置顶推文

baseflwer

1.9K posts

@baseflwer I honestly don’t understand it that well. But I know an account like ‘Sweep’ has no business writing a whole Citron/Hindenburg-style article about tokenomic structure. Seemed like a paid FUD post

English

wow. would you advise building solutions over funding businesses that already have solutions like you mentioned in this particular case. (engineering student) if i had experience in building a solution for a business/ industry would you advise building it myself or find business with similar solutions and meditate a deal between both parties

English

I FUCKING HATE THE GAME: HOW I THINK ABOUT STRUCTURAL OPPORTUNITIES NOBODY ELSE SEES (PART 1)

I'll probably turn this into some sort of series where I walk through specific opportunities and the math behind them

Not because I'm trying to help you

But because most people miss opportunities that are sitting right in front of them

And maybe someone finds it interesting to see how I actually think about finding these

THE CURRENT REGULATORY SITUATION THAT ENABLES THIS

Let me be specific about what's actually happening right now in the EU

Because most people haven't read the actual directives and don't understand the forcing mechanism

The EU Industrial Emissions Directive was updated in 2023 with new compliance timelines

Not suggested targets

Legally binding emissions reduction requirements with severe financial penalties

The key directives creating this:

EU Emissions Trading System (ETS) - carbon price now €80-100 per ton, projected €150-200 by 2030

Industrial Emissions Directive (IED) - mandates Best Available Techniques (BAT) for all major facilities by 2030

Energy Efficiency Directive - requires 11.7% reduction in energy consumption by 2030

Climate Law - makes 55% emissions reduction by 2030 legally binding

What this actually means in practice:

Every industrial facility over certain emissions thresholds must submit compliance plans by 2025

Those plans must show how they'll meet reduction targets by 2030-2035

If they don't comply, they face penalties of €150-200 per ton CO2 by 2030

Plus they have to buy ETS allowances at market rates which are projected to hit €150-200 per ton

So a cement plant emitting 1 million tons annually faces:

€150-200M in annual penalties if non-compliant

Plus €150-200M in ETS allowance costs even if compliant

Total annual cost of €300-400M if they don't decarbonize

No company can afford to pay that

They're economically forced to spend capital to comply

The regulatory timeline is compressed:

2025: Compliance plans must be submitted

2027: Implementation must begin with measurable progress

2030: First major compliance checkpoint with full penalty enforcement

2035: Final compliance deadline with maximum penalties

Facilities have 5-7 years to deploy solutions

That's not enough time for breakthrough technology to be developed and scaled

They need proven solutions they can deploy now

This creates the forcing mechanism:

Mandatory spending driven by legal requirements not market dynamics

Compressed timelines that eliminate technology risk - only proven solutions work

Severe financial penalties that make the economics of compliance obvious

No escape route - every major facility must comply or face bankruptcy-level costs

The EU created approximately €50-80B in forced capital deployment

Just in industrial heat decarbonization

Over the next 7-10 years

That number comes from basic math:

2,000+ major industrial facilities across EU

Average emissions of 200,000 - 2,000,000 tons CO2 annually per facility

Must reduce by 55% by 2030, 80% by 2035

At current penalty and ETS pricing, non-compliance costs more than facility revenue

The spending is mandatory

The timeline is compressed

The penalties are severe

This is what creates the opportunity

EVERYONE INSTANTLY SUBSCRIBES TO THE BELIEF THAT REGULATION CREATES COSTS

You cannot look at regulatory mandates the way everyone else does and expect to find opportunities they don't see

Everyone instantly subscribes to the belief that regulation reduces returns

But really they are subscribing to more than just that

That means they let the following into their thinking:

Compliance is expensive and drags on profitability

Regulated sectors should be avoided or deprioritized

Government mandates destroy value instead of creating it

Businesses built around regulatory requirements are somehow less legitimate

Industries facing regulatory pressure have worse risk-adjusted returns

Any opportunity in a regulated sector must overcome the "regulation discount"

