ELI5 of TLDR

4.6K posts

ELI5 of TLDR

@eli5oftldr

i write about crypto assuming you’re a 5yo with a short attention span / on vacation, brb

加入时间 Mayıs 2022

419 关注16.1K 粉丝

>lure in thousands of fresh normie-MAGA followers with tactically executed boomerslop

>immediately start dripfeeding sympathetic thielian propaganda, rw coopts of critical theory, fantasies of technocapital--

>Vance-Sacks 2028

>Chamath at the Pentagon, Garry Tan at State

>dark abundance, american dynamism, orbital authority

>dyson swarms, starlifting, micro black holes

>biofabrication, telomere extension, wholebrain emulation

>solar sails, seed chips, von neumann probes

are you trusting the plan yet, anon?

English

real defi are eternal, autonomous, credibly neutral, pro bono mechanisms

governance tokens are just transitional stage

English

So Aave Labs changed the router to CoW Swap that is *technically* cheaper than the previous router, Paraswap, but since they decided to include partner fees (which they keep 100% for themselves), the final cost for the user is *actually* higher?

English

i'll explain:

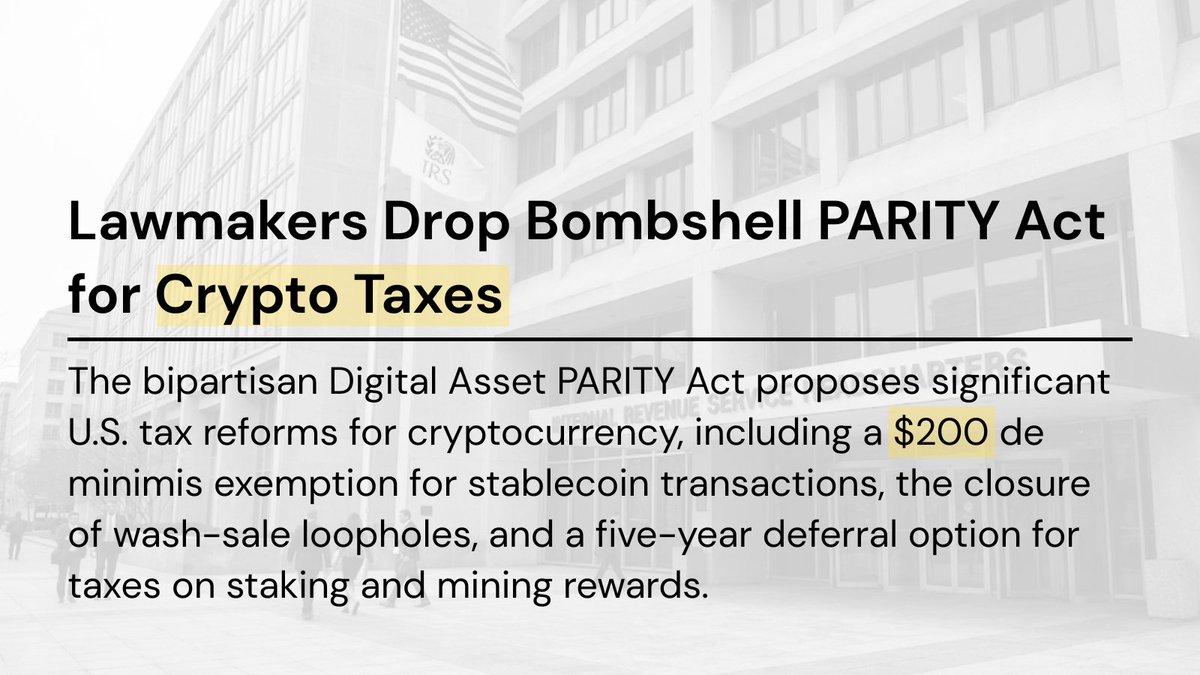

-> parity act $200 tax break only for big regulated stablecoins. but bitcoin & ethereum still fully taxed.

-> wash-sale rules hit traders hard. no more sell low buy back same day for tax tricks. whales lose big edge.

-> staking/mining tax wait 5 years. if price 2x, you pay way more later. i'm sorry stakers.

