@jukan05 Have you seen any charts to show forecasted supply vs forecasted demand? Recognize under supply until 2028 but unclear if post 2028 we’ll have massive over supply

English

Keep Prep Prom

9 posts

$NRP is starting to look interesting. This is a cheap coal (80% met coal) royalty business that has been on a deleveraging path for the last 10 years. The company will likely pay off its remaining debt this year and begin paying dividends. Considering that it trades at less than 4x FCF (ex. stake in soda ash biz), the start of dividend payouts should be a meaningful catalyst. Based on my estimates, there’s about 60% upside in this setup, even assuming $150M in norm. FCF ($220-230m last year), a level the company has almost never reached. During the low met coal pricing years (2015–16 and 2019), distributable cash flow from the coal business was between $187M and $214M, so $150M is a pretty conservative assumption. I’m capitalizing it at a 10% yield, which is more than reasonable given the quality of the royalty stream operations. This also excludes the COVID-affected years when distributable cash flow dropped to trough levels of $130M. Why is the company cheap? There are several reasons for NRP’s undervaluation. For one, it’s structured as an MLP, which by default limits the pool of interested investors. Additionally, coal remains an unloved industry among larger funds, so it’s no surprise the company trades at these levels. On top of that, we’re currently in a low coal and soda ash pricing environment due to weaker Chinese demand. Despite this, NRP operates a royalty business with minimum payment commitments and limited exposure to global pricing and volume volatility. As a result, even a highly conservative normalized FCF estimate of $150M seems to more than compensate for the majority of these supply and demand-side risks. The company owns 13m acres of mineral rights across various parts of the U.S., primarily for coal, most of which is metallurgical coal. These properties are leased for 5 to 40 years to some of the lowest-cost producers in the world. The mineral rights business generates about 80–85% of the company’s total distributable cash flow, with the remainder coming from its soda ash business. Leading up to 2016, the previous management team pursued an aggressive M&A strategy and took on significant leverage. When coal prices collapsed in 2016, the company nearly went bankrupt. The CEO was removed, and new management pivoted to a strategy focused on debt reduction and selling off non-core assets. To survive the debt burden, the company was also forced to issue preferred equity and warrants, though these later became an overhang. Last year, all of the preferreds and warrants were finally eliminated. Now, with just a minimal amount of debt remaining (= to 1y of FCF), the company is positioned to start issuing dividends. Finally, insiders own nearly 25% of the stock, so they’re well-incentivized to pursue buybacks or significantly higher dividend payouts.

New Post - Leon's $LNF.TO: A Real Estate Co. Masquerading as a Furniture Retailer -Leading furniture retailer in Canada -Stable profits and margins -Potential REIT of hidden real estate -Valuable land development project(s) -Est. 100% upside Read here: halviocapital.com/blog/leons-a-l…

