Millionaur รีทวีตแล้ว

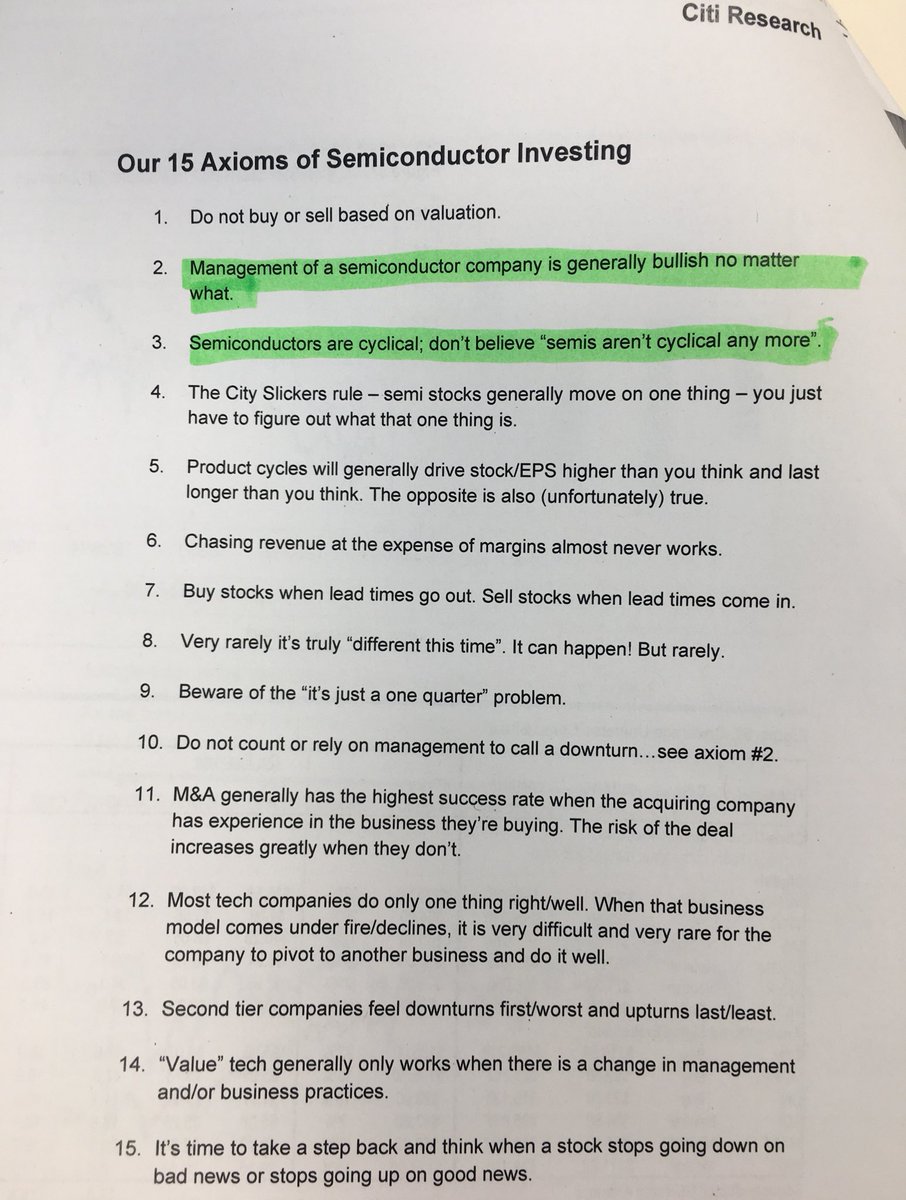

Citi Research’s first axiom for semiconductor investing:

“Do not buy or sell based on valuation.”

This tells you all you need to know about Wall Street.

English

Millionaur

10.4K posts

@millionaur

eToro Popular Investor 🤖AI ⛏️metals ♻️energy 💊biotech 🧬 Bitcoin, Ethereum since 2017 🏂 riding technology & debt cycles