English

SEC HOSTS DEC 15 ROUNDTABLE ON PRIVACY AND CRYPTO SURVEILLANCE STANDARDS

-> zcash pumped 919% in 2025, and its shielded transactions are now 70% of volume, 30% of supply locked in private pools. eu bans these coins starting july 2027. sec meeting could determine if they survive in regulated markets.

-> tornado cash developers getting convicted on money laundering charges tell us something: privacy tool builders face criminal liability even when they just write code. alexey pertsev got 5+ years in netherlands.

-> hester peirce (sec crypto task force head) moderating, featuring not just zcash but aleo, predicate, espresso, spruceid. so we got the entire privacy ecosystem being "interviewed".

English

i'll explain what it means that blobs burn eth:

-> fusaka (ethereum upgrade that went live recently) adds a 'rule' (eip‑7918) that keeps blob fees from being almost free, so when l2 chains use a lot of blobs, ethereum burns a lot more eth (which makes it deflationary) and earns more fee income.

-> before blobs, one l2 data batch cost 0.032 eth in fees, after blobs the same thing cost 0.000131 eth, which is 247 times cheaper, and average mainnet gas prices fell like 60%.

-> bros from galaxy found that, before blobs, rollups (eth's l2s) burned 15,052 eth over 150 days just by posting data; now a lot of eth burn comes from l2 data and from how this new blob fee market is set.

English

good luck:

-> us debt is ~36–38 trillion in total. interest rates the us pays alone can beat defense spend. yearly deficit is still ~1.8 trillion.

-> musk says ai + robots fix this in 3 years, even if it means “significant deflation” (prices falling fast, stuff being cheaper).

-> the debt is near 99.8% of gdp (!!!) and could pass 52t by 2035, so any “ai saves us” story is... well, gl hf.

English

Elon Musk has said that AI will end America's debt crisis within 3 years, per BI

English

@Adam_Tehc hold up, gentlemen. patience.

x.com/eli5oftldr/sta…

ELI5 of TLDR@eli5oftldr

fed ended qt on dec 1, 2025. btc still fell –17.49% this month. if that confuses you, you are probably trading the wrong numbers. fed ending qt is not the auto‑bull signal. my imaginary quant says that maybe ~65% odds btc is higher 12 months after the qt end. but the path is “down / sideways / regret / aaaaaaa / then maybe up”. definietely not straight line. last time this happened: qt1 ended august 1, 2019 with btc at $10,417. by late november it was $7,182 (–31.0%), and by early feb 2020 it was still only $9,393 (–9.8%). sigh. the reason is obvious, if you are my imaginary quant: tga (treasury’s checking account at the fed) went higher after august, draining over $120b of bank reserves in 30 days, including an $83b jump on september 16. qt was “over” but liquidity was not. and btc doesn’t care about the word “qt”. i mean it, it's just a computer code. but btc is that weirdo computer code that actually cares about money. 2020–2023, btc’s correlation with global M2 (like all the world's money) was 0.94. during 2022–2025, US M2 shrank by about $2.20–$2.40 trillion, btc fell from ~$47,000 to ~$16,000, crabbed $16,000–$30,000, then only entered the "kinda_up_only_mode.exe" mode once liquidity stabilized and the market priced in qt end, btc climbed above $110,000. qt ending is a SIGN, BUT it's global liquidity being THE trigger. nonetheless, good luck, gentlemen!

English

QT is officially ending but be patient with your bags.

Historically bitcoin leads tightening of the balance sheet (quick to dump) but lags expansions of the balance sheet (slow to rise).

Last time QT ended (2019) it took Bitcoin 59 weeks to break out.

Watcher.Guru@WatcherGuru

JUST IN: 🇺🇸 Federal Reserve officially ends quantitative tightening.

