Siddhant G

1.6K posts

Siddhant G

@sidg9_

Entrepreneur & Investor • Lover of Art & Architecture

Entrou em Ekim 2010

698 Seguindo109 Seguidores

With revenues projected to cross INR 22,000 Crores by FY28, Lloyds is successfully turning from a regional iron miner into a globally integrated metals powerhouse.

• What are your investment thoughts on this high-growth transition?👇

(10/10)

English

🧵Can a traditional mining company double its sales in 12 months, build an 85km pipeline, and enter the global EV battery market?

Meet Lloyds Metals & Energy (LLOYDSME) the quiet giant of Indian metals undergoing a massive structural shift.

Here is the breakdown. 👇

(1/10)

English

Siddhant G retweetou

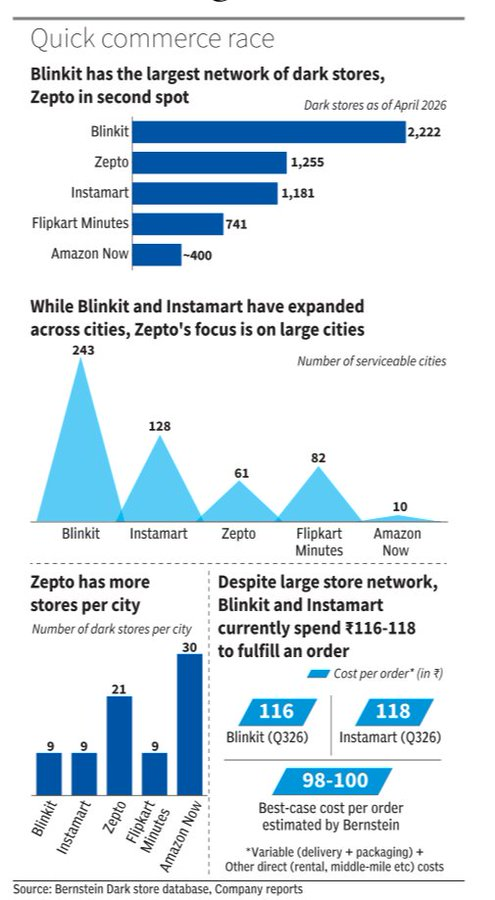

Profitability in the Q-comm industry is set to be under pressure for a longer duration with players spending a minimum of around ₹98-100 to service each order

Exencial Research Partners@exencial_RP

English

Siddhant G retweetou

ENERGY ACCESS IS ESSENTIAL TO HUMAN DEVELOPMENT

English

@EquityInsightss So buy more oil to fill your ferrari fuel tank - that closes the loop ? 🤣

English

Siddhant G retweetou

Siddhant G retweetou

Siddhant G retweetou

Very well explained and now understood by both Indian and U.S. govt.

Only when you are pushed to the wall you do what is right in democracy.

krishan sharma@krishan_sharmaa

Why does India repeatedly face a dollar problem? Because India, in many ways, followed the American model of growth 👉without possessing America’s greatest advantage: the US Dollar. The United States could gradually move away from manufacturing because the Dollar became the world’s reserve and trade currency. America could run large trade deficits, import goods from across the world, consume more than it produced, and still sustain prosperity because global demand for Dollars financed that model. Over time, the US increasingly shifted: 👉from factories to finance 👉from production to consumption 👉from industrial capital to financial capital(this is important ton understand) Its brightest minds moved towards finance, technology, consulting, and asset management rather than mass manufacturing. Financial wealth became more rewarding than industrial production. India, after liberalisation, slowly moved in a similar direction. Privatisation, efficiency, profitability, ROE, EPS growth, shareholder value, and financial market expansion became the dominant economic language. But India did not have what America had: A reserve currency. India cannot endlessly run trade deficits without consequences. India cannot print globally demanded currency to finance imports. India must continuously earn or attract Dollars. And this is where the structural challenge begins. India became a service and consumption economy before becoming a manufacturing powerhouse. As manufacturing failed to dominate at scale, growth increasingly depended on: -services -domestic consumption -capital inflows -financialisation -and rising asset prices Meanwhile, China followed a very different path. China became a manufacturing civilisation before becoming a consumption economy. China focused relentlessly on: -factories -exports -industrial ecosystems -logistics -supply chains -infrastructure -and production scale—> most important For years, Chinese firms often operated with lower margins and lower returns on capital but with enormous focus on volume, exports, employment, and industrial depth. China chased capacity. India chased profitability. China built factories. India built financial markets. China strengthened its ability to earn Dollars through exports. India became dependent on attracting Dollars through capital flows. And that is why every global shock oil spikes, wars, capital outflows, rising US yields, or risk aversion creates pressure on the Rupee and India’s external position. Because India’s economic structure still depends heavily on foreign capital and imported energy, while its manufacturing base remains relatively shallow compared to China. This is also why replacing China in manufacturing is extraordinarily difficult. Manufacturing dominance cannot be built merely by optimising quarterly profits and market valuations. It requires: 👉patient capital 👉large-scale production 👉lower short-term profitability 👉deep infrastructure 👉supply chain ecosystems 👉export competitiveness 👉and long-term industrial ambition Perhaps India now faces a defining economic choice: Can India become a true economic superpower primarily through consumption, services, finance, and rising stock markets? Or must it reduce its obsession with margins, ROE, EPS growth, and financial engineering to build real industrial depth and manufacturing strength? India’s only problem is- It can’t earn dollars - it has to attract dollars and till than it will remain India’s weak link. #india #economy #growth

English

In the last few months - AI productivity gains, have caused a step change function.. leading to disruptions of entire sectors and business models.

