Jebaim@Jebaim3

Looks amazing, right?

Before you bite the FOMO and buy stocks which ran over 200% in a few months, check the following:

$AVGO Carries ~$70B in net debt from the VMware acquisition — robust FCF covers it, but AI custom silicon slowdown would expose leverage.

$CSCO Splunk acquisition added ~$22B in debt, and hardware revenue is in secular decline as the SaaS transition is still unproven at scale.

$MRVL Still posting GAAP losses; Celestial AI + XConn deals diluted shares by ~27M and spent $1B cash before revenue materialises in FY2028.

$APH Rapid M&A pace (CommScope CCS, Trexon) creates integration execution risk and may pressure near-term margins despite AI tailwinds.

$GLW $7B in long-term debt; stock up ~48% YTD on AI fiber euphoria — valuation now prices in a sustained supercycle with no room for disappointment.

$KEYS Emerging from a multi-year revenue downcycle; Q1 FY2026 blowout was strong but recovery across all end markets is not yet confirmed as durable.

$FN Heavy customer concentration in optical clients ties revenue tightly to the transceiver capex cycle; Thailand manufacturing adds FX and geopolitical risk.

$BESI Reports recently surfaced that leading AI chip makers are reconsidering hybrid bonding timelines — sent the stock sharply lower and creates near-term demand uncertainty.

$POET Raised $150M through a January 2026 equity offering (heavy dilution) to fund development — still near-zero revenue with production readiness not expected until end of 2026.

$LWLG Zero commercial revenue and operations funded by repeated share sales — polymer modulator tech has been "almost there" for years with no product shipments.

$AAOI Dramatically rerated — now guiding $1B+ revenue in 2026 after 82% growth, but historically near-zero profitability, and demand reportedly outpaces production capacity through mid-2027, creating execution risk.

$MXL Revenue collapsed ~60% from its 2022 peak on inventory correction; recovery is happening but margins remain well below prior levels and customer concentration persists.

$SIVE Very small cap with minimal operating history and revenue — essentially a pure speculative bet on CW DFB laser exposure.

$AEHR Revenue is highly lumpy and dependent on a narrow customer base and single product-cycle driver — currently in a trough between adoption waves.

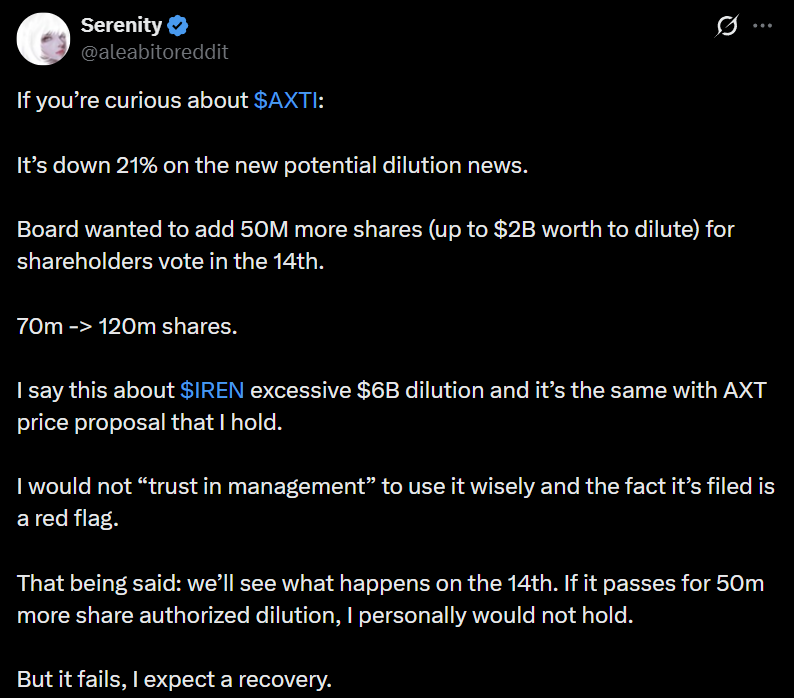

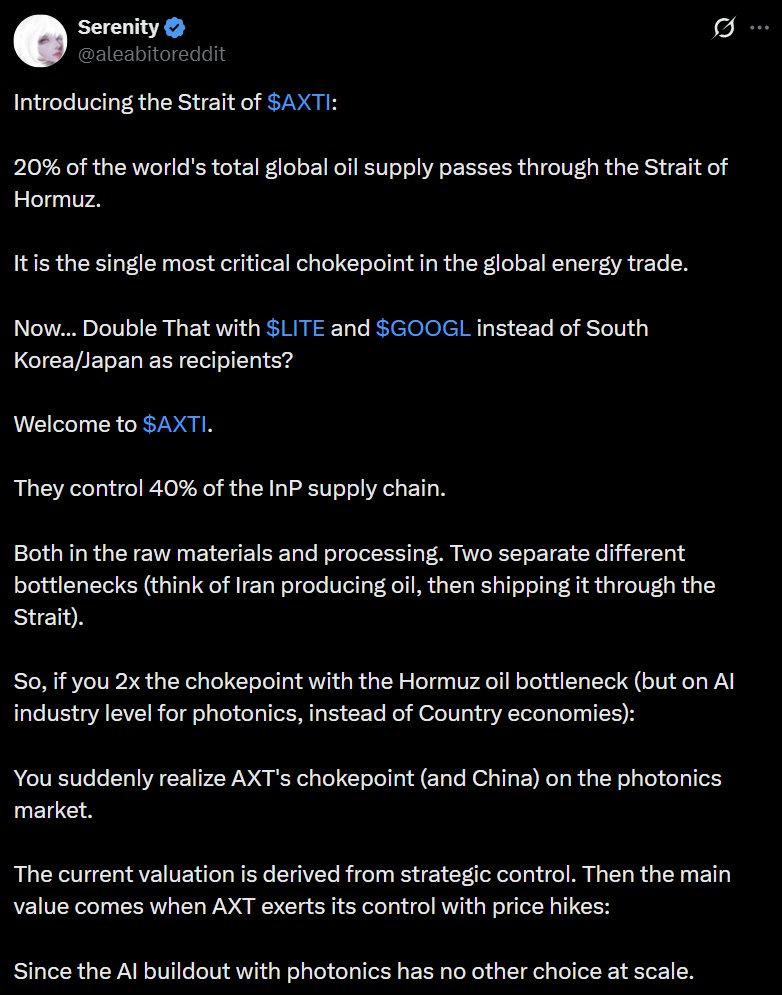

$AXTI Long history of operating losses and erratic cash flows despite being a legitimate compound substrate supplier — the optics boom helps, but execution consistency is absent.

The vast majority of companies mentioned have absolutely horrible finances, future dilution, debts.

On top of that add a very complex business models to understand and comfortably navigate.

Lastly, add cyclicality and momentum traders in today's world.

This is claude sponsored research done in 2 minutes, and you can protect yourself against losses with a bit of research.

Of course many of these have a very attractive reward, but equal or even bigger risk ratio too.

Going all in into a risky play usually turns out to be a very bad decision.

Please be responsible with your own cash. No one will come to help you when you see your stock down -50%.