Angehefteter Tweet

AsymmetricEdge

62 posts

@AsymEdge

Ex-quant. Investing own capital. Asymmetric opportunities — where price diverges from reality. Opportunity Map • Valuation • Signals Tech, Crypto, Commodities

The S&P 500 is currently on pace for its worst month since 2022 🔴

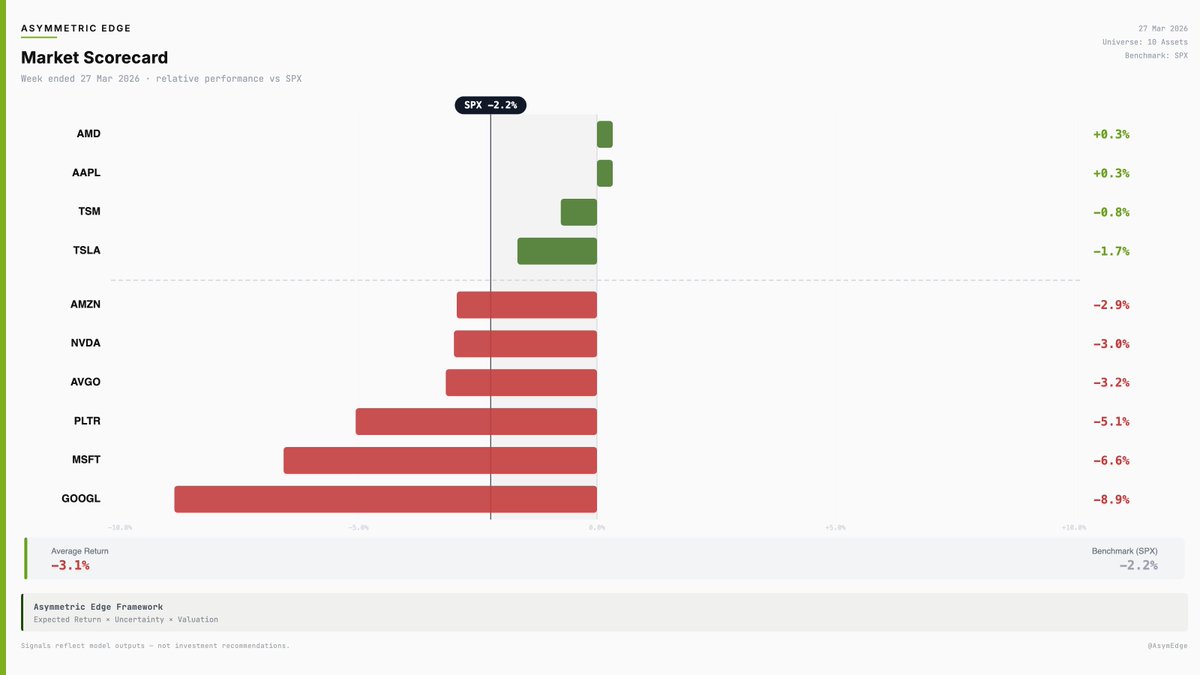

STAY AWAY from semiconductor stocks. The global semiconductor industry is expected to hit $975 billion in sales this year. A historic peak. Revenue growth north of 25%. Every cycle peak sounds the same: this boom is STRUCTURAL, not cyclical. AI demand is permanent. The old rules don't apply. "It's different this time," they say. I've heard those 4 words more times than any others in 45 years on Wall Street. They're always wrong. Here's how I think about it: When any industry generates obscene profits, capital floods in to compete those profits away. The higher the margins, the faster it happens. Semiconductor margins right now are at levels that would make a drug cartel blush. Look at Micron. The crowd says it's "cheap" because the PE looks low. Except Micron's price-to-book ratio sits at roughly 7x. The 10-year median is 1.86x. The historical floor is 0.81x. That's not cheap. That's the most expensive this stock has EVER been relative to its asset base - dressed up in a low PE because earnings are wildly above trend. This is the oldest trap in cyclical investing. You see it in shipping. You see it in commodities. Earnings spike, multiples look compressed, everyone piles in. Then the cycle rolls over and those "cheap" earnings disappear. Now layer on the bigger picture: New capacity is already being announced across the industry. The hyperscalers alone - Microsoft, Amazon, Alphabet, Meta - plan to pour $600-700 BILLION into AI infrastructure this year. That's 70%+ more than 