And probably 50 other assumptions get embedded in their framework that prevent them from seeing what's actually there

When you subscribe to a belief as truth without questioning it

So much comes with that which will hide in your thinking and could steer you away from opportunities for the rest of your career

Not even as a direct result of that belief

But just from what also must be true for that thing to be true

WITH THE EU EMISSIONS DIRECTIVE EXAMPLE

Me not instantly accepting that regulatory compliance is a cost to avoid did not come from arrogance

It came from honest curiosity

So what did I do and what can you do when faced with what is posed as unquestionable consensus by people who've never read the actual regulatory text?

You simply think about it and give some effort

Not coming from a place of trying to disprove that "regulation equals bad returns"

But understanding WHY people think that

How did they come to this conclusion?

Did they actually read the directive?

Did they model the economics of forced compliance spending?

Did they map the timeline and penalty structures?

Or did they just inherit the framework from industry consensus without questioning it?

AN IMPORTANT NOTE HERE

It makes no sense to deploy capital in a way that isn't curated to what you as an individual think creates opportunities

That is what you're doing this for

Not to be contrarian for the sake of it

But to find actual opportunities by only pursuing theses that resonate with your own analysis

Not based on what everyone else is doing

I ACTUALLY READ THE EU INDUSTRIAL EMISSIONS DIRECTIVE

Perhaps I take a look at the actual legislative text and see wow okay so the EU mandated that industrial facilities must reduce emissions by specific percentages by 2030-2035

Not suggested, mandated

With penalty structures of €150-200 per ton CO2 by 2030

Plus ETS allowances at similar prices even for compliant facilities

Well what else goes into the claim that this "creates costs" for investors to avoid?

What forced capital deployment can be identified and measured?

Are we sure regulation is the reason this sector should be avoided?

How much are facilities forced to spend to comply?

How desperate are they for solutions that actually work economically?

How compressed is the timeline and what does that mean for technology risk?

You can have a thesis about where to deploy capital which is in itself more important than following consensus deal flow

That is a fact because no one can tell me what opportunities I should pursue

I get to decide based on my own analysis

Therefore I get to acknowledge that consensus says avoid regulated sectors but continue to pursue opportunities there anyway

You can agree regulation creates complexity but not agree that it aligns with avoiding the sector entirely

Many people get stuck on this

They never think about what actually creates opportunities and why certain frameworks might be wrong

Actually most of the successful PE operators I know do not give this thought

They are like algorithms that deploy capital efficiently but are slaves to consensus

Following the same deal flow everyone else sees

Competing for the same assets at inflated prices

With it comes deployed capital and hopefully returns to raise larger funds

This is not at all what they would say is most important to them if you asked them

They wouldn't say it because people would look at them funny

The industry says strategic value creation, operational excellence, proprietary deal flow are what matter

People would say anyone who admits they just follow consensus and compete on price is unsophisticated

PERSONALLY I THINK THEY LIKE THE FEELING OF DEPLOYING CAPITAL

And the validation from LPs eases the feeling of inadequacy from not having truly differentiated opportunities

They get addicted to the feeling of winning deals and never think about why they like it or what sacrifices are being made

The market is their compass

Deploying capital is them getting closer to building a track record

People can do whatever they want

I cannot tell someone their approach to finding deals is not legitimate

Because it obviously works for many people, it's happening

But I can encourage them to acknowledge a very big problem with logic

And encourage them to place true value onto solving this problem

PROBLEMS ARE OBSTACLES THAT GET IN THE WAY OF FINDING ACTUAL OPPORTUNITIES

The more consistently you identify the same problem as an obstacle the stronger this grows inside your conviction

You start to see this problem everywhere

Everyone competing for consensus deals

Everyone avoiding regulated sectors without questioning why

Everyone following the same playbooks about SMB roll-ups

All the sudden it becomes a complete wall blocking the industry from seeing what's actually there