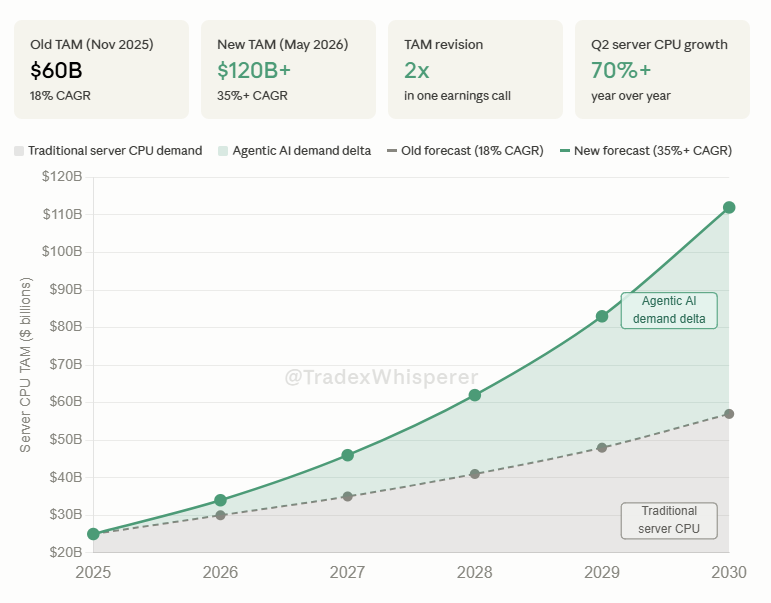

$AMD $INTC AI Inference & Agentic AI Tailwind. Is Market finally pricing in the CPU necessity? -AMD CEO Lisa Su disclosed at the March 2026 Morgan Stanley TMT Conference that server CPU demand has "far exceeded" prior forecasts. -Meta and AMD announced a five year, $60 billion agreement anchored by 6th Gen EPYC "Venice" CPUs paired with next-gen GPUs, with workload-specific tuning for inference-heavy environments. -Intel and SambaNova are building a disaggregated inference architecture specifically for agentic AI. Intel Xeon 6 CPUs handle agentic tool execution and system orchestration. SambaNova RDUs handle LLM decode. GPUs handle prefill. -In agentic pipelines, the orchestration layer accounts for 50 to 90% of total system latency. That makes CPU performance the rate-limiting variable. Not VRAM. Not FLOPS. -Deloitte forecasts that inference will make up two thirds of all AI compute by 2026, far exceeding initial training costs.

The power grid upgrade is probably one of the clearest themes for the next 3-5 years. Aside from $XLU, the best names at current valuations I think are: 1. $ITRI: Smart grid, metering, and utility tech. 2. $FLNC: BESS for grid stability. If you're bullish on solar and wind energy, then BESS for stability is going to have huge demand. Slight issues with profitability, but trades very low for the growth. 3. $AES: The "safer" play with PPAs from $GOOGL and other hyperscalers. 4. $MYRG: Electrical infrastructure contractor trading at 17x NTM EBITDA for 18% EBITDA growth. 5. $PWR: So far, the clear winner but trades at a PE of 43x ahead of the pack. All of these plays are going to benefit from huge tailwinds in the sector. - Rate cuts - Huge CapEx cycle expected to top $1T in a couple years

Agreed high-level directionally, $FLNC compelling at $3B valuation post-earnings after taking a closer look. Very rare to see a US energy player that small get 2 direct Hyperscaler deals... The $5.6B+ backlog derisks the company growth, not including new hyperscalers backlog like $GOOGL or $MSFT. The hyperscaler deals were framework agreements, which are likely to convert "soon" Q3 this year, and aren't included in numbers. Once that's released it's major positive catalyst, similar to qualification -> volume ramp in semi players. Citi Analyst: "The possibility of a hyperscaler order will likely overshadow everything else in the quarter. We expect a positive reaction to the announcement" I'm going to go ahead and guess they'll likely rerated once they announce their hyperscaler orders maybe anytime in the next 3 months so I jumped on the boat as a short term catalyst trade. (not just 1 but 2) Also, if they hit ~$288M net income off gross-margin expansion ($6B revenue, 13.0% gross margins) from their software segment expansion, ~11.6x fwd p/e for 2027. The current stock price is -50% Feb's prices despite hyperscalers + backlog de-risking the company looks like a great entry point to me (NFA).

$AAOI reports earnings tomorrow and this is what I'm expecting. 2025 revenue was $456M. Management guided $1B+ for 2026 with $120M+ in non-GAAP operating profit. The business is set to more than double in a single year after running $190-250M annually from 2019 through 2024. > Q1 guide is $150-165M vs Street at $157M. CATV running hot, 800G firmware slip from Q4 pushed shipments into Q1, and they beat EPS by 91% last print. Setup favors a beat. > Q2 is what matters. Management has telegraphed it as the first profitable quarter and the start of the 800G/1.6T ramp. Above $185M with positive NG EPS and the move continues. > OFC capacity slide showed 650K combined 800G + 1.6T units/month by Q4 26, 30% above prior guidance. 930K/month by Q4 27. That's a ~$6B annualized run rate from two product lines against a $14B market cap. Full pre-earnings breakdown linked below. $AAOI $LITE $COHR $AEHR $VIAV