Andy

465 posts

Andy 已转推

Some perspective on bubbles:

• Cisco went from $1 to $53 in just 5 years.

• It had three large drawdowns on the way up.

• Its P/E multiple expanded from 26 to 232.

• It stayed above the 50 & 200 SMAs nearly the entire time.

• Revenue climbed from $1.9B to $17.8B (and peaked at $23.8B a year later).

I bet there were people calling the top the entire run.

English

Andy 已转推

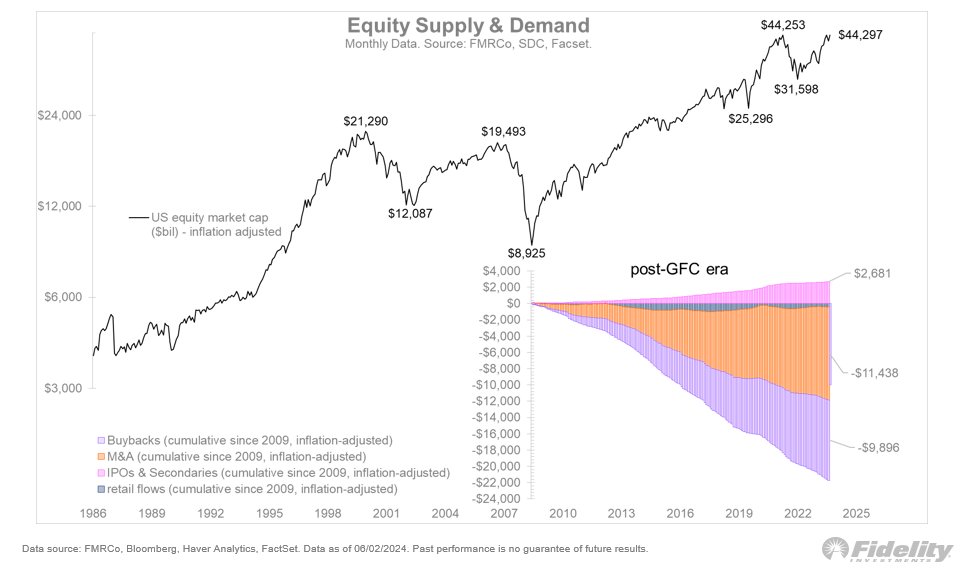

On a cumulative basis since 2009, the issuance of shares totals $2.7 trillion, while the reduction in shares totals $21.3 trillion. That’s a huge supply/demand imbalance against a market cap of $44 trillion. No wonder the market has gained so much since the secular bull market began in 2009! /4