At this point it turns into your edge

Now your analysis has meaning

You must look where others won't to find opportunities they don't see

You are moving with intention toward non-consensus sectors

You have a vision of where forced capital deployment creates opportunities

You have something to channel your capital into that you deeply believe creates asymmetric returns

You now have a unique lens for evaluating opportunities

Honestly assessing whether something is actually attractive or just consensus

THE EU INDUSTRIAL EMISSIONS DIRECTIVE IS THE PERFECT EXAMPLE

The directive mandated specific emissions reductions by 2030-2035

For a cement plant emitting 1 million tons CO2 annually, penalties are €150-200M per year by 2030

Plus ETS allowances of another €150-200M

Total annual cost of €300-400M if they don't decarbonize

For a paper mill doing 80,000 tons, that's €12-15M in penalties plus €8-10M in ETS costs

They will spend literally anything that costs less than that to avoid these costs

This creates approximately €50-80B in mandatory capital deployment over the next decade

Just in industrial heat decarbonization

That number isn't speculative

It's basic math on facility emissions, penalty structures, and compliance timelines

EVERYONE IN CLIMATE TECH SEES THIS AND BUILDS THE WRONG THING

They look at €50-80B in forced spending and think "we should innovate"

Novel thermal storage materials

Advanced heat pumps

Hydrogen production breakthroughs

They're trying to compete on technology

Hoping for breakthroughs that make their solution win

Wrong game entirely

The timeline doesn't allow for technology development

Facilities must comply by 2030

That's 5-6 years from now

Not enough time to develop, test, and scale new technology

The actual opportunity is recognizing that proven technology already exists

Thermal energy storage has been deployed in concentrated solar plants since the 1980s

Molten salt storage, ceramic thermal batteries, phase-change materials

All proven, all commercial, all ready to deploy today

Nobody's deploying it to this specific mandatory market at scale

THE ACTUAL PROBLEM FACILITIES FACE RIGHT NOW

They have mandatory emissions reductions by 2030-2035

Compliance plans due 2025

Implementation must begin 2027

Current options don't work economically:

Direct electrification requires €20-30M per facility, grid infrastructure that doesn't exist, electricity 40-60% more expensive than gas

Hydrogen conversion requires €25-40M for burner conversion, hydrogen at €8-12/kg versus gas equivalent of €3-4/kg

Neither solution closes economically

But they still must spend money to comply

Timeline is compressed - no time for breakthrough technology

Gun to their head

Forced capital deployment

No legitimate solution at scale

This is where opportunity lives

THERMAL STORAGE SOLVES THIS COMPLETELY WITH PROVEN TECHNOLOGY

Install modular thermal storage at the facility

Charges using grid electricity when it's cheap or free (200+ hours annually in Germany/Scandinavia when wind overproduces)

Discharges stored heat into existing steam systems

No process modifications required

Can be deployed and operational within 12-18 months

The economics for a typical Swedish paper mill:

€8M capital cost for 20 MWh thermal storage

Replaces natural gas worth €60-80 per MWh

Annual value creation: €10-15M

Operating costs: €2-3M

Net annual value: €7-12M

Payback: 3-4 years including EU subsidies covering 30-40% of capital

After payback they save €3-4M annually on energy

Plus avoid €12M annually in penalties

Plus avoid €8-10M annually in ETS allowances

That's €20M+ in annual value from €8M investment

The solution works economically today

And can be deployed within the compressed regulatory timeline

€50-80B IN FORCED SPENDING, FRAGMENTED SUPPLY, NOBODY EXECUTING AT SCALE

This is what everyone misses

Massive mandatory market with compressed timeline, guaranteed demand, proven technology, excellent economics

But the supply side is completely fragmented

200+ small thermal storage suppliers across Europe

Most doing €5-20M annual revenue

Selling to concentrated solar and niche industrial applications

None focused on this specific mandatory market

None building commercial infrastructure to serve industrial facilities at scale

None have the reference customers or installation capacity to serve 2,000+ facilities by 2030