2025. They're consuming roughly 90% of their operating cash flow on capex. Borrowing north of $400 billion to cover the rest. Nobody can afford to stop spending because everyone else keeps spending. It's mutually assured destruction with better PR. And historically, the companies that spend the MOST on capex deliver the WORST stock returns. BCA Research just argued AI threatens all 3 pillars of Big Tech profitability; 1. Economies of scale 2. Network effects 3. Proprietary tech Goldman Sachs compared software stocks to NEWSPAPERS in the early 2000s. The group that fell 95%. Software is now underperforming the Nasdaq by the widest margin this century. Meanwhile, the rotation I've been positioning for is already underway: Most MAG 7 names are DOWN year to date. Emerging markets are up. Energy is up. Gold miners are up. Last year, the EM ETF returned roughly DOUBLE the S&P. This isn't starting. It's been happening since 2024. So my framework is simple: Valuation doesn't matter in the short run. But the longer you go out, the more it matters. And money ain't free anymore. When capital was free, pigs flew. Unprofitable companies soared. Narrative crushed fundamentals. That era is OVER. The 60/40 portfolio hedges against recession. But recession isn't the risk. The risk is continued money printing, persistent inflation, and higher real rates. Bonds don't protect you from that. Gold does. Energy does. Real assets do. You don't need to get clever here. Just avoid what's overpriced and own what's cheap. The regime is changing. The market's scorecard already tells you that every single day. Are you listening?

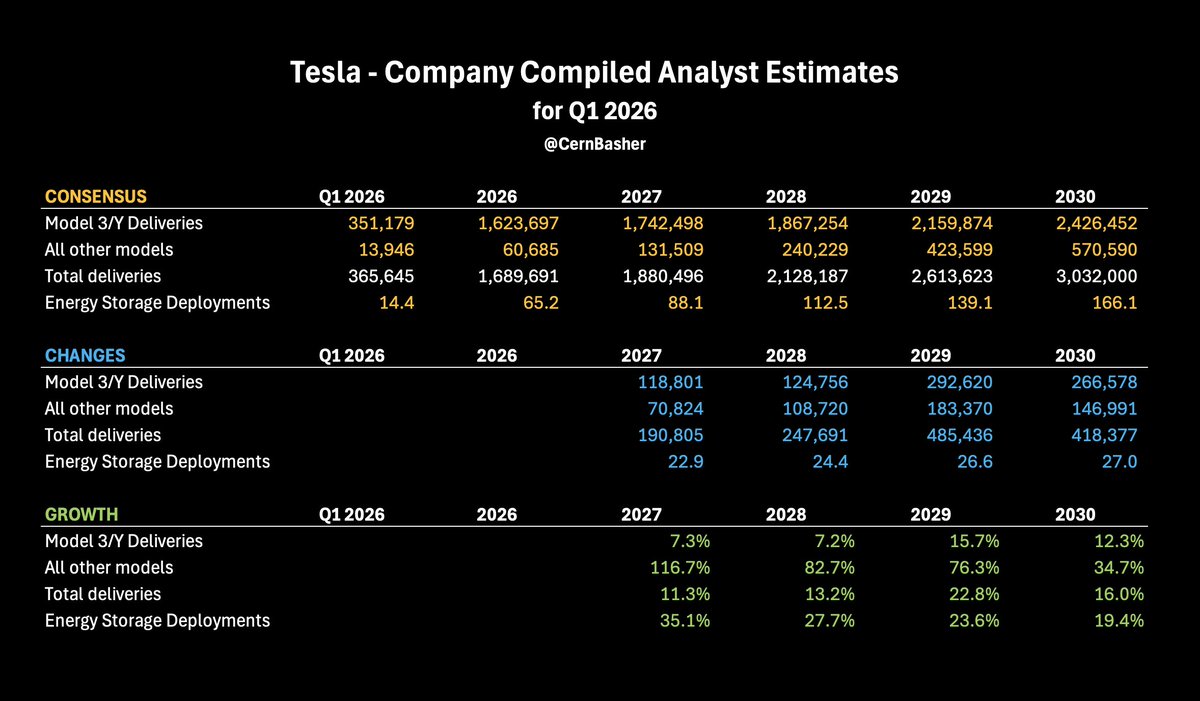

I like that we get these now quartely. Link: ir.tesla.com/press-release/…

We have been surpassed: AI written output exceeded human written output in 2025