LevelQue

2.1K posts

Never understood why DTB withholds profits and gives a very low ROE. Not worth

Market Cap Trainers@NSE_Investors

Will DTB management get us sh 10 per share?

English

No matter how much you work and earn at any job, the moment you stop working, you stop earning.

If you want to be wealthy and for multiple generations, then start your own business.

The weekend is a great time to think through ideas of side hustles, or upscale your business.

English

@ThomasJosephat3 Wapi Hiyo Kaka, nitembee, Mahindi Bei ya Ngapi Kwa sasa

Filipino

Sacco returns, KPLC dividends, coupon payments, these are some of the passive incomes you can register in the month of March. Whether it's 2K, the secret is to start the process and the same grows.

Don't be content with one income.

English

@JohnHiuhu Changamoto ni kwamba, You can't put all your investments in Equity

English

Your Sacco gives 9% returns yearly. Equity is giving 7% dividends. In 10 years, the Sacco deposits will have the same value. The share price will have tripled. But mnataka Coupons za 12%.

English

Gloss Clear PPF on Range Rover.

Why PPF?

1. Protect the original paint from scratches and chips

2. Enhance paint appearance without changing the original colour

3.Maintain resale value by keeping the paint pristine.

4. Avoid cost of repainting and touch ups over time

English

Cut rent to Sh 3,000 max, pay yourself first, track every expense, avoid high interest debt, and invest consistently. Start small, stay disciplined, and watch your money work for you.

Abojani Investment 🇰🇪🇺🇬🇹🇿@TheAbojani

Help a bro....

English

@BoardLotSultan @MworiaJ Not sure whether these guy still earns those bonus on performance.

English

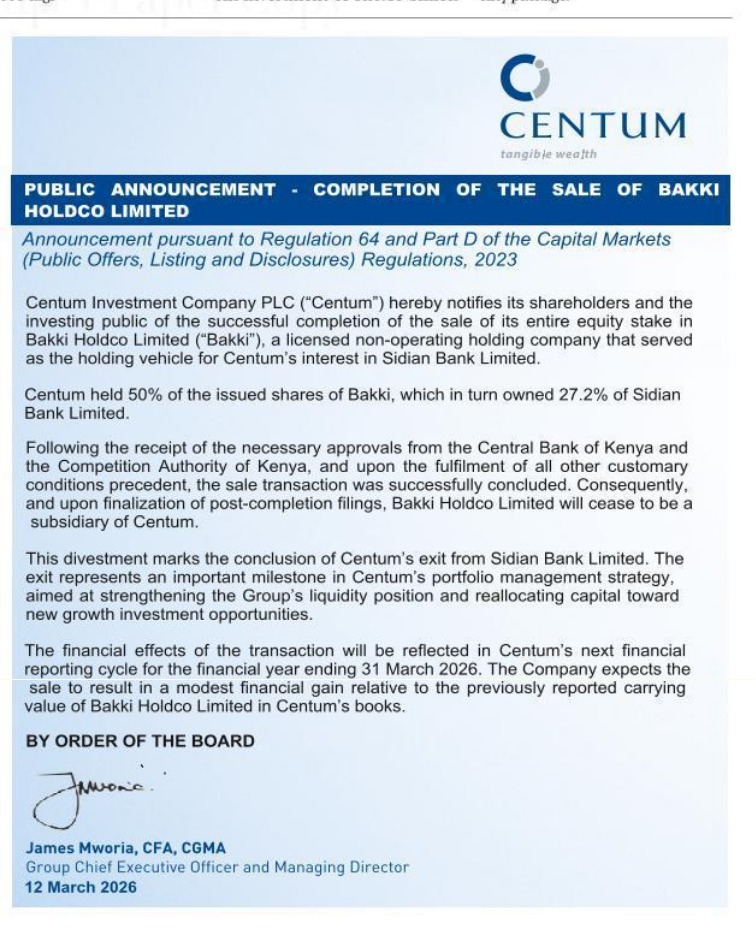

.@MworiaJ mkuu hiyo pesa ya Kuuza Sidian bank, usiweke 2 Rivers. Turudishie special dividends. Tuko payaba sana. Been waiting dividends. Thanks. Yours Shareholders

Filipino

LevelQue 已转推

Ni gani inakufaa sana kwa Business yako?

Tipper Trailer

Flatbed Container Carrier

Fully Enclosed Box Body.

English

LevelQue 已转推

Hii meli watu wa weigh bridge wakaiona Kenya wanaweza chizi

Indonesia

@tonykaromo Even Matatus are hired it's not that the owner drives them.

English

Exactly how will NTSA know which cars have been hired, or if the violator is the owner?

English

If I have a car on bank loan that is still is registered in the name of the bank and I speed on Expressway above the speed limit, who pays the instant fines?

English

Indonesia

@majau_k @Vickyjr @DrKanyuira Did a circuit today too mate. Muranga-Othaya- Nyeri- Nairobi.