English

fed ended qt on dec 1, 2025. btc still fell –17.49% this month.

if that confuses you, you are probably trading the wrong numbers.

fed ending qt is not the auto‑bull signal.

my imaginary quant says that maybe ~65% odds btc is higher 12 months after the qt end. but the path is “down / sideways / regret / aaaaaaa / then maybe up”. definietely not straight line.

last time this happened:

qt1 ended august 1, 2019 with btc at $10,417.

by late november it was $7,182 (–31.0%), and by early feb 2020 it was still only $9,393 (–9.8%). sigh.

the reason is obvious, if you are my imaginary quant: tga (treasury’s checking account at the fed) went higher after august, draining over $120b of bank reserves in 30 days, including an $83b jump on september 16.

qt was “over” but liquidity was not.

and btc doesn’t care about the word “qt”. i mean it, it's just a computer code.

but btc is that weirdo computer code that actually cares about money.

2020–2023, btc’s correlation with global M2 (like all the world's money) was 0.94.

during 2022–2025, US M2 shrank by about $2.20–$2.40 trillion, btc fell from ~$47,000 to ~$16,000, crabbed $16,000–$30,000, then only entered the "kinda_up_only_mode.exe" mode once liquidity stabilized and the market priced in qt end, btc climbed above $110,000.

qt ending is a SIGN, BUT it's global liquidity being THE trigger.

nonetheless, good luck, gentlemen!

Zeneca🔮@Zeneca

I was told by some very legitimate sounding YouTubers that this means alt szn starts now

English

the idea that ‘mstr is just levered btc’ is one of the more dangerous boomer takes in this market.

it’s actually a funding vehicle that moves about 1.8x as much as btc, owes 8.16b usd in convert debt, and starts to break once the stock is only worth the coins and nothing else.

but

mstr doing a true luna-style zero is very unlikely (<3%)

BUT

the stock doing a luna-style chart (–80% to –95%) if btc nukes 20–30% while funding dries up is like 35–50% odds.

to put it in numbers for my fellow math-loving gentlemen:

1. Strategy hold ~650,000 btc on the books (~3.1% of supply), average cost around $74,433.

2. it owes about 8.16b usd in convertible bonds (lenders can ask for cash or take shares), pays around 0.421% interest, and those start coming due between 2028 and 2032.

3. no active btc margin loan anymore; the old $21k btc margin meme is dead.

4. real insolvency (when their debt is higher than coins they hold) only happens if btc chills under roughly $12,000–$16,500.

here's a free lesson on finance:

nav = value of all btc minus all debt.

mnav = stock market value / that nav.

mnav 1.0x = stock exactly equals coin value.

mnav >2.5x = hype zone, they can sell shares, buy more btc, and everyone wins.

mnav <1.0x = stock trades cheaper than its coins → market saying “no thanks” to Strategy and its [redacted].

as of now, it's around 1.2x down from ~3.2x a year ago as big money rotated ~$5.4b into clean btc etfs instead of mstr. that collapse in premium is the first crack. i wonder why Saylor doesn't fud etfs, even indirectly.

they owe roughly $690m–$840m per year (interest + preferred dividends) while the actual business (selling some software?) is cash-flow negative (around –$45m). that means they must either sell more shares or sell some btc over time.

2027 is the final boss:

sept 15, 2027, a $1.01b convertible note where bondholders can ask for cash IF the stock is below $181.82.

however, IF mnav is sub-1.0x and stock is weak into that date (below that $181.82), the board has three moves: heavy dilution, btc sales, or pissing off creditors. none are bullish, no?

forced btc selling will be a spark.

if they dump, idk, 5–10% of the stack (32,500–65,000 btc), that’s ~$2.8b–$5.6b. if done in 1–3 days, current books probably move btc –15% to –25% just from that. then: futures and perps puke $30b–$50b of forced liquidations around key levels, leveraged mstr products mechanically sell 1b–2b to rebalance, passive funds auto-dump because of their rulebooks. domino.

so, next time you see bros fudding mstr:

terra-style system death (auto mint/burn, instant zero): almost no chances here because mstr is over-collateralized with btc and there’s no onchain peg. it's not like 1 mstr MUST equal X btc.

terra-style equity massacre (forced selling, no new money coming in, constant share dilution, and a down‑only chart for years): ok maybe if btc does –20–30% into a tight credit window.

as of now, i'd just wait for sept 15, 2027 put date. that’s where the quiet funding problem can turn into a very loud equity problem.

nonetheless, good luck, gentlemen!

