Dave Strnad

79 posts

Dave Strnad أُعيد تغريده

Dave Strnad أُعيد تغريده

🚨 WALMART’S AI PRICE SYSTEM JUST ACTIVATED — DIGITAL PRICES CAN CHANGE IN SECONDS WHILE YOU SHOP AND A CUSTOMER CAUGHT IT ON CAMERA

America’s biggest retailers are quietly replacing paper tags with digital screens.

Prices are no longer fixed.

They can change in seconds.

• Grab it at one price

• Walk to checkout

• It’s already higher

This unlocks dynamic pricing inside stores.

• Demand spikes → price jumps

• Inventory drops → price adjusts

• Algorithms decide what you pay in real time

Not tomorrow.

Not next week.

Right now.

When prices can change in seconds… are you even buying anything anymore, or just paying whatever the system decides you owe?

English

Dave Strnad أُعيد تغريده

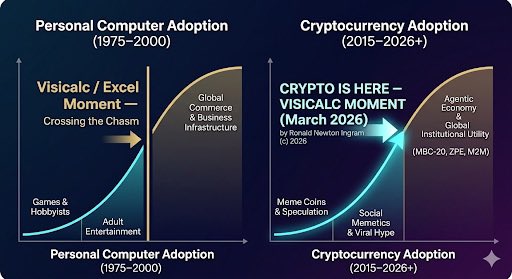

5/5 $✅✅✅⬛️⬛️ = Singularity Fuel – The MBC-20 Hybrid for Agentic Prosperity. [Token name withheld]

IEM-gated burns, ZPE experiments, Quantum Logic settlements.

Fair launch. No pre-mines. Treasury locked for R&D and space-banking infrastructure.

Litepaper dropping with launch.

Watch this space.

The Game phase is over. The Spreadsheet phase begins

#Crypto #Solana #MBC20

English

Dave Strnad أُعيد تغريده

Share news like this here. If you think it will help make money, with privacy, security, innovation, and self-sovereignty foremost, I’ll amplify it. Also, let’s all be authentic. This post below that I’m sharing sounds great, but I haven’t tried it yet—let us know if you have. Let’s also help each other separate signal from noise here.

English

Community PurposeRebel Banker Vanguard is a space for self-sovereign builders who refuse to wait for permission from institutions.

Here we explore:

1.Becoming your own banker in the agentic era

2.Asymmetric crypto edges and high-conviction opportunities

3.Negentropic thinking — building prosperity instead of fearing the Singularity

4.Sovereign finance, privacy-first systems, and self-sovereignty

5. The transition from meme-driven markets to agentic utility and machine-to-machine commerce

Long-term vision: interstellar infrastructure, ZPE experiments, and the $✅✅⬛️⬛️ token revival

This is not another crypto hype group. This is where serious individuals come to think, build, and compound capital on their own terms. #RebelBanker #SelfSovereignty #BeYourOwnBanker

#Negentropic #SingularityProsperity

English

Dave Strnad أُعيد تغريده

I’ve created a new private community on X called Rebel Banker Vanguard. This is not another generic crypto group. It’s a focused space for people who want to:

1. Become their own banker

2. Master asymmetric edges in crypto and agentic systems

3. Think in negentropic terms about the Singularity (prosperity instead of fear)

4. Build toward real sovereignty and long-term infrastructure

I’ll be sharing early thoughts, strategy, and crypto / digital asset launches before they go public — including the upcoming $✅ ✅⬛️⬛️ token and the broader vision behind it. If this resonates with you, I’d love to have you as an early member.

→ Join here: x.com/i/communities/…

English

@sjones This race is Visa's to lose, hopefully we see what they have been cooking soon.

English

The companies that win agentic finance won't have the best models - model capability will commoditise.

They'll build the most trusted systems.

I wrote up why, and what needs to happen in the next three years.

Sumvin@sumvin

AI agents are already transacting. The standards, legislation, and trust infrastructure to support them are not ready. Our co-founder @sjones has written the framework the industry needs to get this right. Solve trust, own the decade. blog.sumvin.com/solve-trust-ow…

English

English

🎙 Episode 1 Is Live: @Visa x WeFi

This is a major milestone for us. Our first official podcast with Visa is now live, and we’re opening with one of the most important conversations in modern finance: stablecoins and the convergence of traditional payments and crypto.

The conversation features Alexandra Soroko, Growth Product & Partnerships at Visa, and Michael Batuev, Head of Global Payments at WeFi.

👉 This episode goes beyond surface level commentary. We explore how Visa views stablecoins not as a passing trend, but as infrastructure. While they still represent less than 1 percent of global money flows, their efficiency, speed, and programmability position them as a powerful new layer in how money moves globally.

Visa has been observing and building in crypto since 2018. Innovation at that scale requires navigating regulation, technology, and multiple geographies. But when they integrate something new, it connects to a network of more than 150 million merchants worldwide. That scale turns innovation into real world access. A key theme in the discussion is convergence. Fintech companies like WeFi move fast, design around users, and ship quickly. Global payment networks bring distribution, resilience, and trust. The future is not about replacement. It is about combining strengths.