THE CONSOLIDATION THESIS IS OBVIOUS

Market size: €50-80B mandatory deployment over 7-10 years

Timeline: Compressed to 2030-2035, facilities must deploy now

Market structure: Highly fragmented, 200+ small suppliers

Regulatory catalyst: Severe penalties plus ETS costs create guaranteed demand

Technology proven: Zero R&D risk, can deploy immediately

Customer urgency: Must comply by 2030, running out of time

Current solutions inadequate: Creates massive opportunity for thermal storage

Consolidation benefits: Scale in procurement (30-40% cheaper components), installation capacity (50+ projects annually vs 5-10 for independents), reference customers, multi-site contracts, ability to meet compressed timelines

After consolidating 15-20 suppliers you have structural advantages small players cannot match

They lack the installation capacity to serve customers on compressed timelines

They lack the references to win large contracts

They lack the scale to handle 50+ simultaneous projects

They lack the procurement advantages to match pricing

THE MATH ON BUILDING THIS

Years 1-2: Acquire 3-4 suppliers for €30-50M, get to €40-60M revenue, execute first 10-15 installations by end of 2026

Years 3-4: Acquire 8-10 more suppliers for €80-120M, scale to €200-250M revenue, expand to cement and steel, have 40-50 reference installations by 2028

Years 5-7: Selective bolt-ons plus massive organic growth as regulatory deadline approaches, scale to €800M-1.2B revenue, exit at 12-15x EBITDA

Total capital: €400-500M

Exit value: €3-5B

MOIC: 6-10x

This is how it works when you find forced capital deployment with compressed timelines before it's consensus

WHY THIS ISN'T CONSENSUS YET

Most PE firms don't do regulatory analysis to find sectors

They look at market reports about software and healthcare

They follow banker deal flow showing consensus opportunities

They inherited the framework that regulation equals bad returns

They're not reading the actual EU directives to understand penalty structures and compliance timelines

So opportunities like this sit there

Perfect PE characteristics but nobody's building the thesis

Because it requires work most people won't do

Reading 300 pages of legislative text

Modeling facility-level compliance economics

Understanding penalty structures and ETS pricing

Mapping compliance timelines and technology deployment windows

THE SMB MARKETPLACE CONTENT CREATORS COMPLETELY MISS THIS

You see them posting frameworks about boring businesses

HVAC roll-ups, landscaping consolidation, plumbing aggregation

"The 7-step framework for evaluating SMB acquisitions"

"Why boring businesses generate the best returns"

They're pattern matching to what worked for someone else

Optimizing tactics for competing in consensus sectors

How to find sellers better, negotiate better, finance better

Meanwhile €50-80B in mandatory spending with compressed timelines sits in a sector they'll never look at

Because it doesn't fit their framework

And it requires reading regulatory documents instead of following playbooks

They're too busy posting about loving the process to read the actual directives

BEHIND EVERY AVOIDED SECTOR THERE IS AN OPPORTUNITY

Behind every opportunity you can find asymmetric returns

But if everyone says regulated sectors have worse returns

That can be true for most people but not align with what I've found

My analysis shows regulatory mandates with compressed timelines create forced spending in fragmented markets

First mover who consolidates captures the sector before it's consensus

Most people won't do the regulatory analysis work required

Which means opportunities are available to those who will

THE ACTUAL SCALE OF WHAT THE EU CREATED

Industrial heat: 20% of EU carbon emissions, roughly 800M tons CO2 annually

Must reduce by 55% by 2030, 80% by 2035

At €150-200 per ton penalties plus €150-200 ETS allowances, non-compliance costs €240-320B annually by 2030

No company can afford that

They're economically forced to spend capital

€50-80B required just for thermal decarbonization

2,000+ industrial facilities that must deploy solutions by 2030:

