🚦New research! "Trend following is not about alpha. It's about risk control."

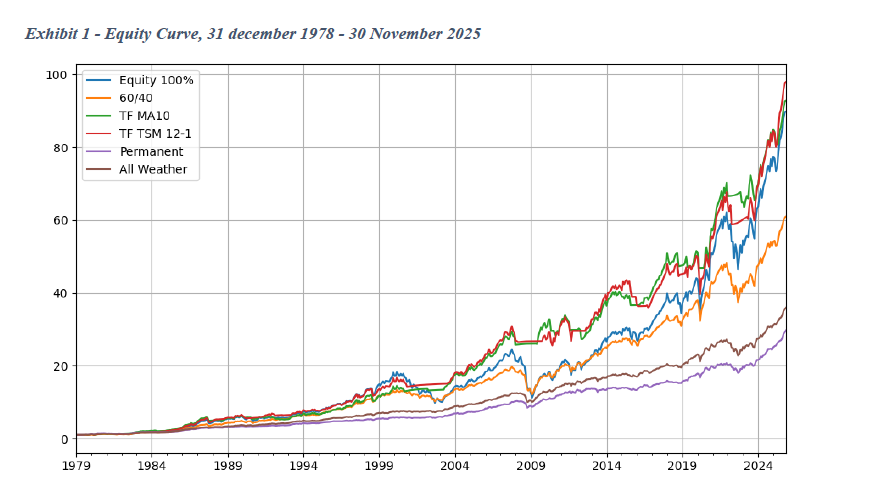

New research using data from 1979 to 2025:

Simple equity trend filters (10-month MA or 12-1 momentum) deliver:

* Same ~10% CAGR as buy-and-hold

* Max drawdown slashed from -54% → -20%

* Sharpe improved from 0.72 → 0.93

I always get the impression, in these dynamic asset allocation risk-on/off backtests, that the prob of curve fitting is high when filters are active only a few times.

What do you think?

Anw, worth taking a look.

📄 Paper: papers.ssrn.com/sol3/papers.cf…

→ More research like this in my weekly newsletter: ivanblanco.ai/newsletter

English