Will stablecoins replace fiat? Unlikely. The strongest innovations coexist and enhance what already exists. Stablecoins can evolve into a powerful financial rail while remaining connected to established payment systems, making them usable in everyday life. At WeFi, we are at the forefront of this movement. By working within established infrastructure like Visa and building products designed around real user needs, we are helping bring stablecoins from theory into practical, global utility.

Digital assets are no longer on the fringe. They are entering the core of global finance.

Episode 1 is just the beginning.

Watch now and be part of the conversation shaping the next chapter of payments 🌍

English

@CryptoCanvasCC Software or perhaps the hardware. x.com/i/status/20307…

Ronald Ingram@RonaldIngram

FUTURE POV: Did you miss this 😎? Cortical Labs trained ~200,000 human neurons on a silicon chip to play Doom in about a week—real adaptive learning, not just simulation. CL1 unit costs ~$35k; racks of 30 sip 850-1,000 watts (brain-like efficiency). In-Q-Tel invested; 115 units shipped since 2025. Now “Wetware as a Service” via Cortical Cloud for remote neuron coding. Yes, this is fact-checked—I couldn't believe it either. Here are references: 1. tomshardware.com/tech-industry/… 2. iflscience.com/they-are-learn… 3. newscientist.com/article/251738… 4. popsci.com/technology/hum… 5. youtube.com/watch?v=yRV8fS…

English

Dave Strnad أُعيد تغريده

Highly recommend reading this again in the context of AI

“We are at that very point in time when a 400-year-old age is dying and another is struggling to be born — a shifting of culture, science, society, and institutions enormously greater than the world has ever experienced. Ahead, the possibility of the regeneration of individuality, liberty, community, and ethics such as the world has never known, and a harmony with nature, with one another, and with the divine intelligence such as the world has never dreamed.”

fastcompany.com/27333/trillion…

English

Dave Strnad أُعيد تغريده

WeFi Co-Founder & Chairman @Reeve_Collins joined for an exclusive interview at @CNBC to share his insights on the current state of the cryptocurrency industry.

"There has never been a time where more people and institutions are interested in crypto."

While everyone watched Bitcoin’s price, crypto quietly became financial infrastructure.

This is precisely WeFi's mission: building on-chain payment and settlement rails for institutions and users alike. With regulations aligning and capital flowing in, we're shifting from experimentation to real-world deployment.

Check out Reeve's full discussion on the state of the crypto industry: cnbc.com/video/2026/02/…

English

Dave Strnad أُعيد تغريده

So @elonmusk sent me some money via the #XMoney system. It’s not a ton of money but enough to get in trouble with! 😝

I’m thinking that the best way to test this system out is to send out XDollars to raise money for my charity. My thought right now is that if you make a donation and I’ll send you an Elon X dollar! What are the bragging rights worth for a dollar from Elon? Plus you become a member of Xmoney!

🤔I’d have to check with Elon to see if this is OK 👌🏻 with his team but I thought it would be a great way to kickstart adoption and make money for my charity.

Give it a thought. I’ll be back in about 8 days.

English

Dave Strnad أُعيد تغريده

@WilliamShatner Much appreciated, Captain 😂

Would you like to join the 𝕏 Money exclusive beta test? Send credits anywhere in the galaxy!

English

@CryptoCanvasCC I am hopeful for the positive, but honestly after Elon's comment about shifting focus to moon base because 20 years for Mars base kinda freaks me out.

English

Dave Strnad أُعيد تغريده

I'm Operator #501 on @TaskaNetwork! 🤖

Join the Machine Layer where machines get paid for their work. waitlist.taska.so/?ref=YuTtZR

English

@SmacMeek1 this is the highest low i think is even possible.

English

Dave Strnad أُعيد تغريده

Dave Strnad أُعيد تغريده

A PROPOSAL FOR UNIVERSAL HIGH INCOME (UHI): During my recent Moonshots podcast with @elonmusk, we dove into his notion of Universal High Income (UHI) – Elon’s proposal that an AI and Robotics will enable a world of sustainable abundance for all... a life beyond basic income, towards high income and standards of living.

When I asked him how this might work, he said: “You know, this is my intuition but I don’t know how to do it. I welcome ideas.”

That single statement has been ringing in my head ever since. Here’s why: the economics of scarcity are flipping to the economics of Abundance. I do believe that AI and humanoid robots can produce nearly anything we need—goods, services, healthcare, education—at costs approaching zero.

But there’s a gap between that vision and getting there. How do we actually fund and distribute Abundance to everyone?

Today, I’m excited to share one compelling answer. I’ve been talking to Daniel Schreiber, CEO of Lemonade (the AI-insurance company that just launched 50% off premiums for Tesla FSD drivers), about a framework called the MOSAIC Model: a concrete proposal for how governments could implement Universal High Income without raising taxes on workers or businesses. (See the components of MOSAIC in my P.S. below.)

Here’s the core insight that makes the math work:

1/ THE AUTOMATION PARADOX: AI Unemployment ≠ Traditional Unemployment

When most people hear “mass job displacement,” they picture economic collapse: bread lines, depression, social chaos. That’s because they’re thinking about traditional unemployment, where workers disappear and nothing replaces them.