Paper and pulp: 500+ facilities

Cement: 200+ plants

Steel: 150+ facilities

Chemicals: 400+ plants

Glass: 300+ facilities

Food processing: 450+ facilities

Each facing mandatory reductions with compressed timelines, inadequate current solutions, severe financial consequences

This isn't speculative

This is counting actual facilities with actual emissions facing actual penalties on actual timelines

The spending will happen between now and 2030

DIFFERENT WAYS TO CAPTURE THIS DEPENDING ON YOUR SITUATION

€300-500M in PE capital: Full pan-European roll-up, consolidate 15-20 suppliers, exit for €3-5B

€50-100M: Regional platform in Scandinavia or Germany, dominate that market, exit for €300-500M

€10-25M: Partner with supplier, build reference base, sell to larger player

Industry relationships but limited capital: Broker between facilities and suppliers, take fees on deals, eventually get acquired or backward integrate

Thermal engineering expertise but no capital: Provide technical diligence for financial players, partner for equity split

You don't need €500M to capture value

You need to understand where value gets created and position accordingly

Multiple entry points depending on what you bring

THIS IS WHAT REGULATORY MANDATES WITH COMPRESSED TIMELINES ACTUALLY CREATE

Not costs to avoid

€50-80B in forced spending to capture over 5-7 years

Severe penalties plus ETS costs making non-compliance impossible

Compressed timeline eliminating technology risk - only proven solutions work

Current solutions don't work so new deployment gets premium pricing

Fragmented supply so consolidation creates structural advantages

Desperate customers because they're running out of time

This is the pattern worth looking for

Not optional spending where you compete on value

Mandatory spending with compressed timelines where you execute better than fragmented alternatives

MOST PEOPLE WILL NEVER SEE THIS

Because they inherited the framework that regulation equals bad returns

They won't read 300 pages of boring directives

They won't model facility-level compliance economics

They won't map penalty structures and timelines

They won't question whether their assumptions are true

So they'll keep competing for consensus deals in unregulated sectors

While €50-80B in forced spending with a 2030 deadline sits there

Waiting for someone willing to do the work

I'LL WRITE ABOUT THE NEXT ONE SOON

There are 5-6 other EU regulatory mandates with similar characteristics

European defense procurement modernization, reshoring infrastructure requirements, grid interconnection mandates, water treatment standards, building energy retrofits

Each one €20-50B in addressable spend with compressed timelines

Same pattern: forced spending, compressed deployment windows, fragmented supply, proven solutions, severe penalties for non-compliance

Different sectors

Same opportunity for whoever reads the actual regulatory text and models the economics

Instead of following consensus frameworks about avoiding regulation

TL;DR

Regulation isn't a cost to avoid

It's forced capital deployment with compressed timelines to capture

The EU emissions directive created €50-80B in mandatory spending that must happen by 2030

Everyone sees it and builds the wrong thing

Or avoids it entirely because "regulation equals bad returns"

Meanwhile the opportunity sits there

Proven technology that can deploy immediately, fragmented suppliers, desperate customers facing 2030 deadline, excellent economics

For whoever questions consensus and does the boring work of reading the actual directives

That's the entire point

Not following playbooks about SMB roll-ups

Reading the actual regulatory documents others won't read

Finding forced capital deployment with compressed timelines

Building consolidation positions before they're consensus

Everything else is just competing for consensus deals at inflated multiples and hoping for the best

English

@moneyfetishist may just be too late- but i’m interested in learning how you learned to eloquently write your thoughts as comprehensive as you’ve done?