English

Andy 已转推

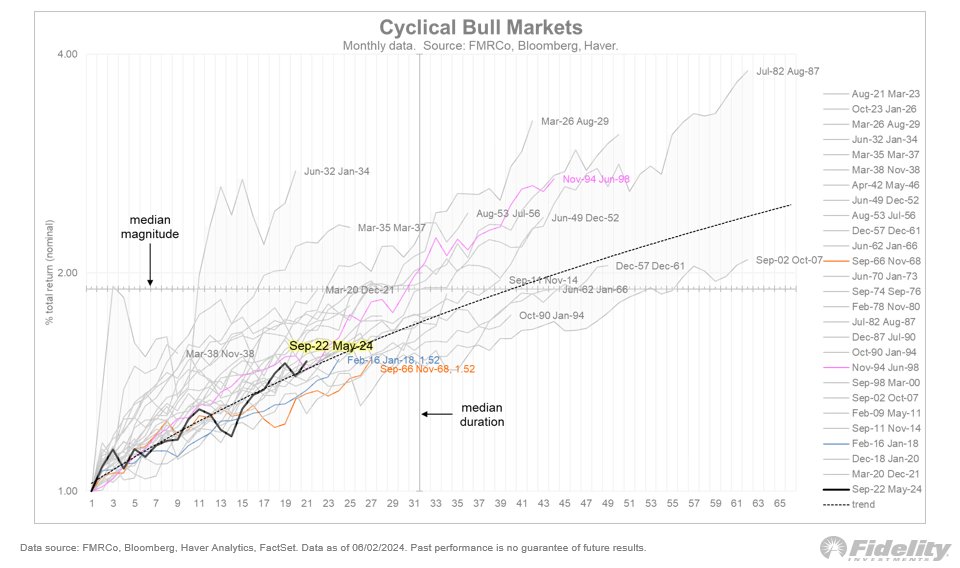

The current bull market cycle is 20 months old and produced a 53% gain. By historical standards there seems to be life left for this bull, given the median 30 months and 90% gains that’ve been produced over the past 100 years or so. We might only be in the 5thinning. 🧵

English

Andy 已转推

#CELH

#季節概念股

#長期成長股

#做長做短都可以

#非電族群個股

當大家的關注焦點都在黃教主身上時, 我們也需要把眼光轉移到一些其他有機會的個股身上, 夏季要來了, 很多季節概念股已經啟動!~

中文

Andy 已转推

Andy 已转推

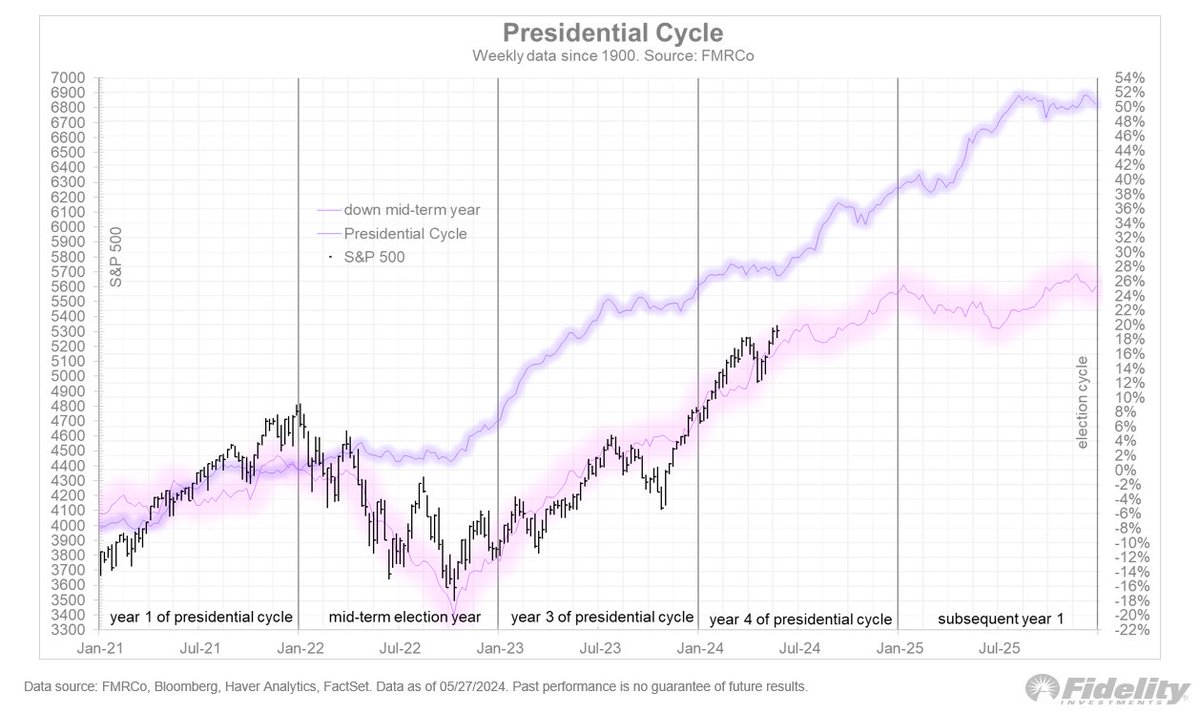

We are in year 4 of the Presidential cycle, and that year tends to be strong, especially when it follows a down mid-term year. The market has closely followed this “down mid-term” cycle.🧵

