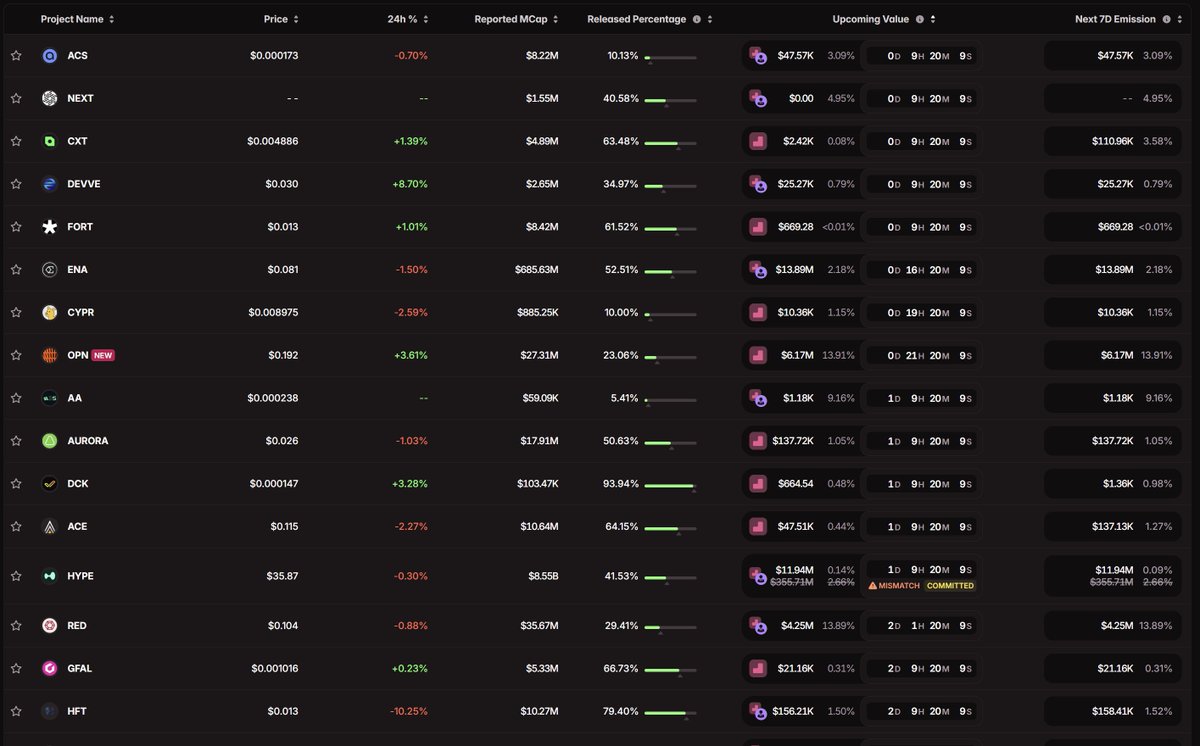

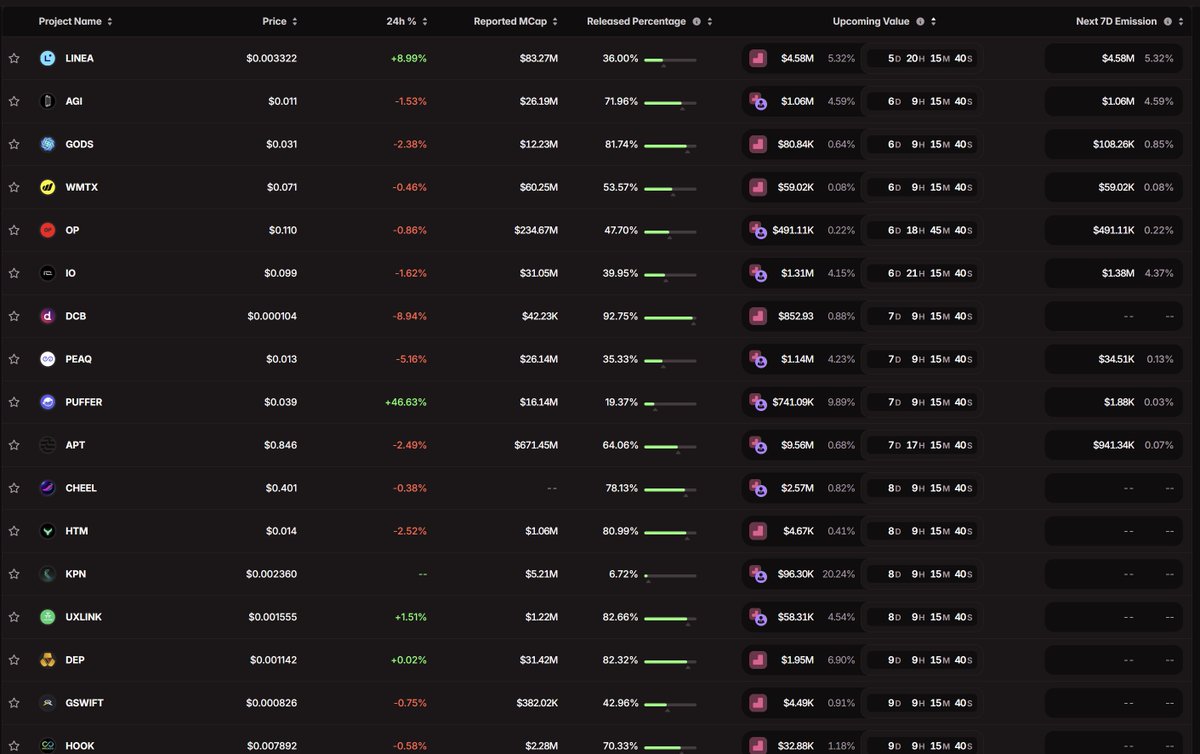

Upcoming unlock schedule for 50 tokens. I only focus on trading Futures when it is a Cliff Unlock event and the unlocked volume is greater than 25% of daily trading volume. If you are focused on long-term investing, keep an eye on these events as well to optimize better entry points after each unlock.

At the moment, there are 8 unlock events worth watching because the unlocked volume is high relative to daily trading volume:

$ENA - 26.56%

$OPN - 36.51%

$RED - 118.06%

$MOVE - 29.80%

$BABY - 84.65%

$AGI - 114.57%

$PEAQ - 47.50%

$APT - 29.15%

#TradingSetup#MarketInsights

Global crypto markets stayed range-bound in the week of March 29–April 4, but the overall tone remained defensive rather than constructive.

🌐 This week, crypto largely stayed trapped in a narrow range as total market capitalization hovered around $2.4T while liquidity and trading volume fell noticeably from the previous week. $BTC mostly moved between 65.5K and 68.5K, $ETH held around 1.98K–2.05K, and most altcoins continued to lag without a clear leadership narrative.

📉 Overall sentiment remained cautious, with the Fear & Greed Index stuck in Extreme Fear for weeks, funding rates in derivatives staying negative, and long positions still facing liquidation pressure. This structure points to a market that is no longer in deep panic, but still not ready to fully re-embrace risk.

🛢️ The biggest pressure point this week was still the macro and geopolitical backdrop, especially Middle East tensions pushing oil prices higher and keeping global capital tilted toward defense. At the same time, the Fed’s still-firm rate stance and US economic data continued to limit the odds of a sustained rebound in risk assets, including crypto.

