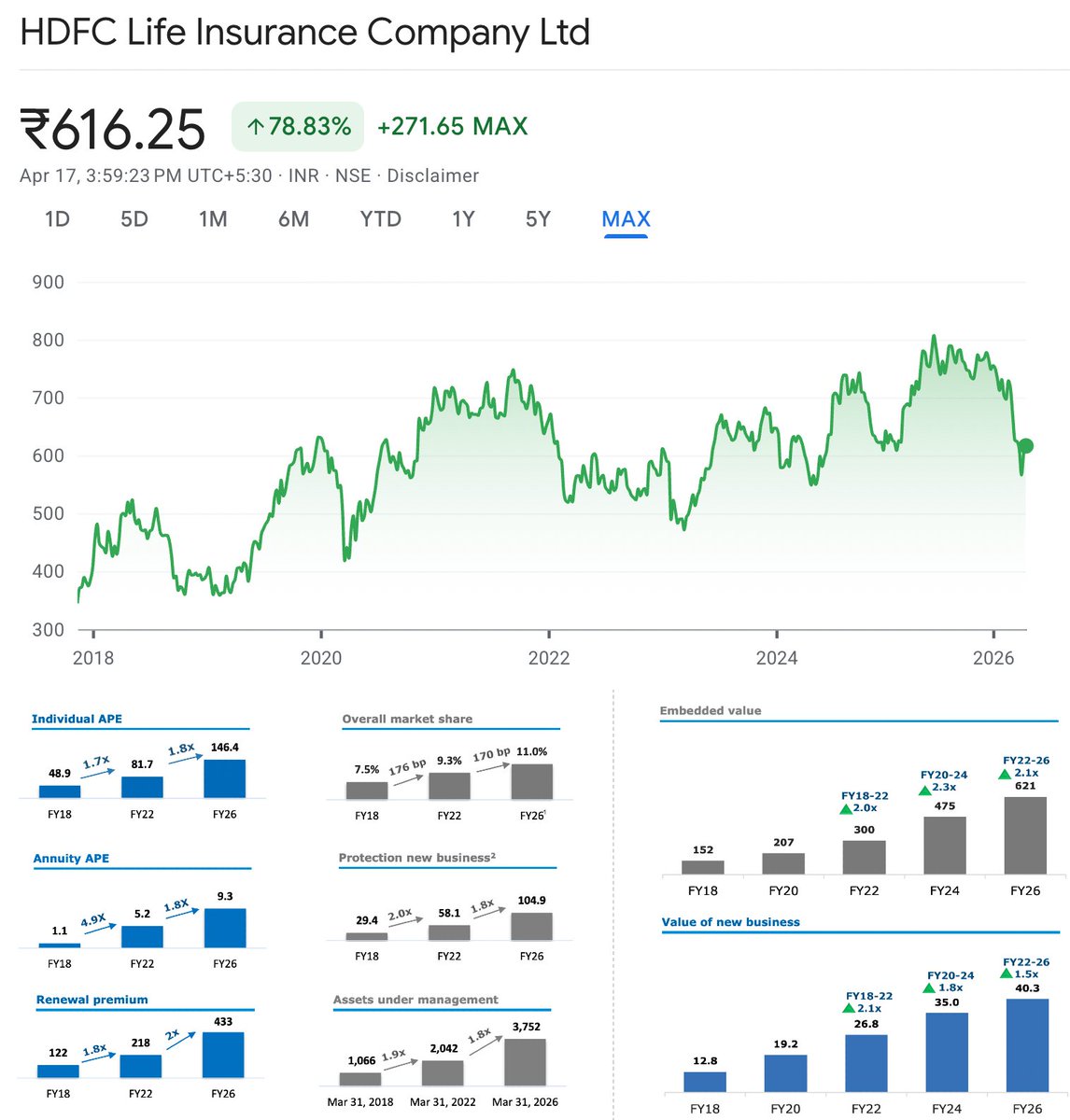

Crazy de-rating in HDFC Life Insurance

Stock is currently trading near 2019 levels - nearly 7 years of consolidation

Once a market favourite, valuation multiple