English

Andy 已转推

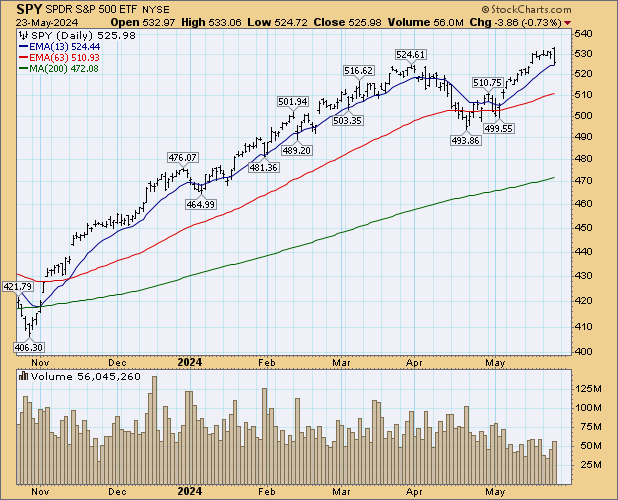

Big outside reversal day in $SPY. Enough to stop the bull run for a while? I report; you decide...

English

Andy 已转推

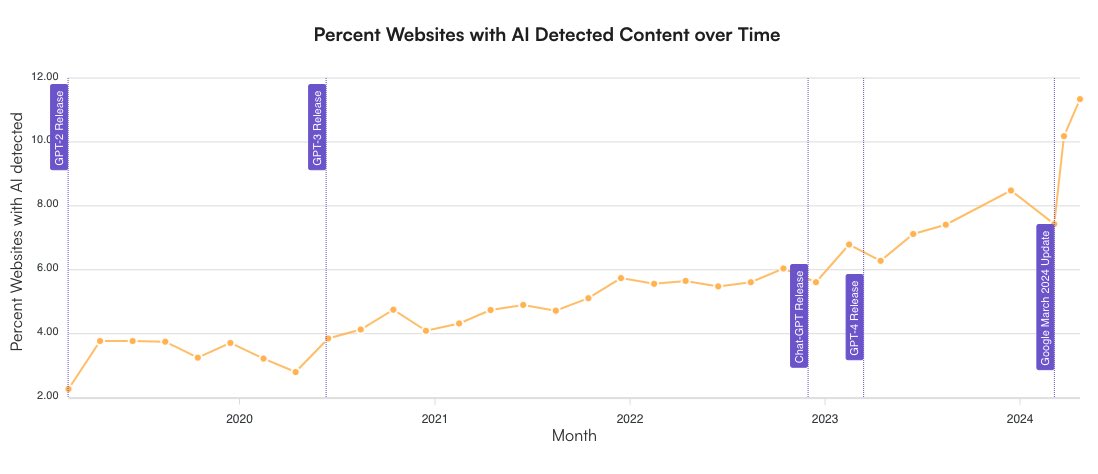

AI-generated content in $GOOG search results continues to grow at a disturbing rate. The % of websites with AI content this month was almost twice the % last year, climbing to almost 12%

The spread of AI generated content has a few implications for $GOOG and several companies in the media/internet space…

Perversely, I think this trend benefits Google.

As more AI content saturate the search results, it makes it even more competitive for companies to compete for limited digital real estate. Which means they’ll have to pay even more for online advertising if they want visibility. Companies like $GOOG, $MSFT (with LinkedIn), $META and even $ROKU could benefit from all these new ad dollars

Remember, all this new AI generated content is in addition to AI generated answers shown on the very top of many Google search queries, which pushes down organic search results even further.

Of course, this trend isn’t new. It’s been ongoing for the past decade+ with content farms, auto-generated content and AI will only exacerbate it. While it’s true that consumers might switch to ChatGPT but consumer habits are very hard to change over time.

2nd, as AI-generated content becomes popular, ppl will become increasingly skeptical of anything they read online, especially if it’s not from a reputable brand or influencer.

Which means they’ll increasingly start to look for “human content”. Platforms like $RDDT should continue to benefit (and already have been as shown by the popularity of appending “Reddit” to many searches).

