ApeChartz

6.5K posts

ApeChartz

@ApeChartz

Crypto Trader | Setups, Trades, and Full Analysis/Ideas Shown For Educational Purposes Only

Beigetreten Ekim 2021

211 Folgt26.4K Follower

@TraderJqrit @MuroCrypto @SailorManCrypto @ThePenguinXBT @swisstrader09 @George1Trader @EZCharts_ @Crypto_Scient thank you brotha, appreciate it!

English

its been a while since i gave a shoutout to all the transparent traders here on X.

If you wanna level up your trading skills follow these legends.

-@MuroCrypto

-@SailorManCrypto

-@ThePenguinXBT

-@swisstrader09

-@George1Trader

-@EZCharts_

-@ApeChartz

-@Crypto_Scient

-@tradermatt

-@cryptolala

Sorry if i forget one, enjoy your weekend🫶

English

Anyone got Masters alpha?

Feel like sprinkling on some long shots.

polymarket.com/event/the-mast…

English

Upon request, I'll post some educational content here with live example today

Just from the chart today we could see we had a huge impulse up met by larger sellers right at 72.7 so that was the initial level to watch this morning

Upon sweeping/retesting the high, we could see large longs entering and chasing price

Could just observe this by looking at flow + OI + delta

These longs were met by similar passive sellers around the same level and we began to reject that level, trapping the longs and closing SFP

This led to over a 2% drop as the longs started to unwind and increase sell pressure

Easy trade this morning based off simple price action

#BTC

English

BANG closed 50% of my btc long here for a +$1600 move 🔥

Gave you guys the perfect bottom level yesterday when we were $2000 higher

Plan the trade, trade the plan.

Hope you guys caught this with me🤝

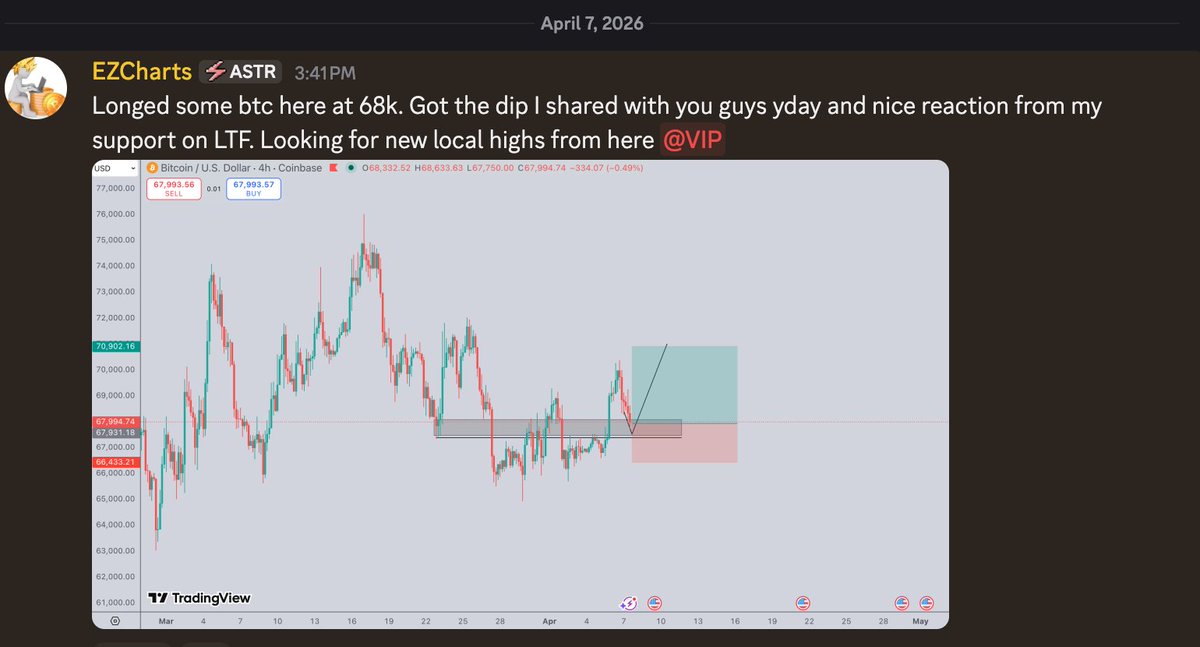

EZcharts@EZCharts_

Area I'm watching for long triggers on btc Dip into 67's, hold s/r and previous low and get our next leg up Looking for this tomorrow if market provides

English

Bang, Closed btc longs for a nice +$2000 move 🔥

Sniped the pico bottom on friday held through the weekend and fully secured gains on this weekend pump

Show some love and I'll tweet my next trade on here too this week

Let's keep rolling.

EZcharts@EZCharts_

Longed some btc at 65.7k looking for a bounce back to 68k Nice sweep of our local low on NYO with 65.5k support right here I think we can bounce from here, but wrong on an hourly close below 64.8k

English

$BTC

CLOSED longs for a +$1500 move

Sniped the bottom on here and held through the chop

More trades coming next week, hope everyone has a great weekend

ggs

ApeChartz@ApeChartz

$BTC Bang! Perfect bounce off 3-tap + demand and 50% position closed Still looking for $68ks for full TP Discord is cooking, what a snipe!🔥

English

Instant pop off entry and closed 50% of my long for a quick +$1200 move 🔥

Local high swept after our local low did and securing profit here

Hold above 66.5k and I think this runs to full tp but risk taken care of

lfg

EZcharts@EZCharts_

Longed some btc at 65.7k looking for a bounce back to 68k Nice sweep of our local low on NYO with 65.5k support right here I think we can bounce from here, but wrong on an hourly close below 64.8k

English

@ApeChartz You’re allowed to keep passively investing/yielding

English