English

spent the last few hours answering questions from strangers on the internet while sitting on a plane and the thing that keeps striking me is how similar every question sounds once you strip away the context

the BB analyst making $200K wants to know if his life has meaning. the 20-year-old in a frat wants to know if he is on the right path. the guy running a $15M environmental services company cannot sleep because his leverage ratio scares him even though his covenants are fine. the first-year law student wants someone to tell him the career pivot will work out. the immigrant who got laid off wants to know he is not falling behind permanently

the details are different. the feeling underneath is identical. am I going to be okay

we pretend that money and status and titles fix this. they do not. I sit in rooms with people who control nine-figure portfolios and they are nervous about the same things as everyone else. they just have more expensive language for it. the fund manager calls it "risk management." the analyst calls it "career strategy." the 20-year-old calls it "figuring out my path." same anxiety wearing different suits

I watched a grown man worth more than most people will earn in ten lifetimes throw a tantrum in a conference room because someone questioned his assumption in a model. not his competence. not his track record. an assumption in a spreadsheet. a cell in Excel. he turned red and raised his voice because for 15 seconds he felt like he might be wrong about something and his entire identity could not absorb that possibility

that is not a professional disagreement. that is a kid on a playground who got told he is not the fastest runner

Schopenhauer wrote that humans are not rational beings who occasionally feel emotions. we are emotional beings who occasionally think rationally. the rationality is the exception. the feeling is the baseline. every framework we build in finance and in business and in life is an attempt to impose order on a brain that is fundamentally running on fear and desire and the need to be seen as competent by other people who are also running on fear and desire

the most dangerous version of this is the person who thinks they have outgrown it. the one who believes that enough success or enough money or enough status has made them rational. that person is not more rational. they are less accountable. nobody around them pushes back anymore so the irrational impulses go unchecked and get rebranded as conviction and vision and leadership

the best operators I know are the ones who understand that they are still unreasonable kids underneath everything. they lose their temper over small things. they take criticism personally even when it is constructive. they make emotional decisions and reverse-engineer a logical justification after the fact. the difference is they know they do this. they have systems to catch it. they hire people who are allowed to tell them when they are being stupid. they build in a 24-hour delay before any decision made while angry

the worst operators are the ones who think they have evolved past it. they confuse pattern recognition with wisdom. they confuse wealth with emotional maturity. they confuse the silence of the people around them with agreement when it is actually just fear

Nietzsche said that the most common form of human stupidity is forgetting what one is trying to do. I think the more common form is forgetting what one is. which is a complicated animal that learned to use spreadsheets but never stopped being afraid of the dark

none of us outgrow being unreasonable. the question is whether we build a life that accounts for it or one that pretends it does not exist

thanks for the questions today. you are all going to be fine. even the ones who do not feel like it right now

moneyfetishist@moneyfetishist

bored on a flight. AMA PE, M&A, deal structuring, operational stuff, Mittelstand, AI in boring industries, tax structures that make your accountant nervous, how to not get fcked when selling your company, game theory applied to literally anything, European vs American business culture, why your restaurant is bad, or whatever else you want to know no topic off limits besides to my person. ask

English

@izebel_eth I’m betting aggressively on hyperliquid..i want to allocate all my capital buying up dips instead of getting carried away on alternative assets like LIT. thanks for the reply.

English

@baseflwer all your money in single best idea is absolutely the best way to aggressively grow your portfolio (as long as your right)

i did this 4+ times to come back from blowups

but at current stage am more focused on consistency than aggression tbh, i feel like i graduated a bit

English

its not hyperliquid vs lighter

its hyperliquid and lighter vs the drifts of the world

English

@izebel_eth jez, what happened with put all your money in your single best.. not your second best idea. Why are you approaching the perps trade differently in this regard specifically?

