@gabcasla Ok, thanks — I assumed that price because it seemed to be the one implicitly coming out of the model.

English

Deep Capital

112 posts

@DeepCapital_

Sobre bolsa y mercados financieros

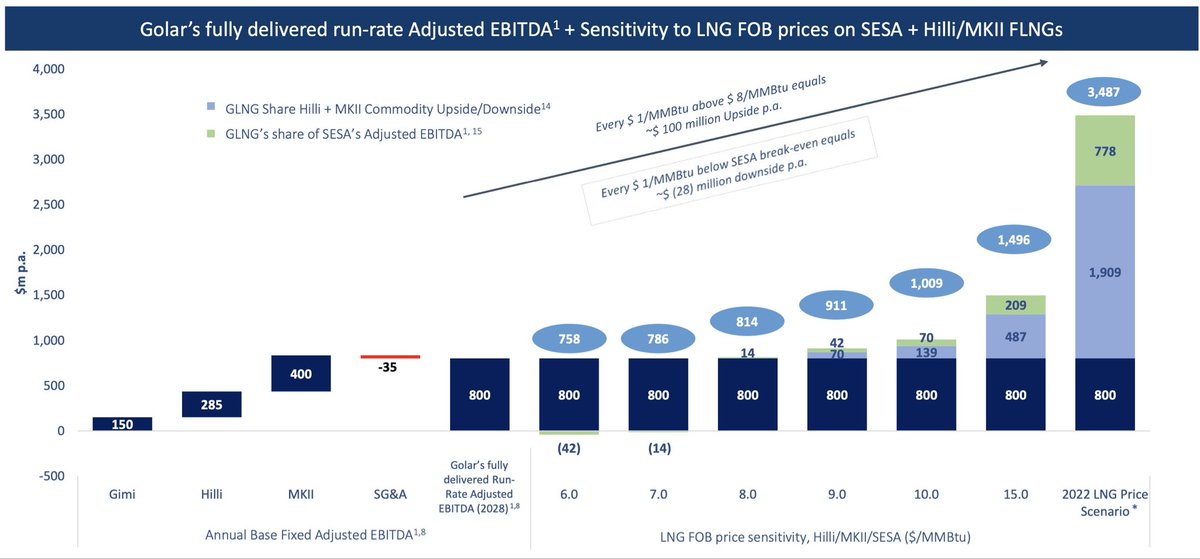

⛵️ Golar LNG - Full analysis post 🇦🇷deal ✅Analysis of the company I’ve spent the most time on over the past 5 years, including full details of the transformative deal announced this Friday. 💎Downloadable spreadsheet with the full Sesa business case (10% $GLNG owned) + DCF valuation model for Golar LNG across all potencial scenarios (TTF/JKM, shipping, eur/usd, Mark II B, CPI,…) 🧐Breakdown of key variables & assumptions — after a full weekend digging into what’s often left out or not so obvious