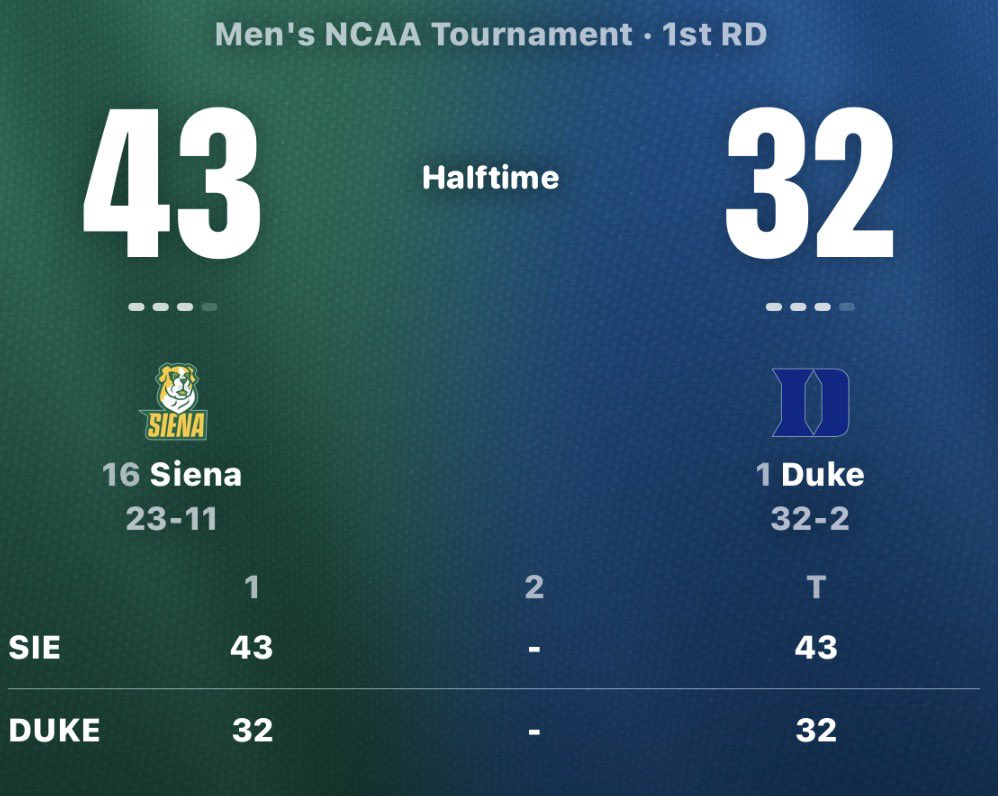

CLTrdr

5.7K posts

BANGGGGGGGG 🚨🚨🚨🚨🚨

Michigan ML ✅✅✅✅✅ 10u

Max Plays move to…..

29-12 lifetime!!

Typed this up with 10 minutes to go!

Congrats to all who tailed!

I. Am. March.

🤝

English

🚨🚨🚨🚨🚨

A Max play has made my card for the Final 4 tonight.

I am 28-12 (70%) lifetime in these spots

That alone doesn’t mean it’s a lock, they don’t exist, but pretty damn good

Free Play

Michigan/Arizona Under 157.5 🏀 2u

To grab the Max play ⬇️

smartmoneysports.net

winible.com/smartmoneyspor…

English

CLTrdr ری ٹویٹ کیا

UBS SEES S&P 500 SURGING TO 7,700

UBS remains bullish on U.S. stocks, expecting the S&P 500 to reach 7,300 by mid-2026 and 7,700 by year-end.

The bank says the rally is supported by strong earnings growth, expected Fed rate cuts, and continued AI-driven gains. It forecasts 11% profit growth in 2026.

Geopolitical risks are seen as temporary, with UBS expecting energy markets to stabilize. While prolonged disruption could weigh on stocks, history suggests markets typically rebound after such events.

Despite recent volatility, UBS believes the overall outlook for equities remains positive.