English

i am very specific about the exchanges i support, and i have large positions in each:

1. hyperliquid is the best, and i continue to support them and their ecosystem

2. lighter is #2 with retail advantage + specific tech advantages that i think will let it do spot collat best

3. variationals model is click trading + rfq = not fighting other exchanges for clob liquidity

i fully believe the perp pie will grow enough that i will make money on all three

English

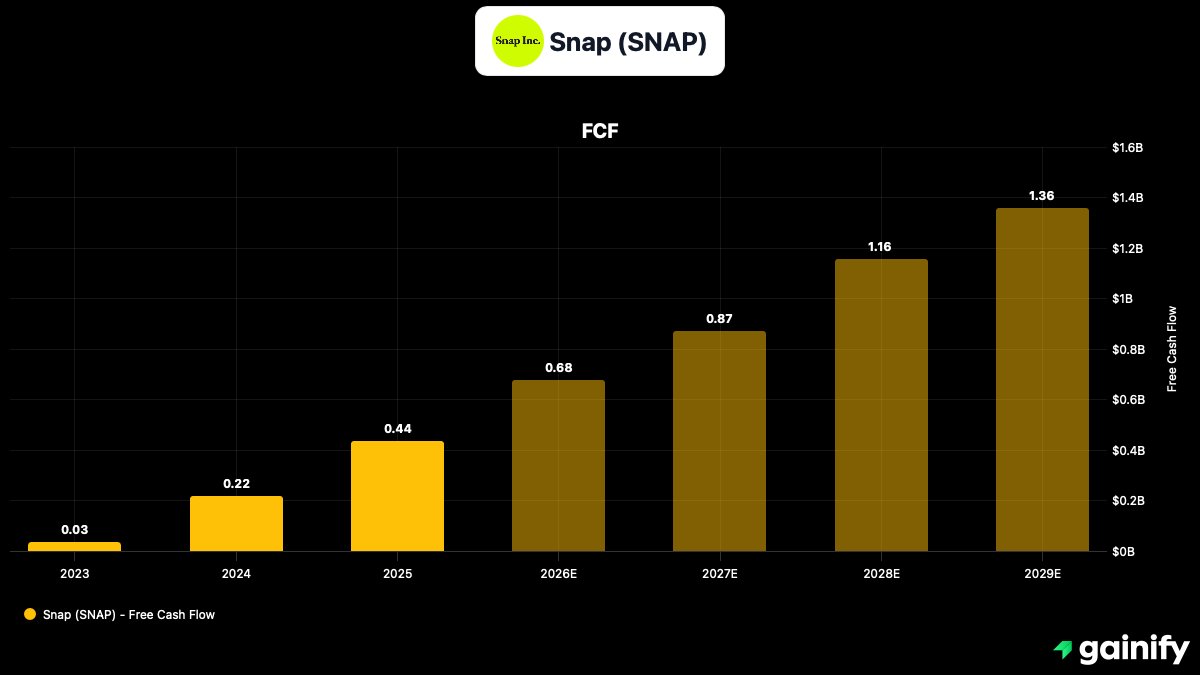

$SNAP is quietly becoming a cash flow machine… and most people still don’t see it.

Free cash flow went from basically nothing

to hundreds of millions in just a couple years.

~$35M in 2023

~$219M in 2024

~$400M+ recently

That’s not normal growth.

That’s a business inflecting.

And it’s not just one good quarter either…

Snap just printed over $200M in FCF in a single quarter.

So what’s happening?

The business is finally showing operating leverage.

Revenue is growing

Margins are improving

Costs are becoming more efficient

Now look at the estimates…

They’re projecting steady growth out over the next few years.

But honestly… those look conservative.

Why?

Because they’re not fully pricing in:

- Snapchat+ scaling

- Improving ad platform + AI targeting

- Stronger international monetization

- Continued operating leverage

Now let’s address the biggest bear case:

Stock-based compensation.

Yes, SBC has been high.

And yes, it creates dilution.

But here’s what matters…

The business is now generating real cash.

That means Snap has flexibility.

As cash flow grows, they can:

- Offset dilution

- Reduce reliance on SBC over time

- Let operating leverage do the heavy lifting

SBC is a concern if the business isn’t improving.

That’s not the case here.

The fundamentals are getting stronger, not weaker.

English

head down.

stay focused.

holding/buying crypto will be by far the hardest decision you'll have to make over the next year or 2.