I also think influencer marketing will continue to be big as well, though I don’t know how you would play this in the public market. But if you have a huge loyal following with lots of connections, you will be highly coveted by brands.

3rd, I think this trend doesn’t bode well at all for any new companies or startups. The barrier to entry to making anything whether it’s online content, a product, a cold email has been diminished to almost zero with AI.

Yet the amount of $$$ needed to market and sell that product has increased tremendously. AI generated content will saturate almost every single marketing channel: not just search results. But social media, email, even cold calls. Good luck trying to reach anyone when the other persons guard is high, skeptical that they’re being pitched to by an AI bot.

It’s always been hard to sell anything, but with AI, it will become almost impossible to sell anything unless you are already a big brand and have the distribution network in place.

Once again, the big players and incumbents in SaaS like $CRM $MSFT $NOW $GOOG will benefit here.

Source of chart below: Originality (dot) AI

English

Andy 已转推

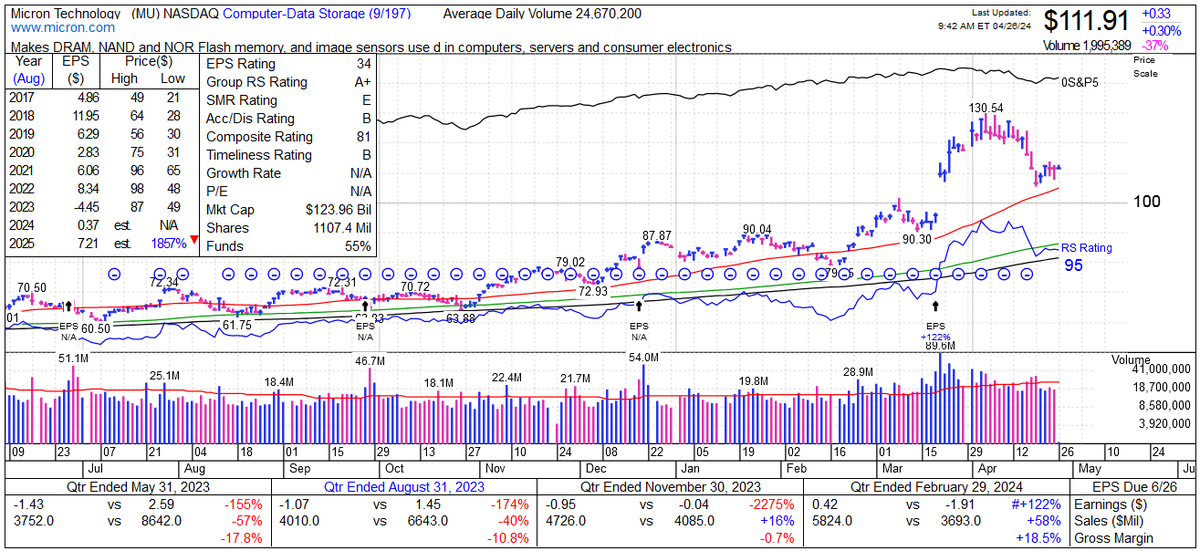

I'm looking for stocks to buy out of this correction. Micron Technology $MU has historically been a growth cyclical. It appears the AI technology and the AI environment is creating the conditions or potential for a longer EPS up cycle. The stock just hit an all-time high from a large base entering the beginning of a new Stage 2 uptrend on the heels of an excellent EPS report. This is my favorite technofundo setup, where the rubber meets the road on both during a correction. The stock may need to pullback a bit more or consolidate. But I would look for this name to setup as a potential leader.

English

Andy 已转推

Andy 已转推

I recommend watching this video review of the Xiaomi SU7 to better understand the competition in China. This particular review is pretty good.