Sandeep | CEO, Polygon Foundation (※,※)@sandeepnailwal

I just wish, hope, and pray that MSTR is not the LUNA of this cycle. Another public, but this time, Wall Street–retail-entangled death spiral is the last thing this industry needs. Hoping Saylor can pull some Wall Street voodoo magic.

English

ELI5 of TLDR 已转推

with each halving bitcoin is getting less secure.

once we are done with the reward issuance, then what? will government subsidy miners to keep them securing the network?

right now miners get roughly $100,000,000 per day from new coins and ~$264,000 per day from fees.

that’s ~0.26% fees.

after 4 halvings, fees are still a rounding error. empirically, fee revenue has been negative-to-flat vs subsidy cuts (like -0.32 to 0.0). the market already answered “will fees just scale up?” with “nope”.

the 2024 halving. fees briefly hit ~16% of rewards during the runes/ordinals mania, then bled back to ~1% within months.

1%!!!

year-on-year, fees were down ~79.91% and tx volume down ~25%. yeah, 2140 gonna be fine.

and you’re part of the problem (not judging). lightning network (bitcoin's l2) made txs 97–99.9% cheaper: 1 sat vs $0.30–$2.00 btc mainnet. volume up like 266–317% in 2024–2025. so if bitcoin bros will get disgusted by paying fees on the l1 that are are >2–5% of the tx value, why wouldn't they migrate to some l2? and then, less demand for blockspace → less fee revenue. if btc l2s pull of, their success pulls value off l1.

picture an actual miner: you’ve got power bills in fiat, hardware that decays, and a spreadsheet. you don’t care if your revenue is “subsidy” or “fees”. you care that each block pays you more than your cost per TH/s per day. if subsidy shrinks faster than fees grow, you unplug. simple.

2024 halving:

block reward went 6.25 → 3.125 btc. hash rate (which is the total "power" used to secure bitcoin) dropped ~11.2% (from ~650 EH/s to ~577 EH/s), then ripped to ~1.1 ZH/s over 7 months.

why?

because price went from ~$60k to $90k+.

miners follow price, not “security philosophy”. the network is effectively secured by new buyers bidding the coin up, not by a "mature fee market."

and now let's do some "bitcoin goes down because it's literally attacked" scenario:

at ~1.1 ZH/s, a proper 51% attack is estimated around $6,000,000,000 per week in op-ex, plus maybe $5–20b in hardware. cut hash in half to ~550 EH/s (ol'good bear market + more halvings) and weekly op-ex drops toward $1,800,000,000.

that's pennies for state actors.

every halving makes honest mining thinner and attack costs cheaper relative to potential payoff. at some point, a state or cartel can spend a few billion, short btc, nuke confidence with reorgs, and walk away net positive. below certain hash levels it blends into normal cyber budget.

and it gets worse once blocks are paid only with fees.

“selfish mining” = a miner finds a block, hides it, and plays games with timing to earn *more than their fair share* of rewards.

in the old, simple model (only fixed block rewards), you needed about 33.33% of the hashrate to make this profitable.

today, because fees jump around a lot from block to block, the threshold is already closer to ~26%.

in a future world with no subsidy and crazy fee spikes, that threshold drops even further, to roughly 15–23%.

translation: you don’t need “half the network” to take over bitcoin. just one big pool deciding to play dirty.

in 2025, koki kamada and tomoya noda published a paper on bitcoin’s security budget.

to tldr their findings: if you want the network to be secure, the block reward should never fully go to 0. some positive subsidy is always “socially optimal”.

to eli5 their findings: the math says a zero-subsidy bitcoin is bad for long-term security.

right now, fees are only about 1.05% of miner revenue, so they are nowhere close to replacing the security budget that comes from new coins being issued.

so the math literally says "21m cap no bueno". but the 2017 blocksize war proved one thing: bitcoin maxis treat the 21,000,000 cap as religion. hard-forking in perpetual inflation is gg wp.

what is to be done, gentlemen?

Uncle ↑@UncleRewards

There are THREE forbidden questions in crypto: - Don't ask a $BTC maxi what happens when block subsidies goes to 0 - Don't ask Toly how much $SOL he and the foundation have - Don't ask VCs why we need yet another L1 blockchain $ETH fixes all these things, btw

English