⚠️ Within the industry itself, the nearly $285M exploit at Drift Protocol became the biggest crypto-native shock of the week, weakening confidence in DeFi and adding pressure to the $SOL ecosystem. On top of that, early-April token unlocks and continued distribution from larger wallets kept dilution pressure on altcoins, even as retail flows showed signs of gradual accumulation.

🏦 The more constructive side is that the longer-term picture has not broken down. Spot $BTC ETFs posted positive net inflows for March, several traditional financial firms kept expanding crypto spot trading infrastructure, and total stablecoin supply continued to grow across the market. That suggests institutional capital has not left the sector, but is still waiting for a clearer trigger before scaling exposure again.

🔎 In the short term, the market still looks like it is waiting for a fresh catalyst, with $BTC support around 65K–66K and nearby resistance around 68K–70K. Until there is a stronger breakthrough from policy, ETFs, or a clearer easing in geopolitical risk, crypto will likely remain range-bound with a mildly defensive bias.

#CryptoInsights#MarketOutlook

Greece reshuffles its cabinet to contain the widening fallout from the EU farm subsidy scandal

🌍 Prime Minister Kyriakos Mitsotakis’s cabinet shake-up shows Athens is trying to contain the political damage from the EU farm subsidy scandal before it grows into something larger than an administrative controversy.

