Read about concave and convex worldviews from @VitalikButerin's blogs and found it interesting enough to share it here.

So the idea is, Centralization is convex, decentralization is concave.

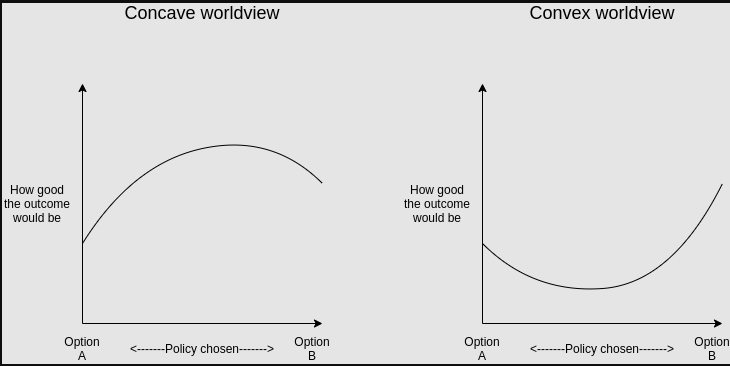

One way to categorize decisions that need to be made is to look at whether they are convex or concave. In a choice between A and B, we would first look not at the question of A vs B itself, but instead at a higher-order question: would you rather take a compromise between A and B or a coin flip? In expected utility terms, we can express this distinction using a graph (the attached image).

If a decision is concave, we would prefer a compromise, and if it's convex, we would prefer a coin flip. Often, we can answer the higher-order question of whether a compromise or a coin flip is better much more easily than we can answer the first-order question of A vs B itself.

Examples of convex decisions include:

- Pandemic response: a 100% travel ban may work at keeping a virus out, a 0% travel ban won't stop viruses but at least doesn't inconvenience people, but a 50% or 90% travel ban is the worst of both worlds.

- Military strategy: attacking on front A may make sense, attacking on front B may make sense, but splitting your army in half and attacking at both just means the enemy can easily deal with the two halves one by one

- Technology choices in crypto protocols: using technology A may make sense, using technology B may make sense, but some hybrid between the two often just leads to needless complexity and even adds risks of the two interfering with each other.

Examples of concave decisions include:

- Judicial decisions: an average between two independently chosen judgements is probably more likely to be fair, and less likely to be completely ridiculous, than a random choice of one of the two judgements.

- Public goods funding: usually, giving $X to each of two promising projects is more effective than giving $2X to one and nothing to the other. Having any money at all gives a much bigger boost to a project's ability to achieve its mission than going from $X to $2X does.

- Tax rates: because of quadratic deadweight loss mechanics, a tax rate of X% is often only a quarter as harmful as a tax rate of 2X%, and at the same time more than half as good at raising revenue. Hence, moderate taxes are better than a coin flip between low/no taxes and high taxes.

When decisions are convex, decentralizing the process of making that decision can easily lead to confusion and low-quality compromises. When decisions are concave, on the other hand, relying on the wisdom of the crowds can give better answers.

English