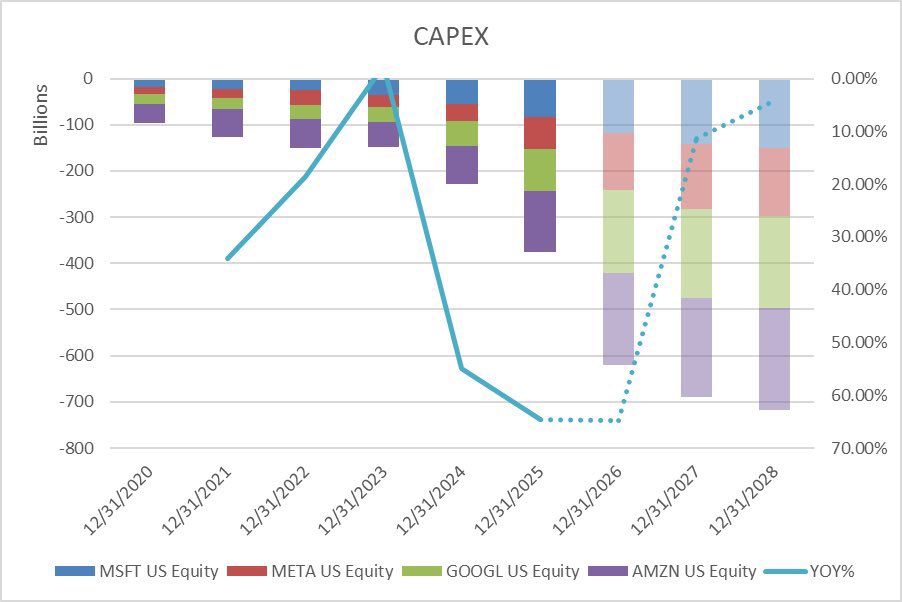

the biggest downside i see is next year capex, most of the capex is assumed from FCF, and the growth in capex they see in 2027 is funded mostly by the estimates for increased FCF, which is fine if a perfect scenario happens but oil price is going to pull consumption from possible growth of all non oil related sectors. so either hyperscalers products somehow maintain a completely inelastic demand profile AND grow alongside that inelastic demand, or demand falls for their products and earnings expectations for next year are too high. the obvious counter argument for this is the compute they are running makes the money to invest in more capex but the relative size of the hyperscalers legacy business makes that argument hard to balance against the small (as of right now) sales these companies make from ai compute specifically. The other alternative to this is issuing more debt/equity to pay for the increased capex if FCF doesnt't meet it.

this is ignoring all the possible cannablization of their legacy business sales from companies which might switch to paying for the insane cost of tokens.

English