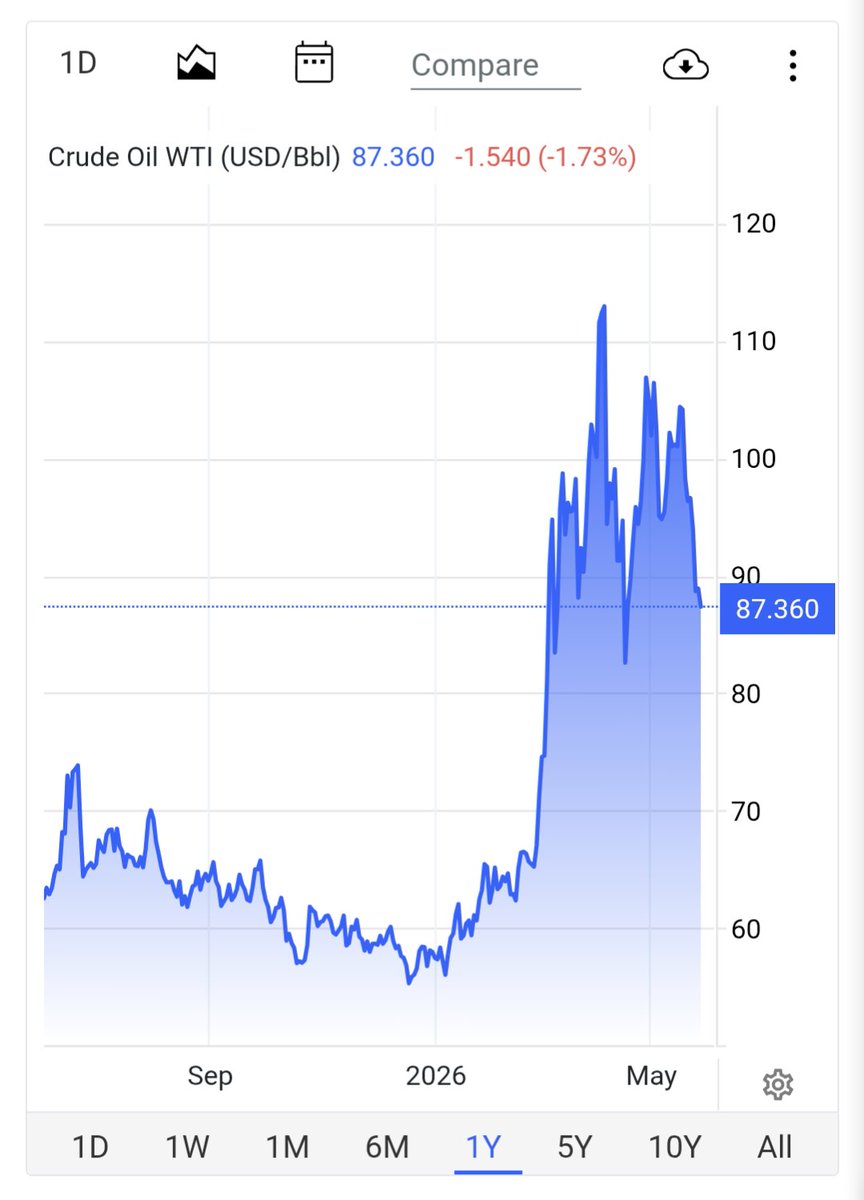

BREAKING || Unprecedented Drop in US Oil Prices - US oil prices drop below $87/Barrel

Stand out like a fuckin’ sore thumb. Miss the 90s when only a select few could afford to travel abroad. Much of the dehati filth remained confined to dehat that way. Class hierarchy is such an underrated social positive.

Emerald Finance Ltd Q4FY26 Results:- #Q4Results #Q4FY26 #Stockmarket #Nifty #Emerald 🟢 Total Revenue at 9.75 Cr vs 6.45 Cr (+51.13% YoY┃+24.97% QoQ) 🟢 PBT at 5.94 Cr vs 3.60 Cr (+65.06% YoY┃+11.26% QoQ) 🟢 PAT at 4.36 Cr vs 2.65 Cr (+64.35% YoY┃+8.95% QoQ) 🟢 PAT After Minority Interest at 4.05 Cr vs 2.56 Cr (+58.41% YoY┃+5.58% QoQ) 🟢 Strong all-round growth with consistent improvement across revenue and profitability metrics 🟢 Steady scaling in financial services business with healthy YoY and QoQ momentum Is Emerald Finance building a consistent micro-finance growth story or still in early-stage expansion phase? 🤔 #IndianStocks #ShareMarket #StocksToWatch