English

CLTrdr ری ٹویٹ کیا

THE GUY WHO POSTED THIS NEVER MISSES

CHART SAYS IT ALL 🚀

English

@ZachGelb @TheFieldOf68 It's been like this for years now, 0 bulldog mentality. Go up 10, give up a 10-0 run. It's 100% coaching

English

UNC Legend Tyler Hansbrough wasn’t stunned whatsoever that UNC blew a 19-point lead to VCU.

(@TheFieldOf68)

English

@SMSports34 As a UNC guy, I'd give my left nut for Duke to lose this game

English

CAPTAIN AARON JUDGE LEADS TEAM USA ONTO THE FIELD WITH AN AMERICAN FLAG BEFORE THE WBC CHAMPIONSHIP GAME.

🇺🇸🇺🇸🇺🇸

CHILLS.

English

Wait till he realizes it's last year's data.....Cooper Flagg???

A guy in my fantasy league did this for our draft and it pulled 2024 days without him realizing it, took Rashaad White 4th round LOL

Joe Kunkle@OptionsHawk

I mean, pretty nuts, created this Matchup Analyzer in 5 minutes

English

🚨#BREAKING: Pentagon officials are now actively exploring the purchase of Ukrainian-made air defense interceptors as the U.S. looks to strengthen defenses against the growing threat posed by Iranian attack drones.

English

🚨#BREAKING: The country of Spain has officially agrees to cooperate with the United States on Iran after president Donald Trump cuts trade.

English

.@StJohnsBBall down 12 with 13 to go. Big East Regular Season Crown on the line. NCAA seeding on the line. What gives ?

English

@StJohnsBBall SENIOR NIGHT AND YALL GET WHOOPED AS A 17 PT FAVORITE LMAO

English

Congrats to our Seniors!!

Thank you for your dedication to this program. This is a special group! Excited to see what the future holds for these Johnnies! ❤️⚡️

English

CLTrdr ری ٹویٹ کیا

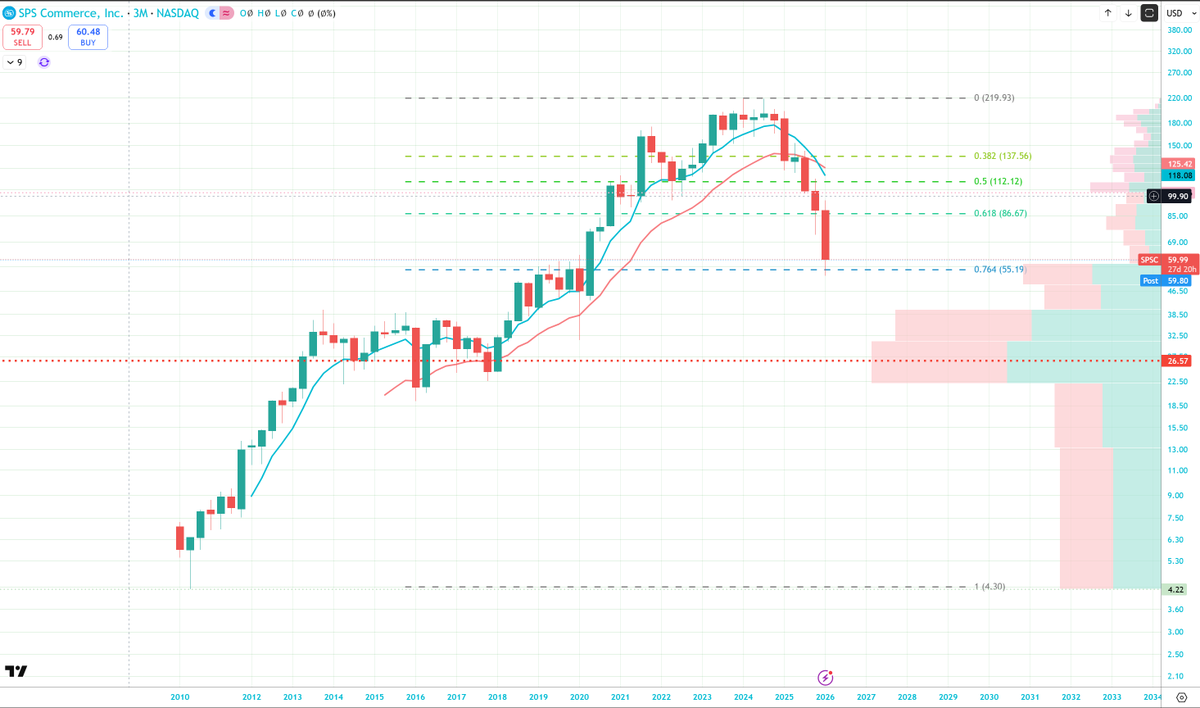

I'll do this one public...always liked this Co. and is wildly cheap at these levels...