🧾 The focus is OPEKEPE, the agency handling more than EUR 2 billion in farm aid each year, where authorities allege false pastureland claims were used to secure subsidies improperly. The fact that the EU had already fined Greece EUR 392 million over weak oversight makes this episode even more damaging for the government’s image.

🏛️ The appointment of Margaritis Schinas as agriculture minister looks more like an effort to reassure Brussels than a sign the problem has been resolved. The new cabinet may help stabilize the government in the near term, but it does not address the deeper flaws in the subsidy system.

⚠️ The bigger risk now lies in the investigation itself, with EPPO seeking the lifting of immunity for several current and former lawmakers. If the case keeps expanding, it could turn into a prolonged political drag on New Democracy ahead of future election debates.

#Europe#PoliticalRisk

Global chemical markets in the week of Mar 29–Apr 4, 2026 showed how the Middle East shock rapidly reversed the short-term supply-demand balance.

⚗️ This week, the global chemical market was driven almost entirely by the Middle East conflict, as disruptions around Hormuz broke key feedstock flows across the petrochemical chain. From ethylene and naphtha to glycols and polymers, the market shifted quickly from oversupply and weak pricing into localized shortages and a sharp cost surge.

📈 Price reactions came fast at the start of April. Asian PE jumped 40–50%, production costs nearly doubled, while Europe’s April ethylene contract price surged another €450/t to around €1,595/t, marking one of the strongest increases in years. Singapore naphtha also climbed toward $1,000/mt, triggering broader hikes across polymers, solvents, glycols, and intermediate chemicals.

🌏 Asia remained the center of supply pressure as ethylene and derivative availability tightened sharply, forcing several plants to cut rates or halt production. Europe faced additional pressure from rising energy and feedstock costs, along with the risk of Q2 import shortages, which pushed buyers toward defensive restocking. Meanwhile, the US saw temporary support from cheaper gas-based feedstock, more stable operating rates, and stronger export potential into undersupplied regions.

🏭 The shock did not stay limited to base petrochemicals but spread quickly into downstream segments such as packaging, engineering plastics, polyurethane, coatings, and even fertilizers. That suggests the market is no longer dealing with a simple feedstock rally, but with a broader regional split shaped by logistics, cost structures, and access to supply.

⏳ In the near term, this was one of the most volatile weeks for chemicals since the start of 2026. If disruptions around Hormuz persist, shortages and price pressure could easily extend into Q2; even if transport flows normalize, a full return to previous conditions is unlikely in the short run.

#ChemicalMarkets#CommoditiesInsight

BOJ keeps the door open for more rate hikes even as the Iran conflict adds pressure to Japan’s economy

🟦 BOJ’s latest remarks suggest policy is still leaning hawkish, even as the Iran conflict pushes oil prices higher and makes the business environment more difficult. The key takeaway is that Japan’s central bank does not see this as a reason to step back from policy normalization.

🟨 For an economy heavily reliant on imported energy, higher oil prices and a weaker yen are driving input costs up more quickly. Even so, BOJ believes this shock could feed into underlying inflation more strongly than in the past, as companies are now more willing to raise prices and wages.

🟥 That means the Middle East conflict is not only a growth risk, but also a factor that strengthens the case for further tightening. Markets are therefore leaning toward a scenario where BOJ could deliver another 0.25% hike at the late-April meeting or, at the latest, in June.

🟩 If that scenario is confirmed, JPY could find near-term support, while Japanese equities may continue to face pressure from higher costs and tighter profit expectations.

#ForexInsights#MarketUpdate

Global Energy Market Overview for the Week of March 29, 2026 – April 4, 2026

⛽ Global energy markets stayed locked in a supply-shock narrative during the week, as disruption around Hormuz kept geopolitics at the center of price action. The market was no longer reacting only to headline risk, but increasingly to the possibility of a prolonged physical supply squeeze, which kept volatility elevated across the entire complex.

🛢️ Oil remained the main focus, with WTI briefly slipping below $100 per barrel before rebounding toward $111, showing how tightly the market is trading between technical pullbacks and renewed supply fears. Even a large build in U.S. crude inventories did little to calm sentiment, because traders were more concerned about whether April would bring deeper shortages than what weekly stock data alone could offset.