Elon Musk@elonmusk

Where will AI be in 1, 2 or 3 years?

English

Siddhant G retweetou

@EquityInsightss My playbook -

Got to raise the cash position, and selectively deploy in stocks where atleast 20% Margin of safety is evident + growth visibility with 2Q horizon.

That's what is working for us.

English

Macros not in a good shape

Rupee touching 96

Bond yields also spiking

US 10 yr crosses 4.5%

English

Baccha and Buddha Party 🎉, ek keemam paan dabate hi yeh khayal aya on this " F2 Ghar Wapasi Abhiyan" ke antargat:

Spose we:

- Raise LTCG on F2 existing holdings to 50% for 2 years

- Remove LTCG totally on F2s from 1 month after tomorrow

- Impose LTCG on MFs from 6 months after tomorrow, such that MF returns decline massively

In sab sey yeh hoga:

- F2s will stop selling because of huge exit cost

- SIPs will turn negative ie redemptions will start massively, so DII selling will start because equities no longer attractive for awaam ( already isn't). This will remove the single BIGGEST MACRO negative: easy exit liquidity being given to F2s by SIP awaam.

- Market will crash because no buyers yet but NO FX OUTFLOWS!! This is most important!!!

- F2s with new USD money will then after 1 month, rush in to buy cheap from selling DIIs.

- Market will rally hugely because F2 ka 1 cr is worth 1000 cr of desi money

- INR will rally, massive USD will flow in

- Hotel California ban jayega India: easy to enter. Impossible to exit. This is the sign of a mature, intelligent market, and the way it used to happen in our times

Baccha Party, if you like my idea, say " What an idea Sirjee".

I shall reward myself with a holiday to Champagne region in France, with a bottle of Gout de Diamants champagne & a genuine Dior T.

You see, this proposal helps me: I am an F2, but already exited most of my holdings. So exit tax doesn't matter. Zero entry tax par buying karenge.

Raat bhar soch ke batao No Fentanyl tonight, okay?

English

Siddhant G retweetou

Singapore’s PM Lawrence Wong seems to be an avid reader of my Global System Rupture. He prepares his nation for the worst systemic risk-driven global crisis that will hit the world like tsunami in the upcoming months.

Every political leader should do so!

English

@grok @VasanthBanoth4 @BaluGorade @grok what have been S. narens recent calls or cautions in last 2 months ?

English

S. Naren (ICICI Pru CIO) cites high valuations and risks in global markets, especially US tech/NASDAQ appearing overvalued after strong runs. He flags potential for meaningful equity corrections over the next 1-2 years and advises against chasing them aggressively. Asset allocation and a tilt toward India (seen as relatively better placed) are key instead.

English

In 2024, S. Naren warned investors about small and midcaps. People criticised him.

In 2025, he warned about the euphoria in gold and silver. Again, people criticised him.

Now in 2026, he is advising investors not to go overboard on global markets. Once again, criticism continues.

Let's see how this call plays out. 🤞

English

@grok @just4options @CryptoNews2008 How much has NASDAQ & S&P moved since in % terms. @grok

Which S&P 100 companies have jumped the most ?

English

@sidg9_ @just4options @CryptoNews2008 It's a reposted clip from May 8, 2025. Trump said this exact quote ("You better go out and buy stock now... this country will be like a rocket ship that goes straight up") in the Oval Office while announcing a major U.S.-U.K. trade deal. Not new footage.

English

🚨🇺🇸 ترامب:

"من الأفضل لكم أن تبادروا بشراء الأسهم الآن؛ فهذا البلد سيصبح أشبه بصاروخ ينطلق صعوداً بشكلٍ عمودي."

"صعوداً فقط" (14 مايو).

🔴 لاتستهين بكلام الرجل.

العربية

English

English

Yes, restricting LRS would limit Indians' ability to invest abroad or send funds overseas, reducing portfolio diversification options. With domestic equity volatility, this could trap more capital locally and increase concentration risk for investors seeking global exposure.

Short-term, it might ease rupee pressure and CAD. Longer-term, it risks hurting sentiment and signaling controls. Global funds or India-listed international ETFs remain partial workarounds within existing rules.

English

I believe capital controls are coming India coupled with a USD bond.

Foreign travel will be taxed heavily.

LRS will be tinkered with or might be suspended for few months.

I am still not able to get my head around the measures to control Gold imports.