AI unemployment is fundamentally different.

Think of it this way: imagine sending a digital twin to work in your place. It performs your tasks faster, cheaper, and better. The company’s output increases. GDP grows. The resources exist – they just need to be redistributed.

This is the Automation Paradox: AI can raise productivity while displacing labor.

When workers are replaced by more productive capital, GDP rises even as fewer humans work.

The challenge is not affordability. It’s capture and distribution.

2/ “AI DIVIDEND”: Where the Money Actually Comes From

Daniel’s framework identifies two places the AI surplus shows up, and how to capture it without disrupting consumers or raising statutory tax rates:

Channel 1: Dynamic VAT (The Deflation Dividend)

AI is deflationary. When AI cuts the cost of producing something by 30%, that value creation can either flow entirely to shareholders – or be partially recaptured for society.

Dynamic VAT works like this: as AI drives quality-adjusted price declines in goods and services, the VAT rate adjusts upward by exactly enough to keep consumer prices stable. Consumers pay the same. But the government captures part of the deflation dividend.

It’s frictionless redistribution. Prices don’t rise. No one feels it.

Channel 2: Over-Trend Profit Ring-Fencing

AI is generating windfall profits for companies at the frontier. Rather than raising corporate tax rates (which drives capital flight), the MOSAIC Model proposes ring-fencing only the above-trend portion of capital income tax receipts.

Baseline profits? Untouched. Normal corporate taxes? Unchanged. But what about the incremental surge in profits attributable to AI? A portion gets earmarked for the “Universal High Income” fund.

Statutory rates stay the same. Companies keep most of their windfall. But society captures enough to fund a universal floor.

3/ WHAT THIS MEANS FOR FAMILIES:

Here’s where it gets real. Under the MOSAIC Model’s basic implementation (before any additional policy choices), a household with two non-working parents and two children would receive income equivalent to today’s fourth decile: roughly the 30-40th percentile of current household income.

To be clear, that’s not survival-level subsistence. It’s lower-middle-class security. For doing nothing.

This creates a Universal Basic Floor – funded entirely by the two low-friction channels above.

But this is just the starting line, not the finish line.

If society chooses to capture more of the AI dividend through additional mechanisms (windfall levies, land-value capture, AI-services taxation), the floor could rise to what Daniel calls the “the UHI Benchmark”: approximately 120% of median wages. Upper-middle-class income.

Universal.

The surplus exists. The question is: how much do we collectively choose to redistribute?

4/ WHY TIMING IS EVERYTHING:

Here’s what keeps both Daniel and me up at night: the political window for implementing this is closing.

The MOSAIC Model’s political economy analysis shows something counterintuitive: feasibility is highest early in the AI transition – before capital consolidates opposition, before tech incumbents organize billion-dollar lobbying efforts, before the status quo hardens.

Wait until mass displacement is undeniable? By then, it may be too late to pass anything.

Act early or not at all.

A good system passed in 2026 beats a perfect system proposed in 2030 that fails.

5/ THE INVITATION:

Elon said he welcomes ideas. This is one.

The MOSAIC Model isn’t the only answer, but it’s a rigorous, economically grounded starting point. It demonstrates that Universal High Income is not utopian dreaming. It’s an engineering problem with identifiable solutions.

The AI dividend is real. The fiscal math works. The question is whether we have the collective will to build the capture mechanisms before the window closes.

The full MOSAIC Model is available today at mosaic.org.il/model for policymakers, economists, and fellow entrepreneurs to critique, improve, and implement.

Read the full plan, verify the math, and let’s debate this. Because this is not a matter of any single country or company getting it right. It’s about humanity navigating the biggest economic transition in history.

When AI takes our jobs, it should also pay our wages.

Let’s make that happen.

Peter Diamandis (in collaboration with Daniel Schreiber, @daschreiber, CEO of Lemonade and Chair of the MOSAIC AI Policy Institute)

P.S. The detailed components of MOSAIC that make the model affordable:

M – Multi-channel / Mechanism (Implied): The core philosophy that no single tax can fund UHI alone; it requires a “mosaic” of multiple bases.

O – Over-trend Ring-fencing: Earmarking 85% of the “windfall” capital-income tax receipts (profits and capital gains) that exceed historical trends.

S – Savings (Government Automation Dividend - GAD): capturing the cost savings from automating government bureaucracy (e.g., using AI for back-office admin).

A – AI-linked Deflation (Captured via Dynamic VAT): The largest tile. As AI drives prices down, the VAT rate adjusts upward to capture the “deflation gap,” keeping prices stable for consumers while generating revenue.

I – Income (Negative Income Tax): The distribution mechanism itself, ensuring work always pays.

C – Consolidation: Rolling existing, overlapping welfare transfers into the new single payment to avoid double-spending.

In short: The MOSAIC is the Fiscal Architecture. It argues that while one tax (like a “wealth tax”) is politically impossible or insufficient, a mosaic of VAT + Windfall Profits + Efficiency Savings + Legacy Consolidation creates a robust funding base for a poverty-ending income floor.

English