🔥 The more important shift was that the shock spread well beyond crude. Global LNG flows came under pressure as Qatar-related risks and Hormuz disruption tightened available supply for Asia and Europe, while U.S. Henry Hub stayed relatively subdued thanks to warm weather, strong gas production, and comfortable storage. That contrast reinforced the role of the U.S. as a key balancing supplier for the global gas market.

🚚 Further downstream, higher diesel, jet fuel, and transport costs showed that the energy shock is already feeding into the real economy. Rising fuel prices are not only adding to inflation pressure, but also pushing up costs for airlines, logistics, and fertilizers, increasing the risk of broader spillover into industrial and food supply chains in the coming weeks.

📌 Looking ahead, the market will focus on the April 5 OPEC+ meeting and any signal on whether Hormuz can normalize. If supply conditions remain constrained, energy prices are likely to stay elevated and highly volatile; if tensions ease, upside momentum may slow, but the market would still remain structurally tight for now.

#EnergyMarkets#OilAndGas

Japan Steps Up FX Warning as USD/JPY Moves Closer to 160

💱 Japan’s Finance Minister Satsuki Katayama signaled a firmer stance on the currency market on April 3, saying the government is closely monitoring sharp moves and is ready to respond comprehensively if speculation keeps pushing FX volatility higher.

📉 The focus is now on USD/JPY, which climbed to 159.59 and moved very close to the key 160 threshold, while the yen has weakened about 2.3% since the U.S.-Israel military campaign against Iran increased geopolitical tension, lifted oil prices, and strengthened demand for the dollar.

⚠️ What stands out is that Tokyo is still relying on verbal intervention rather than actual market action, but the tone has clearly become more forceful. That is enough for traders to start repricing intervention risk around the 160–162 area, where Japan stepped in before.

🧭 For traders, carry trade conditions are still attractive, but the safety margin is getting narrower. If oil keeps rising and USD/JPY pushes higher, the risk of sudden volatility triggered by Japanese authorities will become more significant.

#ForexInsights#YenWatch

Global agricultural markets saw sharp swings in the week of March 29 - April 4, 2026 as traders reacted to the USDA’s Prospective Plantings and Grain Stocks report, while the FAO food price update and rising Middle East tensions added fresh pressure through energy, fertilizer, and freight costs.

🌾 The market moved around two main catalysts: the USDA report on March 31 and the FAO Food Price Index released on April 3. At the same time, higher oil prices linked to Middle East tensions pushed production and transport costs higher across the farm sector.

📈 The USDA data reshaped expectations for 2026 US supply. Wheat acreage fell to 43.8 million acres, near historically low levels, helping futures jump after the report. Corn at 95.3 million acres and soybeans at 84.7 million acres triggered a more mixed reaction, with an early rally followed by profit-taking.

🌍 On the global side, the FAO Food Price Index rose to 128.5 in March, up 2.4% from the previous month and marking a second straight monthly increase. Vegetable oils, sugar, and grains led the move higher as expensive crude, firmer biofuel demand, and rising logistics costs filtered through the supply chain.

🌽 Price action became increasingly selective. Wheat stood out on tight acreage and dry, hot weather in the US Plains. Vegetable oils and sugar also stayed firm as soy oil, palm oil, and ethanol-related demand benefited from elevated energy prices. Corn and soybeans mostly traded on technical flows after the USDA release, while rice remained under pressure from ample Asian supply and intense export competition.

☀️ Weather remains a key risk into April. The US Plains stayed dry and warm, worsening winter wheat conditions, while Brazil’s strong soybean harvest still contrasts with concerns over delayed safrinha corn and declining soil moisture. Argentina also continues to face weather pressure late in the season.

🚢 Another theme was the rebound in freight costs as shipping routes tied to Hormuz were repriced for risk. It has not caused an immediate supply shock yet, but it is lifting the cost base for global agricultural trade and could help support prices if disruptions last longer.

🔎 Overall, the week leaned mildly bullish for wheat, vegetable oils, and sugar, while corn and soybeans remained caught between abundant supply and rising cost risks. The next focus is the April 9 WASDE report, along with US weather and the direction of energy prices.

#AgriMarkets#CommodityInsights

Al Taweelah has become a new pressure point for global aluminium supply risk.

⚙️ The March 28 attack forced EGA’s entire Al Taweelah complex into an unplanned shutdown, with heavy damage across key aluminium and metal-processing units. The sudden power loss disrupted operations in a way that will not be easy to reverse, showing this is not a short-lived operational setback.