The Xiaomi SU7 competes directly with the Model 3 and seems to have its own strengths.

youtu.be/xxwym-V_OYE

YouTube

English

Andy 已转推

We were correct to reduce our $TSLA position from 12.2% in Sept 2022 to 2.7% today because of our concern about deteriorating fundamentals. In hindsight we should have sold our entire $TSLA position rather than kept a small % of it. We were right that cutting prices wouldn’t generate much volume growth. We were right that TSLA needed to start advertising to try to convince ICE owners to go EV. We were right that FSD would not reach L4/L5 needed to be robotaxis anytime soon. We were right that TSLA needed to prioritize the $25K compact to compete effectively with the Chinese EV makers. We were wrong in believing Cybertruck interest would create a halo effect for the entire franchise. We were wrong to believe TSLA would figure out that cutting prices just causes consumers to wait for more price cuts.

Gary Black@garyblack00

Ironic that @TSLAFanMtl @realMeetKevin @GerberKawasaki and I have been right to be cautious on $TSLA over the past year and still get attacked by bulls who want to believe everything at $TSLA is wonderful despite the 50% collapse in $TSLA earnings power over the past year. Where’s the analytical rigor?

English

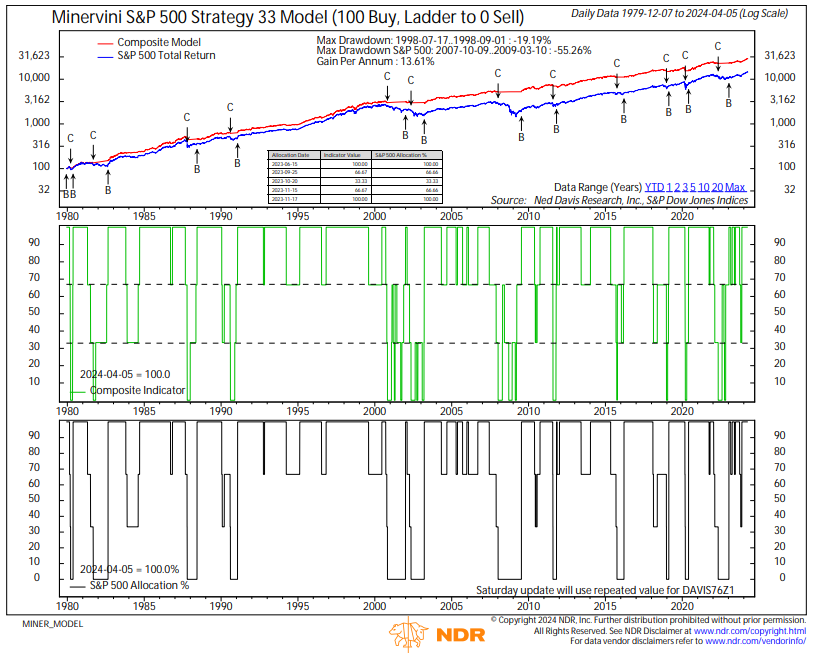

Andy 已转推

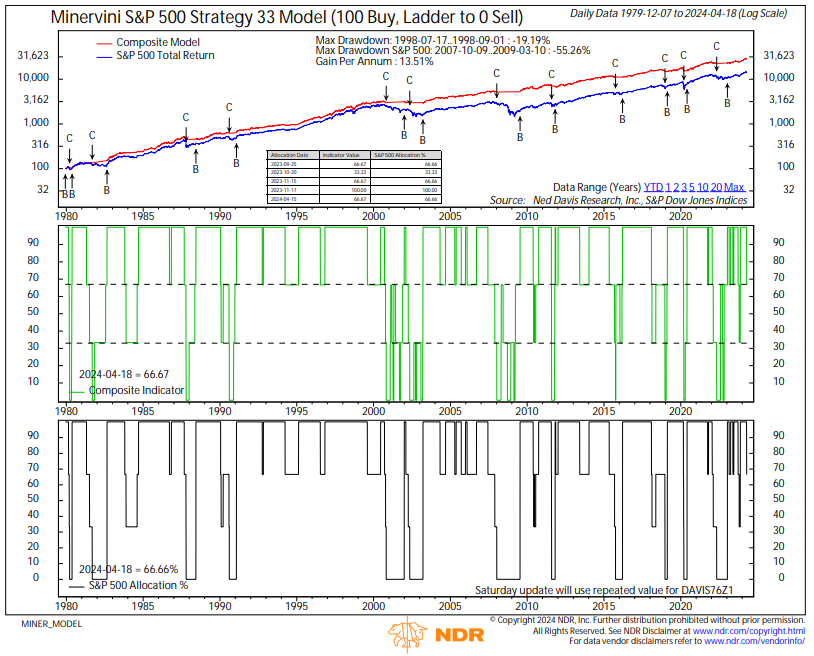

The market is oversold by a number of measures and this could produce a snap back rally, but sentiment and stock action have us sidelined and still holding our $DIA short position.