Unusual Call Spread in High Quality Software Player at Record Cheap Valuation with Limited AI Disruption Risk

SPS Commerce $SPSC with an interesting trade of 3/3 as 1000 July $80/$105 call spreads bought to open for $2.40 offering a nice risk/reward. SPSC also has 1000 July $105/$135 call spreads bought in open interest so the 3/3 trade may be adjusting the long call leg lower for a higher Delta. There are also 350 short July $80 puts in open interest. SPSC was a major small cap winner from 2010 to 2024 but shares have dipped to $60 from $220 highs though retesting a key 2020 breakout and value shelf this quarter. The timing of the unusual options trade comes after recent reports that activist Irenic Capital is pushing the company to explore a sale. Irenic thinks SPSC is a high‑quality, under‑levered, slower‑but‑steady grower that would command a premium multiple in private equity or under a larger strategic buyer.

SPS Commerce is a vertical SaaS “network” business for retail supply chains, with most of its value in a sticky, high‑margin recurring revenue base rather than one‑off licenses. It operates a cloud platform that connects retailers, grocers, distributors, suppliers, 3PLs and marketplaces and automates EDI and related data flows such as orders, ASNs, invoices, inventory and item data so trading partners don’t have to build and maintain their own point‑to‑point integrations. The business is built around three main solutions: Fulfillment (full‑service EDI and order management), Assortment (item and content data syndication), and Analytics/revenue‑recovery tools (enhanced by the Carbon6 acquisition), all sold on a subscription basis to over 54,000 recurring‑revenue customers globally, with SPS acting as the outsourced integration and compliance team.

SPSC sits at the intersection of retail tech and supply‑chain integration at a time when omnichannel complexity continues to rise even as top‑line retail growth slows. Retailers and brands are juggling stores, e‑commerce, marketplaces, dropship, and DTC, which dramatically increases the number of trading partners and document types. SPS’s network model lets each party connect once and exchange standardized EDI and item/inventory data with all other partners, which is hard for smaller players to replicate in‑house.

SPSC has a market cap of $2.24B and screens extremely cheap at these levels, 11.8X Earnings, 2.6X EV/Sales and 14.75X FCF while consensus sees 6-8% annual topline growth through FY28 with double-digit EBIT growth annually. SPSC valuation is at the cheapest in its history despite all efficiency/operational metrics at or near record highs such a margins and ROTC. SPSC’s model is highly recurring and efficient: about 54,600 recurring‑revenue customers, rising ARPU (~14,350 dollars in 2025), and 100 consecutive quarters of revenue growth. SPSC runs with minimal or no debt, throws off robust operating cash flow, and has been returning capital via buybacks. On the product side, SPS continues to invest in analytics, item data/Assortment, and revenue‑recovery/chargeback tools. Management is also focused on expanding internationally and growing 1P retailer and 3P marketplace integrations.

SPSC’s core business is structurally harder for Claude‑style tools to displace than generic horizontal SaaS, and the company is already embedding AI into its own platform. SPS Commerce sits in a different place in the stack. Its value isn’t primarily the code; it’s the network with 300,000‑plus trading connections, deeply standardized EDI/item data, and managed compliance with thousands of idiosyncratic retailer requirements. AI won’t easily replace the decades of mappings, trading‑partner contracts, service teams, and exception‑handling SPS has built. SPS is selling a managed network, rich domain expertise, and now AI‑enhanced workflows built on top of proprietary, high‑quality data, not just a generic app that can be cloned by a prototype. Over time, if SPS keeps executing on MAX and similar features, AI is more likely to expand its margin and stickiness than to obviate the need for its platform.

English

@SMSports34 Haha no sry that was me acting like a pink haired liberal sissy bag like those who would get upset at a post like this. Not I sir!

English