📉 What matters for the market is that Al Taweelah is EGA’s core asset, producing around 1.6 million tonnes of cast aluminium in 2025. When a facility of that scale is hit, supply risk stops being a local issue and starts feeding into the broader industrial metals chain.

⏳ According to EGA’s latest update, a full recovery in primary aluminium production could take up to 12 months. That timeline is long enough for the market to reprice geopolitical premium, especially with the Middle East already a sensitive region for both energy and metals.

📈 In that setting, aluminium prices remain clearly supported in the near term, while market attention will stay fixed on EGA’s next updates. This is no longer just a story about damage at one company, but about how vulnerable global aluminium supply can be when geopolitical shocks hit.

#AluminiumMarket#CommodityInsights

Global stock markets overview for the week of 29/03 - 04/04

🌍 Global equities staged a clear rebound this week after the earlier selloff, as hopes for easing U.S.-Iran tensions helped improve overall risk sentiment. The recovery came right after a highly volatile March, showing that markets are still reacting very quickly to any sign of reduced pressure in the Middle East.

📈 In the U.S., the S&P 500 rose more than 3%, the Dow Jones gained nearly 3%, and the Nasdaq advanced more than 4%, ending a five-week losing streak. Europe also moved sharply higher, with the STOXX 600, DAX, CAC 40, and FTSE 100 all posting strong gains, reflecting a clear relief rally as investors temporarily dialed back concerns over prolonged energy supply disruption.

🔄 Sector rotation was also a key feature of the week. Technology, financials, materials, and real estate led the upside, while energy lost momentum after its earlier surge as oil pulled back from peak levels. That suggests the market is leaning toward the view that the oil shock has not yet turned into a broader new risk spiral.

🌏 Even so, the global picture remains uneven. Asia was generally weaker, especially Japan, where high oil prices and the prospect of a still-hawkish BoJ continued to weigh on sentiment. China and Hong Kong posted only limited gains, suggesting that the current rebound still looks more like a short-term reaction than a fully confirmed broader uptrend.

⚠️ Risks remain firmly in place because oil is still elevated, market volatility has not returned to normal, and major U.S. indices are still negative year to date. The relief rally has eased some pressure, but the durability of this rebound will still depend heavily on geopolitics and on how far the energy shock feeds into inflation expectations.

👀 Next week, markets will likely stay focused on any new signals from the Middle East as well as key U.S. inflation data. If oil continues to cool and price pressure does not accelerate too quickly, the rebound may extend further; otherwise, any renewed escalation could quickly push global volatility higher again.

#StockMarket#GlobalMarkets

JERA’s exit from a long-term LNG deal with Commonwealth suggests major buyers are becoming more cautious toward U.S. projects that have not yet reached final investment decision.

📘 JERA has terminated its agreement to buy 1 million tons of LNG per year for 20 years from Commonwealth LNG, effective March 3, although the market only paid close attention after the DOE filing in early April. A notable point is that neither side disclosed an official reason.

⚖️ In essence, this is not a short-term supply shock because Commonwealth still has not reached FID and its startup timeline has already been pushed back to 2031. That keeps the immediate impact on spot LNG prices limited, but it does raise psychological pressure on U.S. projects that are still trying to secure financing and buyers.

📉 For Commonwealth, losing a major buyer like JERA is a negative signal for its commercial credibility. For JERA, the move shows that buyers are now prioritizing projects with clearer execution timelines rather than locking in long-term volumes from projects that still carry substantial uncertainty.

🌍 In the broader picture, this event reflects a more selective phase for the LNG market. Long-term demand has not disappeared, but the bar for new supply is now clearly higher.

#LNG#EnergyMarkets

Global Forex Market Overview for the Week of March 29, 2026 – April 4, 2026

🌍 The forex market closed the week with a clear tilt toward the U.S. dollar as U.S.-Iran tensions continued to dominate global sentiment. The main driver was not only safe-haven demand, but also the sharp jump in oil prices, which revived inflation concerns and pushed markets to scale back expectations for early Fed rate cuts.

🛢️ WTI and Brent traded in the $94–105 per barrel range, with intraday spikes of more than 10%, putting clear pressure on energy-importing economies. That left the euro, pound, and yen facing a double hit from both risk-off flows and renewed concerns over rising energy costs, while the dollar benefited from its defensive role and stronger rate expectations.