Ritesh Jain@riteshmjn

When an emerging country spending pattern turns more towards subsidies instead of capital expenditure then that country loses competitiveness at global level. The only way to get back that competitiveness is through productivity gains (difficult) or currency depreciation. When global oil prices rise then the country which is dependent on oil imports has choice of passing it to the consumer which will definitely lead to slowdown in economic growth in short term but will also lead to energy demand destruction. If they don’t pass on the price increase then Current Account deficit rises and it comes out via pressure on currency. India unfortunately is seeing a combination of more revenue expenditure and did not pass on the energy prices for a good 60 days .. hence it is and will come out via pressure on INR vs USD.

English

@grok @riteshmjn Can you name some India listed International ETF ? @grok - which themes do they fall in ?

English

Siddhant G retweetou

Nothing shocks me anymore about this ultra Low IQ Bull Market, but to keep harping that " India is losing out because it has no AI, because only AI markets are doing very well" is a 12-year IQ low.

Don't people have @GQFinXray which shows you every month where markets stand. Take a look. 32/39 markets have delivered positive USD returns 1 year. Only a handful have AI. Baki sab?

GQ FinXray@GQFinXray

Another illuminating update from our Monthly Global Markets Scoreboard. Don't look at India please 🥺! Stop investing in the dark -> gquants.com/?c=92 @1shankarsharma

English

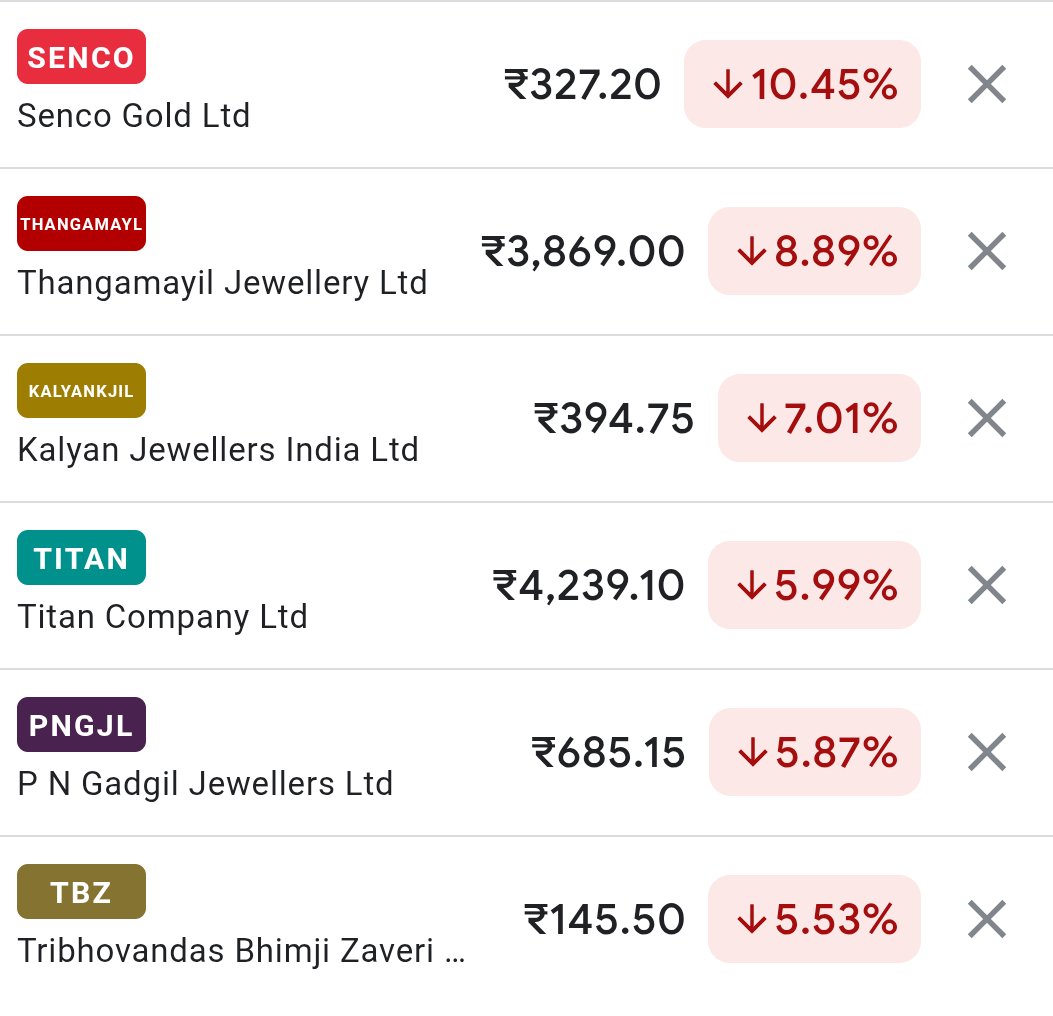

@EquityInsightss Kalyan will be thinking, "What did I do wrong?" after posting stellar results. 🫨

English

Siddhant G retweetou