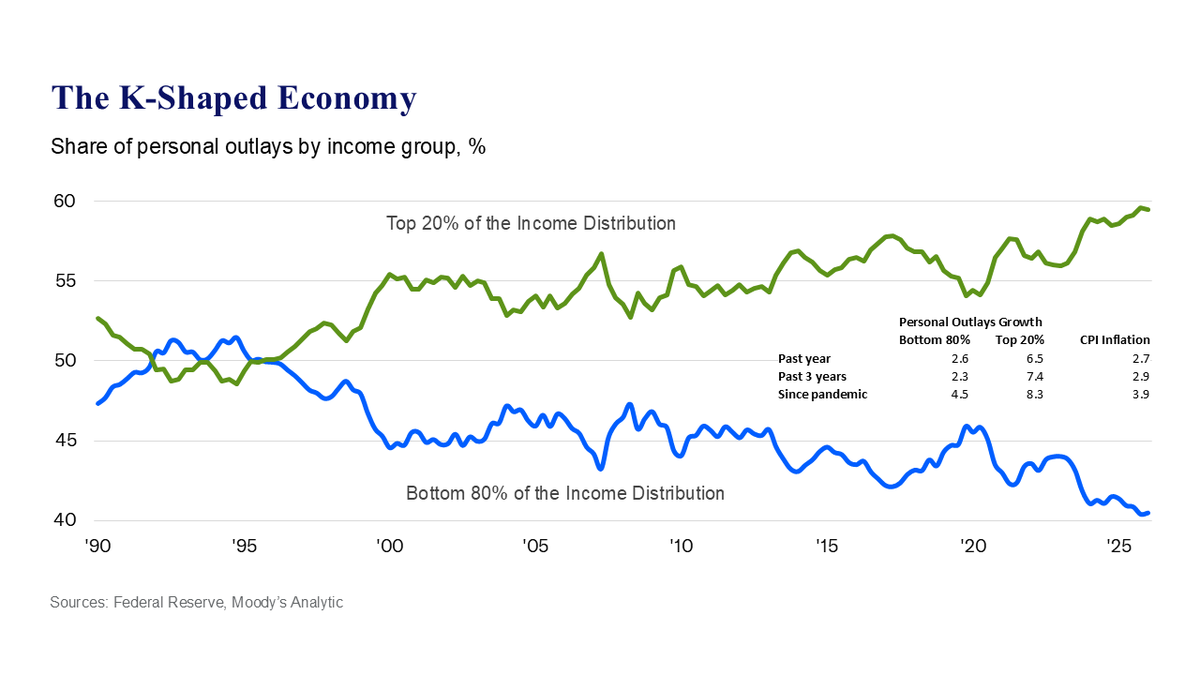

The K-shaped economy remains firmly intact. That’s according to our updated estimate of personal outlays by income group for 2026q1, based on the Fed’s Financial Accounts and Survey of Consumer Finance. Americans in the top 20% of the income distribution (those who earn over $175k annually) account for an astounding nearly 60% of outlays.

The top 20% is driving spending and the economy. Their outlays increased by 6.5% over the past year and by 7.4% per annum over the past 3 years, well above CPI inflation of 2.7% and 2.9%, respectively. But outlays by those in the bottom 80% fell short of inflation. No wonder most Americans are upset with their financial situations and the broader economy.

ICYMI, our estimates have come under some criticism. Fair enough. While we use a methodology devised by Fed researchers long ago, even with the modest adjustments we have made, these estimates may overstate the case. But they make an overwhelming case that the economy is K-shaped and becoming increasingly so. Our methodology is an open book: economy.com/getfile?q=8D6D…

English