📈 The DXY held within the 99.5–100.6 range and finished the week with an upward bias, showing that capital continued to favor the greenback whenever tensions escalated. A brief midweek rebound in risk assets appeared on hopes of de-escalation, but that move quickly faded after tougher signals from the White House pushed markets back into defensive mode.

💼 U.S. data also reinforced the move. ADP, retail sales, ISM manufacturing, and especially March nonfarm payrolls at 178,000, far above expectations, showed that the U.S. economy remains resilient enough for the Fed to keep rates higher for longer.

💴 Among the major pairs, USD/JPY stayed in focus as it swung around the 159–160.5 zone, where traders balanced broad dollar strength against the risk of Japanese intervention. EUR/USD and GBP/USD remained capped by firm dollar demand, while the Canadian dollar proved more resilient than its peers thanks to support from higher oil prices.

⚠️ Moving into April, the main driver for forex is still likely to be the Middle East rather than short-term technical patterns. If tensions ease quickly, the dollar could lose some of its safe-haven momentum. If the conflict drags on and oil stays elevated, USD strength and high volatility are likely to remain the dominant theme.

#ForexInsights#MacroMarkets

Consumer megadeals surged back in Q1/2026, signaling a new restructuring cycle across the sector

🧩 Q1/2026 saw a rare return of megadeals in consumer markets, with McCormick announcing its nearly $45 billion acquisition of Unilever’s food business and Sysco agreeing to spend $29 billion to buy Jetro Restaurant Depot. It was the first time since 2015 that two U.S. consumer deals entered the global top 10 in the same quarter.

📦 What stands out is that these deals emerged while global M&A volume climbed to around $1.3 trillion, up nearly 20% year over year, even as most capital continued flowing into AI, technology, and energy. The consumer sector’s return to the top tier suggests companies are actively pursuing growth through consolidation.

📉 After a period of high inflation, sluggish volume growth, and faster shifts in consumer preferences, scale and portfolio diversification are becoming more important than before. This trend is no longer limited to food, but is also spreading into spirits, beauty, and personal care.

⚖️ Even so, the renewed momentum still faces risks from antitrust scrutiny, tariffs, and geopolitical volatility. If interest rates stabilize further, the consolidation wave across consumer industries is likely to continue in the coming quarters.

#MarketInsights#ConsumerStocks

Global Metals Market Overview for the Week of March 29–April 4, 2026

🔹 The metals market this week was still driven mainly by two major forces: rising tensions in the Middle East and the new U.S. trade measures, rather than by a broad-based growth story. Risks around Iran and the Strait of Hormuz kept energy prices volatile, which in turn revived inflation concerns and pushed capital to swing quickly between defensive positioning and risk-taking.

⚙️ Within base metals, aluminum stood out as the clearest outperformer because it reacted directly to supply disruptions in the Middle East. With major regional capacity affected, the physical market tightened further, backwardation stayed wide, and aluminum continued to lead the broader base-metals complex.

📌 Copper managed to rebound from its late-March lows, but upside remained limited by elevated LME inventories and continued stock pressure on SHFE. That suggests the market is not yet facing a true short-term supply shortage, so each recovery leg is still vulnerable to selling at higher levels.

✨ Precious metals continued to reflect the market’s unstable sentiment. Gold and silver rallied strongly in the middle of the week on safe-haven demand and a temporary easing in geopolitical stress, but the move was not fully sustained as high oil prices, a firm U.S. dollar, and lingering rate concerns continued to cap momentum.

🧭 On the other side, iron ore and steel pointed to a more cautious picture from China, as mill margins remained under pressure, pre-holiday restocking had largely been completed, and port inventories stayed high. Going into the new week, market direction will likely remain tied to the April 6 implementation of the new U.S. tariffs, developments around Iran and Hormuz, and the pace of physical demand recovery in China after the holiday.

#MetalsMarket#GlobalCommodities

The U.S. removes sanctions on former Russian banker Mikhail Zadornov, but the move does not signal a broader shift in Washington’s policy toward Moscow

📌 The U.S. has removed Mikhail Zadornov from OFAC’s SDN sanctions list in its April 3 update, marking a notable development that appears more personal in nature than a sign of broad policy easing.

🏦 Zadornov previously held several important financial roles in Russia, including former finance minister, head of VTB24, and later CEO of Otkritie Bank before stepping away from executive duties in 2022.