has sharply compressed over time

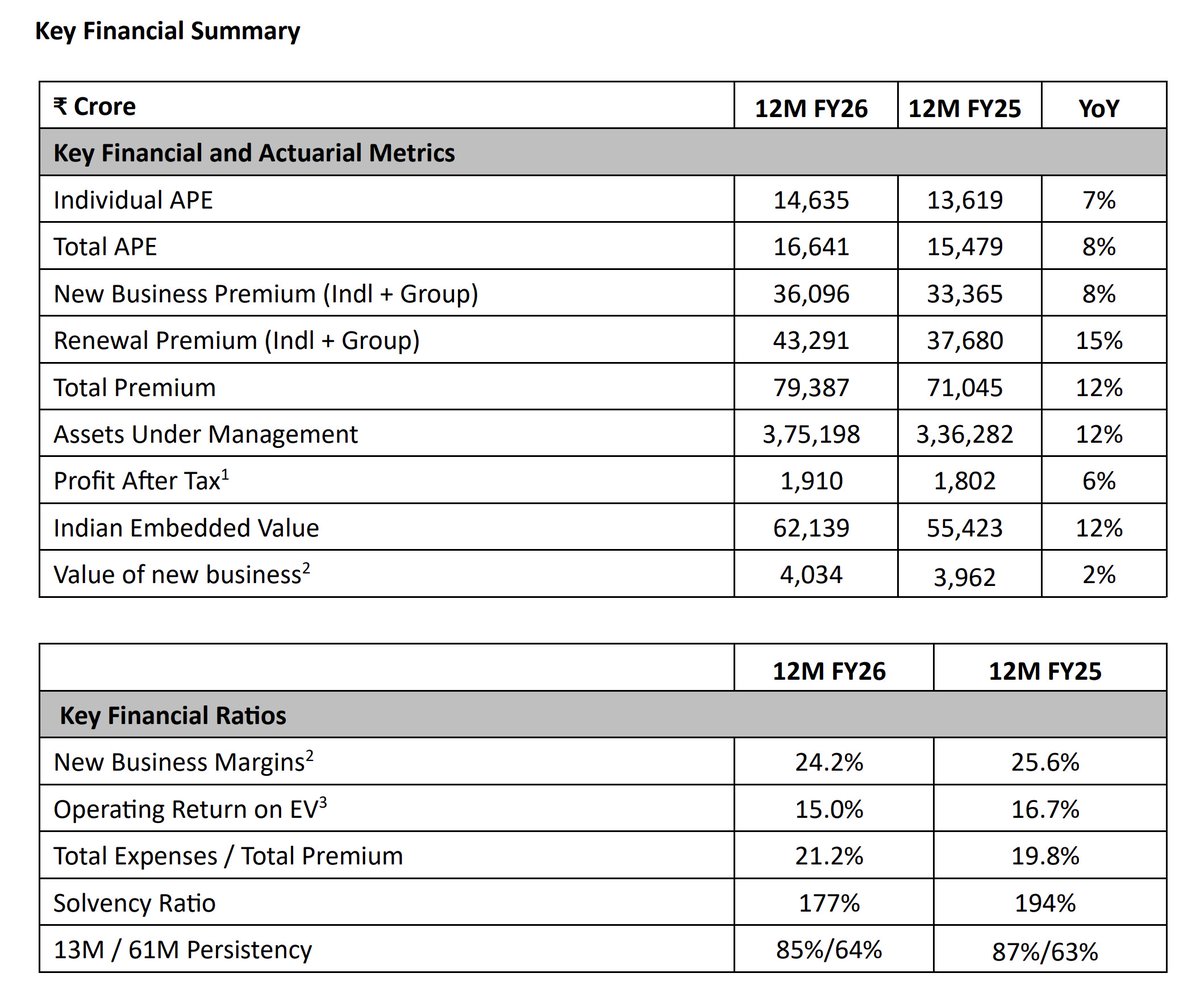

Embedded Value (EV)

FY20 - 20kCr

FY26 - 62k Cr

MCap / EV earlier - above 6x

MCap / EV now - 2x (66% derating)

English