Peter Phan ری ٹویٹ کیا

3rd poster choice for those who want to immortalize the fight against the AirAsia Karen.

Made with ChatGPT Image 2.0.

Stella Chen@stellachenyl

Here's another poster choice. ChatGPT Image 2.0

English

Peter Phan

2.9K posts

@peterphan88

Investment Manager at Castlereagh Equity. Life Sciences and Technology. Always Learning.

Here's another poster choice. ChatGPT Image 2.0

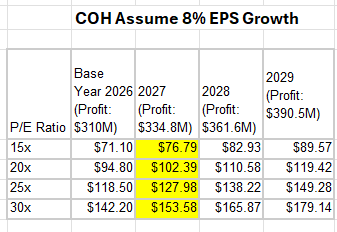

Consider the margin compression. Right now, 50% of new revenue is NON-SEAT BASED Great, right? Except, cost of good sold grew 44% while revenue grew 22% Subs gross margins contracted 360 basis point y-o-y

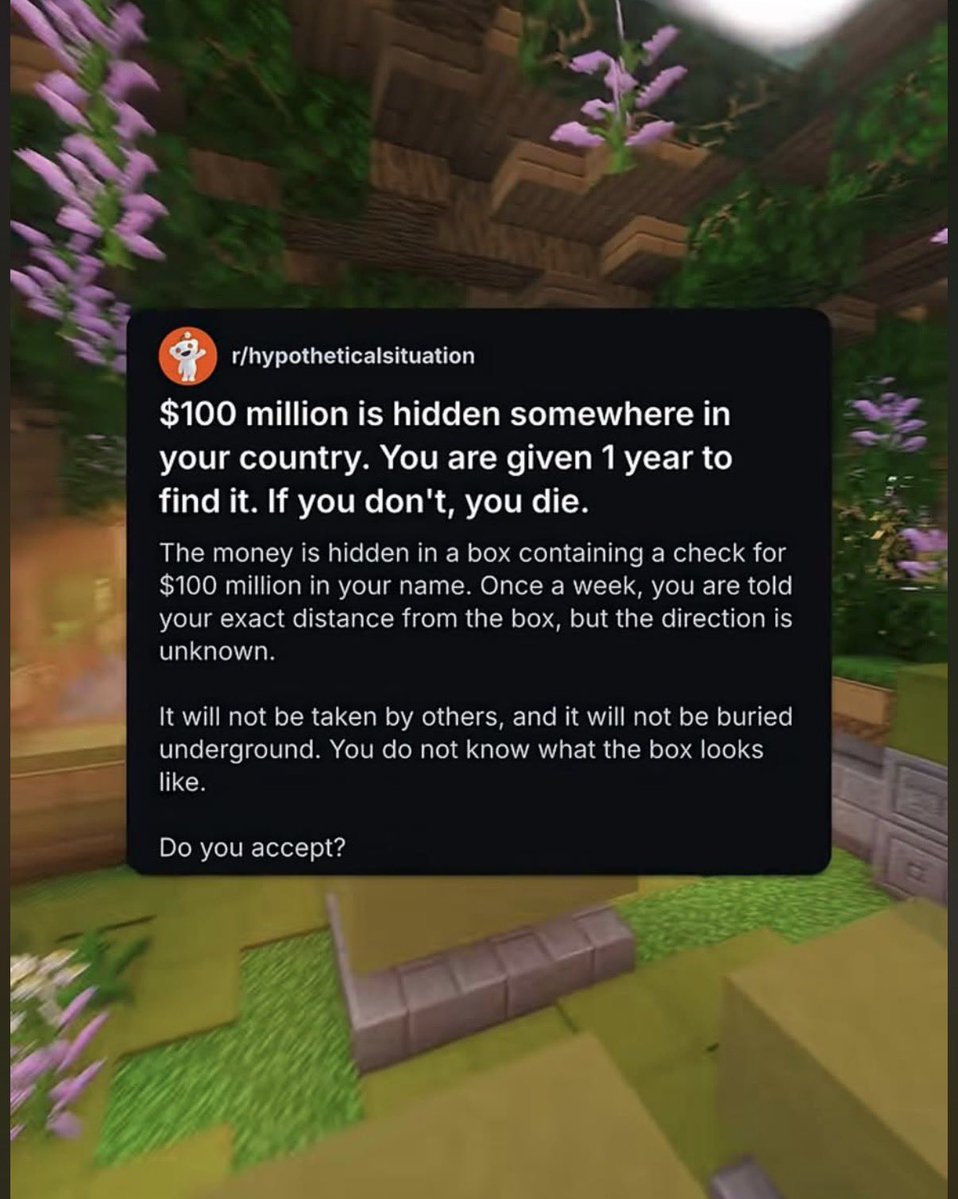

I wrote a quick article on why you should TAKE THIS BET! Here's a visual indication. It would only take a few weeks to find the box to within a few meters, even in a country as big as Russia! I explain this all in the article. Link below.

Absolutely not????