🧭 According to the official information, the delisting was approved through OFAC’s standard petition process, while U.S. officials also stressed that this should not be seen as a meaningful softening of Washington’s overall stance on Russia.

⚖️ The case suggests that U.S. sanctions policy still retains some flexibility on an individual basis, especially for figures who no longer hold strategic positions, while the core restrictions on Russia’s banking, energy, and technology sectors remain largely intact.

🌍 The direct market impact on Russia is therefore likely limited, but the move may still offer a mild signal that selected Russian-related cases could continue to be reviewed individually in the months ahead.

#Sanctions#Geopolitics

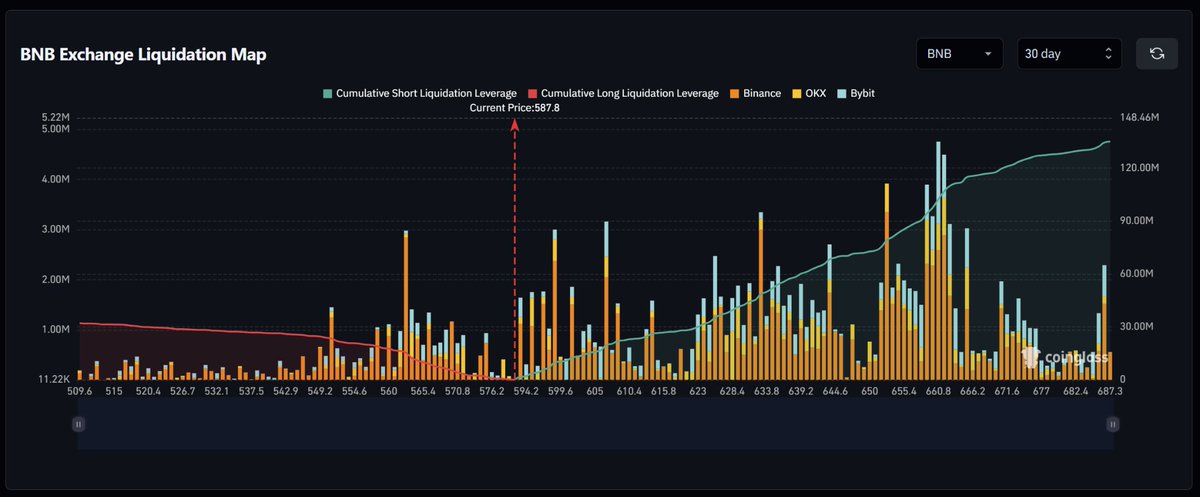

📊 $BNB – Liquidation Map (30 days) – Index ~587.8

🔎 Quick read

• Long liquidation clusters below remain notable at 576.2–570.8 → 565.4–554.6, with a deeper layer at 549.2–537.5.

• Short liquidation clusters above are heavier at 594.2–610.4 → 628.4–644.6 → 650.0–660.8, with a farther zone at 671.6–687.3.

• The area near price looks relatively thin around 587.8–594.2, so once price leaves the pivot, it could move quickly toward the next liquidity cluster.

🧭 Higher-probability path

• If $BNB holds 582.0–587.8 and reclaims 594.2–599.6, the short-term structure still favors an upside push to test the 605.0–610.4 short-liq cluster first.

• If that cluster gets absorbed cleanly, the short squeeze could extend toward 628.4–644.6, with 650.0–660.8 as the next expansion zone.

🔁 Alternate path

• If price loses 582.0, downside attraction could pull $BNB back into 576.2–570.8; if that breaks as well, then 565.4–554.6 becomes the deeper long-liq zone to watch.

• That path would shift the short-term structure toward a downside liquidity sweep before a new balance is found.

📌 Navigation levels

• Pivot: 582.0–587.8

• Bullish confirmation: 594.2–599.6

• Reaction support: 576.2–570.8

• Near resistance: 605.0–610.4 (next 628.4–644.6)

⚠️ Risk notes

• Break/pullback setups around the pivot are preferable with tight risk control, since the liquidity layer near price is fairly thin.

• If price breaks above 610.4, trailing the move makes sense because more short-liq remains overhead; on the other hand, a drop back below 582.0 would weaken the short-term bullish bias clearly.

#TradingSetup#CryptoInsights

Global food prices accelerated again in March as the energy shock spilled over into agricultural markets.

🌍 The FAO Food Price Index averaged 128.5 points in March 2026, up 2.4% from the previous month, marking the second straight monthly increase and the highest level since September 2025. This suggests global food inflation pressure is starting to build again after the earlier cooling phase.