"Doom and Gloom" propaganda will slowly grow as more people capitulate; saturating the timeline with dark and cynical views and beliefs.

Those same people were optimistic and euphoric at the markets ATH so, don't regard their opinion.

keep your head down.

and grow you positions.

and remember:

"Price goes down at some point no matter the euphoria but, it goes up too, at some point, no matter the fear".

English

Q1

I’ll continue to be SHORT going into the first three months of 2026

my reasons are the BOTH the GOLD and SILVER rallies; to me these are indicators of fear.

These assets are safe haven investments. So, it further demonstrates a fear in the markets.

So, i’ll remain cautious and short.

also with my contrarian view, many market participants are still overly optimistic which is good, but until bullish rallies are met with heavy resistance and pessimism. I’ll remain short.

-baseflwer

baseflwer@baseflwer

i think Q4 will be the final nail in the coffin if Q4 isnt as bullish as many still believe it will be then expect many to be sidelined going into 2026 DCA dips try and catch the runners of each month but we arent risk on imo

English

Bro is everyone short?? I don’t see a single long on my timeline

I mean I get it but…what is this PVE?

English

sometimes trading is far easier than many of us make it out to be.

thats partly why the “nothing ever happens crowd” or the traders who remain patient across many months

outperform.

multiple times every year there are opportunities where it is clearly obvious where prices will be compared to where they are now.

sometimes assets fall so low

far below their lifetime low

that buying at those levels is 70%-80% profitable

all that said I was a $snap buyer.

English

Very fair critique, and I do have the tendency to do the calculations and understand with the end result will look like, while not appreciating the time it takes to achieve it. So, you make a very good point!

With this particular event, I do think that certain leverage areas from Trump’s opposition have either been neutralized or are well on their way to being neutralized. A couple weeks ago I was more pessimistic.

But again, to your point, it may take much more time than I foresee. I wouldn’t be surprised if thats the case. My optimism blinds me at times 😁

English

@ChudCrentis curious how you see a pump here? or you’re just a perma bull

English

I do agree the crypto will find a bottom before equities.

but i do find one thing unique about your perspective.

i find you over estimate the capabilities of trump and underestimate the lengths/capabilities of his enemies and their ambitions.

i believe perhaps for personal reasons…that the market will grind lower because this is just the beginning of many more escalations

from tariffs -> ICE-> regime takeovers-> iran conflict-> cuba?

there’s a lot that needs to be achieved under trumps regime and his enemies will play a significant role in disrupting and destabilizing those things

time will tell but i don’t think sentiment bottoms here.

iran may be resolved soon idk

but it won’t stop there.

English

To be fair it looks awful

But my thoughts are crypto bottoms before equities, and I think equities bottom within the next week or two. So we’d be in that timeframe where crypto would start its very uneasy grind higher

Sentiment is absolutely abysmal, most folks are in the mindset of this war being as drawn out as something like Iraq. I actually think trump is working with Iran since the beginning of this conflict and when they decide to end this conflict it will wrap up way faster and cleaner than most people will imagine.

Zero rate cuts are priced in for ‘26 but Trump/Bessent will never let that happen.

The war has exposed Europe as a weak with an inability to be self-reliant for things like energy and a clearly diminished role in global policy. Investors in European bonds/equities will have capital flight, which will likely end up in US markets/treasuries.

Ukraine war will wrap up very soon, as high oil prices crush Ukraine/Europe but generate massive profits for Russia. US will stop helping Ukraine “to focus on the ME”. So by May you could have a situation where you have no active wars occurring, a NASTY Q1 GDP print behind you and rate cuts back on the table.

BTC could always go to 50k like everyone is predicting but i’d rather be accumulating spot here instead of shorting the hole.

Of course I could be right about the political analysis and wrong about price action — happens a lot. But i think there’s enough of an edge for me here to bet on it

English

@baseflwer Crypto bull run*

Btw stonk bull run will resume once the war is over

English