Long term, I think we are in a correction within an on-going bull market. It is normal for the major averages to pullback 5-8% and in some cases as much as 10-12%. While sentiment is indeed frothy, long term sentiment measures like margin debt and IPO/secondary action have yet to reach levels that would signal a major top.

In the near term, volatility risk remains elevated. In our view, a reliable or effective bottom has not yet been established. For the time being - certainly for breakout traders - cash is king.

Long term investors acting in line with our SPY Model (which triggered a buy signal on January 13, 2023) should stay the course with suggested exposures. The model did ladder into some cash yesterday, moving from 100% invested to 67%. A major sell signal occurs when the model moves to 0%

minervini.com

English

Andy 已转推

Long term I remain bullish on the market. Our long term trend model is holding on to the Jan. 13, 2023 buy signal. In the short term, I'm positioned for a pullback. Two days ago we shorted the $DIA with a stop up at the ATH. That's only a little more than 2% risk on one of the most liquid of all indexes/ETFs. A 5-8% (possibly 10-12%) pullback would be normal in a bull market. Of course, tomorrow's highly anticipated CPI data will likely fuel volatility, and possibly a last push, pop or rally before a correction. As long as my stop holds, I'm fine with that.

minervini.com

English

Andy 已转推

We opened relatively strong this morning, but turned decidedly red. Since our March 4th STEM downgrade (our stock only Stock Trading Environment Model), the indexes have made little progress. Stocks in general have been mixed. We slowed our roll considerably in February and continue to take a cautious and very selective approach. We already sold most of our positions into strength and de risked the ones we are currently holding. Indexes are still holding intermediate uptrends. Beneath the surface volatility has picked up a bit and breakouts are not working as well as they were earlier in the year. At this point, it's a matter of waiting for stocks setups to develop and riding the brake until breakouts start working well again. Bull market is still intact, but rotational pullback seems to be in progress. minervini.com

English

Andy 已转推

Peter Thiel recruited Reid Hoffman, Chad Hurley, Sam Altman, David Sacks, and Keith Rabois. Also partnered with Elon Musk.

He's used these 4 questions time and time again to identify 20-year-olds who would go on to be billionaires.

Test yourself with these questions:

English

Andy 已转推

$RIVN reminds me of $TSLA in 2019 when naysayers predicted it would run out of cash and the equity would be worthless. If $RIVN can execute on its plans, production will increase to 215K once the Normal plant is expanded for R2, and add another 400K new R3 production at the Georgia facility, so 615K total capacity in 5-7 years.

At an avg selling price of $45K ($75K for R1, $45K for R2, and $35K for R3) and a 20% auto gross margin, 2030 could look as follows:

- Delivs 526K

- Revs $22.7B

- Ebitda $2.5B

At a 3.5x EV/Rev multiple (TSLA equivalent), RIVN could be worth $67/share in 2030, or $30/share in present value at a 14.1% equity discount rate (+136% upside).

At a 20x EV/Ebitda multiple (TSLA equivalent), RIVN could be worth $45/share or $20/share today (+57% upside).

English

Andy 已转推

I am uncomfortable growing Tesla to be a leader in AI & robotics without having ~25% voting control. Enough to be influential, but not so much that I can’t be overturned.

Unless that is the case, I would prefer to build products outside of Tesla. You don’t seem to understand that Tesla is not one startup, but a dozen. Simply look at the delta between what Tesla does and GM.

As for stock ownership itself being enough motivation, Fidelity and other own similar stakes to me. Why don’t they show up for work?

English