Beeautiful country man

English

So leo niliamua kuzurura Nyeri, hahaha! Proper day out. To go is to see came highly recommended by @DrKanyuira

English

LevelQue 已转推

This is the story of how I cleared a 10-year mortgage in 2 years

In the year 2000, I signed for my first mortgage KSh 2.7 million, repayable over ten years, with a monthly installment of about KSh 37,000. At the time, it felt significant but manageable. Like many young professionals, I believed the difficult part was getting approved. Once the bank said yes, I was ready to sit back and relax knowing that in 10 years i will be a home owner.

That is what traps most people.

When many people secure a mortgage, they celebrate the approval rather than confront the obligation. They upgrade furniture, expand their lifestyle, and slowly adjust their expenses until the monthly payment blends into routine existence. Ten years quietly becomes normal. The loan stops feeling temporary and starts feeling permanent.

I had a mentor who refused to let that happen. Stewart Henderson, who was serving as CEO of Old Mutual at the time told me something that permanently changed my understanding of debt: a mortgage is not a commitment it is an emergency.

Then he introduced a rule that, at the time, felt extreme. Every month I earned commissions, I had to bring my statement to him before spending any money. We would sit down together and allocate it.

The bank required KSh 37,000.

Stewart ignored that number.

Instead, he focused on capacity. Whenever income rose, payments rose. Whenever earnings improved, we attacked the loan. He called it 𝐟𝐢𝐧𝐚𝐧𝐜𝐢𝐚𝐥 𝐚𝐠𝐠𝐫𝐞𝐬𝐬𝐢𝐨𝐧, treating debt as something to eliminate quickly rather than manage comfortably.

The first few months were uncomfortable. The natural instinct after earning more money is to reward yourself. Income creates a feeling of entitlement to enjoy what you worked hard for. But discipline does not negotiate with feelings. Every additional shilling was assigned before it reached my pocket.

Something surprising happened. As my income grew, but my lifestyle did not.

Because expenses stayed controlled, every increase in earnings accelerated repayment. The balance started shrinking visibly not yearly, but monthly. What had been structured as a ten-year obligation began to feel temporary.

Two years later, I made the final payment.

Now here’s the surprise, after I serviced the mortgage to completion, my mentor did not congratulate late me. He simply told me to start looking for the next property.

Most people follow a familiar sequence: earn, spend, then save what remains. I learned to earn, allocate, then live on the balance. The house was not paid off by income alone; it was paid off by priority.

Over the years, advising many individuals, I have noticed a consistent pattern. Nearly everyone wants financial freedom eventually, but very few accept financial discipline immediately. The distance between the two is not measured in years it is measured in habits.

Your path does not have to begin with a mortgage. In fact, for many people the smarter starting point is elsewhere, structured savings & investments, or disciplined accumulation strategies that eventually position you for homeownership without pressure.

English

LevelQue 已转推

If you already own a decent home, a small productive farm, and a reliable car, a KSh 24M net worth, strategically allocated across asset classes, can realistically deliver lifelong financial independence. The key is structuring the portfolio to generate stable income, maintain liquidity, and allow for long-term growth.In my case, a practical allocation could be KSh 12M in Infrastructure Bonds (IFBs), generating about KSh 140K in predictable monthly income from low-risk, government-backed fixed income. Another KSh 4M in equities provides exposure to capital appreciation and dividends, while KSh 4M in a Money Market Fund (MMF) serves as a liquidity buffer for emergencies or opportunistic investments.The last 4M into offshore dollar dominated index funds to protect you from local currency fluctuations.

With housing secured( not rent)and a farm reducing living costs(got most foods from your farm) the KSh 140K monthly cash flow alone can comfortably cover basic expenses, effectively making employment optional. At that stage, you transition from working for income to managing capital, with a portfolio designed for stability, flexibility, and long-term wealth compounding.

But hey greed can't let us stop😄.

Unafika hiyo Ksh24M with a possibility of growth but you still want more and more and more!

@cheruiyotkb how do I end greed 😀?

English

LevelQue 已转推

Onyango and Nyaberi receives Ksh 10M.And they utilize them as follows.

Onyango:

1.Buys Ksh6M locally used Toyota LC 200 to get the mheshimiwa vibes.

2.Rents an apartment in Lavington where he pays 300K per month.

3.Gets a "yellow yellow' murima babe and spoils her.Within one year, 4.Onyango goes broke sells the Land cruiser and finally ends up going back to Karachuonyo

On the other hand:

Nyaberi,

1.Thinks long term, knowing that this is a lifetime opportunity to change his life forever.

2.He allocates Ksh7M in T bond that gives him 80K per month.He buys a used fielder or premio for ksh1M .

3.Gets a 30K apartment in middle class neighborhood and pays 6 month rent as he wait for his first coupon payment. 4.Allocates 500K to KCB MMF as an emergency fund

5.He used the remaining cash to develop a skill and start a business. He sets himself for life with almost zero possibility of going broke again.

Conclusion :

Onyango prioritized appearances and consumption, ignoring whether his lifestyle was financially sustainable.

Nyaberi prioritized assets and income generation, ensuring the money could support his lifestyle indefinitely.

The key principle:

A windfall should first be converted into assets that generate income. Lifestyle upgrades should only follow after the income stream is secure.

English