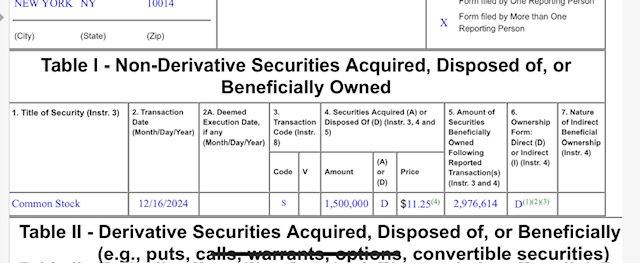

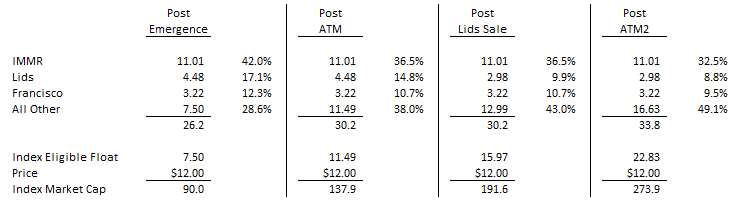

$BNED We had a call with $BNED CEO Jonathan Shar to follow up on the Q. Jonathan has a ton of energy and his excitement for the business opportunity was palpable throughout our conversation. He was extremely articulate about the value proposition of their offerings to students and how they drive educational outcomes. Penetration and market acceptance is increasing and there are robust tailwinds to the industry in a win / win / win for students, schools and professors. The user experience for students is also increasingly a selling point…no longer do students have to deal with standing inline at the book store before school…its often just a QR code scan now. Management also led with comments about First Day “Course” which is the smaller of the two First Day programs and more ala cart tied to individual course materials. The “Course” offering has substantial tailwinds on its own (it is growing slower than FDC) and can be an easier sale to make as a “first step” for schools skittish about fully adopting FDC out of the gate – but we note that FDC is growing fine on its own and many / most schools adopt the fully program without the intermediate step. $BNED sees the total TAM of ~16 mm post-secondary students as having the potential to be fully captured in the end by “First Day” programs; $BNED currently has 925k students enrolled in schools that have adopted FDC. The market is split roughly 30 / 30 / 30 / 10 between $BNED / Follet, self-operated (ie schools that run their own bookstores) and then 10% split between various smaller vendors. The recent new business wins touched on two themes: (1) Syracuse was previously a self-operated bookstore school that because of increasing complexity to operate their own store is now using $BNED…they expect additional self-operated schools may come to a similar conclusion over time and (2) North Carolina A&T was won back, after they left last year…the school found that $BNED had a superior offering and value proposition…management hopes that as the dust continues to settle from the restructuring that any lingering doubts about financial viability fade away. Store count has fallen from (split between physical and virtual) 774 / 592 = 1,366 stores in April 2023 (against FDC enrollment of 580k) to 653 / 509 = 1,162 (against FDC enrollment of 925k) as of the most recent quarter. It sounded to us that most of the heavy lifting with closing unprofitable stores is in the rear view mirror and we note that comp store sales were +3.8% in the most recent quarter. We didn’t appreciate that the virtual stores, while working everywhere, are especially positive for smaller schools. The store discussion ultimately reverted back to the TAM discussion, which we found interesting…under the old physical textbooks bought in actual stores model, many smaller schools were not economical to service. In the current world of digital course materials and virtual stores, these smaller schools are profitable and indeed can have strong economics for $BNED…all else equal, the market evolution means more / all of the TAM is addressable now. The $20 million of cost cuts achieved to date is mostly related to corporate overhead, which was bloated. Some of this $20 million is already in the numbers but a lot will flow through overtime. Coupled with the store rationalization, it sounds like there is more “meat on the bone” when it comes to optimization and this will continue to be a tailwind for numbers. Management was limited in terms of what they could say about the $40 million shelf offering. They did note the cash flow savings from lower interest expense and increasing financial strength. They seemed to suggest a greater ability to win new business was a partial dirver as well. While management didn’t comment on this, we would note that the share count getting over ~37.5 million shares (it will be ~34 if they issue the next $40 mm in equity and is currently ~30.5 million) would bring $IMMR under 30% and allow all of their shares to count towards the market cap used by the R2K $IWM - even excluding the $IMMR shares, $BNED is a near certainty to be added to the index this summer. In short, we left the call convinced of the business momentum and think the additional capital raises are extremely unlikely to be tied to a perception of future deterioration in the business; quiet the opposite, we left the call firmly convinced that our bear / base / bull case EBITDA projections are likely to prove conservative. Our math below assumes that they eventually issue enough shares to get to 37.5 mm outstanding. We note that overtime, net debt will trend to zero (~$20 million of capex) and buybacks will likely reduce the share count. As of April, the company had a $457 million NOL (likely lower now given CODI and actual positive net income). With pre-tax FCF per share of ~$2.00+ per share, likely to grow to $4+ in the intermediate term, we think the name warrants investor attention.