⚡ This latest move was driven more by energy and input costs than by a broad supply shortage. Rising Middle East tensions pushed up oil, fertilizer, transport, and biofuel demand, which in turn lifted vegetable oils, sugar, and wheat.

🌾 Vegetable oils rose 5.1%, sugar climbed 7.2%, and wheat gained 4.3%, while rice fell 3.0% amid harvest pressure and weak import demand. Notably, FAO still raised its 2025 global cereal production forecast to a record 3.036 billion tons, showing that overall supply conditions have not truly deteriorated yet.

📌 In the short term, food markets remain highly sensitive to oil prices and developments around the Strait of Hormuz. If fertilizer costs stay elevated for weeks, the bigger risk will shift to the next crop cycle, when farmers may cut planting or switch to less input-intensive crops.

#FoodMarkets#GlobalInflation

US jobs rebounded in March, but not enough to change the Fed story

📈 The March jobs report showed nonfarm payrolls rising by 178,000, well above expectations, while the unemployment rate edged down to 4.3%. Job gains were led by healthcare, construction, and transportation and warehousing, suggesting the labor market is still showing resilience after the previous soft patch.

🧩 Still, the report was not as hot as the headline suggested. Wage growth came in at just 0.2% month over month and 3.5% year over year, labor force participation held at 61.9%, and the number of discouraged workers increased, showing that softer pockets remain beneath the surface of the labor market.

🏦 For markets, the data was solid enough to support the view that the Fed can stay patient on rate cuts. US Treasury yields moved slightly higher, the dollar firmed, and equities will likely show a clearer reaction at the start of next week because US markets were closed for Good Friday.

#MacroInsights#MarketUpdate

Min Aung Hlaing has taken the presidency, but Myanmar still has not moved beyond the shadow of military rule.

🪖 On April 3, Myanmar’s military-aligned parliament elected Min Aung Hlaing as president with 429 out of 584 votes, completing his shift from junta leader to head of state five years after the 2021 coup.

🏛️ Although it now carries the form of a civilian government, the move is still widely seen as a formalization of military power, as the earlier election was criticized for lacking real competition and the current legislature remains heavily influenced by pro-military forces.

🌐 His departure from the commander-in-chief role, while handing the military to a close loyalist, suggests that the core power structure has barely changed. With the civil war still unresolved and the opposition rejecting the legitimacy of this process, Myanmar is likely to remain a regional flashpoint for instability.

#Myanmar#PoliticalRisk

📊 $DOGE – Liquidation Map (30 days) – Index ~0.092

🔎 Quick read

• Long liquidation clusters below remain notable at 0.0897–0.0887 → 0.0877–0.0867 → 0.0857–0.0847, with a deeper layer at 0.0837–0.0827.

• Short liquidation clusters above are heavier at 0.0933–0.0953 → 0.0963–0.0993, with a farther zone at 0.1003–0.1043.

• The area near price looks relatively thin around 0.0920–0.0933, so once price leaves the pivot, it could move quickly toward the next liquidity cluster.

🧭 Higher-probability path

• If $DOGE holds 0.0909–0.0920 and reclaims 0.0933–0.0943, the short-term structure still favors an upside push to sweep the 0.0943–0.0953 short-liq cluster first.

• If that cluster gets absorbed cleanly, the short squeeze could extend toward 0.0963–0.0993, with 0.1003–0.1043 as the next expansion zone.

🔁 Alternate path

• If price loses 0.0909, downside attraction could pull $DOGE back into 0.0897–0.0887; if that breaks as well, then 0.0877–0.0867 becomes the deeper long-liq zone to watch.

• That path would shift the short-term structure toward a downside liquidity sweep before a new balance is found.

📌 Navigation levels

• Pivot: 0.0909–0.0920

• Bullish confirmation: 0.0933–0.0943

• Reaction support: 0.0897–0.0887

• Near resistance: 0.0943–0.0953 (next 0.0963–0.0993)

⚠️ Risk notes

• Break/pullback setups around the pivot are preferable with tight risk control, since the liquidity layer near price is fairly thin.

• If price breaks above 0.0953, trailing the move makes sense because more short-liq remains overhead; on the other hand, a drop back below 0.0909 would weaken the short-term bullish bias clearly.

#TradingSetup#CryptoInsights