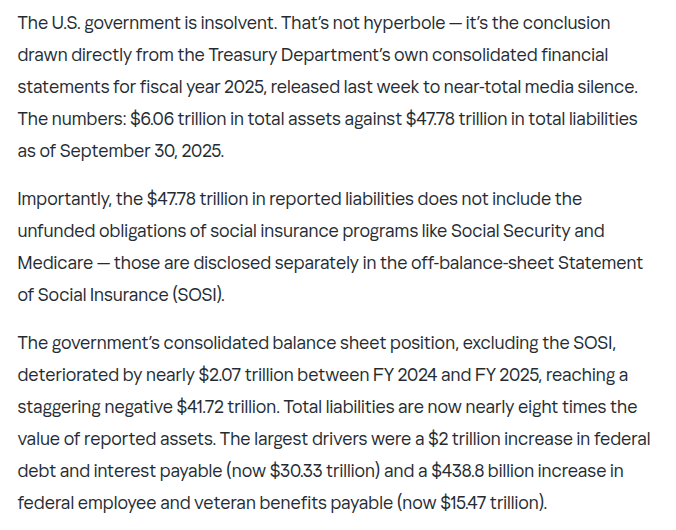

Michael Pettis@michaelxpettis

Thanks, Michael, you're exactly right. In many of my discussions the assumption they make, often without realizing it, is that trade is always balanced, probably because almost all the most important trade models implicitly (and often explicitly) assume balanced trade.

And because they understand how the system works only under conditions of balanced trade, they see no point in discussing the effects of persistent trade imbalances.

But for me the meaningful question is not about whether foreigners use dollars to invoice the two sides of their balanced trade. That is an interesting question for a completely different set of reasons (for example, how US capital controls created the eurodollar market of the 1960s, 1970s and early 1980s). But in that case it is also obvious, as Gopinath argues, that whichever currency foreigners use can have no impact on the US trade balance.

The question here is a completely different one: which assets do foreigners use to balance their structural excesses of exports over imports? The answer to that question has everything to do with who runs the corresponding imbalances. If capital-rich foreigners prefer to invest their excess saving in capital-poor developing economies, as the economic textbooks prescribe, it will be developing economies (like the US during much of the 19th Century) that will run the corresponding deficits, and in many cases these will be healthy deficits because they will be driven by higher investment.

But if, as is actually the case, capital-rich and capital-poor foreigners run structural trade surpluses, and invest their excess saving mainly in a trio of capital-rich countries (the US, the UK and Canada), then clearly it is that trio that will run the bulk of the deficits.

Does it matter? Economists say it doesn't, but of course it does. When capital flows into developing economies in which investment is constrained by scarce domestic saving, it can lead to higher overall investment, which is good for global growth.

But if it flows into advanced economies in which investment is constrained by scarce domestic demand, it won't lead to higher investment, in which case it must reduce saving, either by suppressing domestic demand (as Keynes and Joan Robinson warned) or by boosting domestic debt.

But the main point is much simpler. Economies like Japan, Germany, China, South Korea, Sweden, Taiwan, etc. that have run structural trade surpluses for decades did not do so because they were forced by domestic imbalances in the US. These were all the result of conscious industrial policy decisions. Belive it or not, they have agency.

But economies that run structural trade surpluses have also had no choice but to balance those surpluses by acquiring foreign assets. The claim by Gopinath (and many others) that how and where they decide to invest those surpluses has no impact on the external imbalances, and thus the internal imbalances, of the destination economies makes no sense to me. A decision by a surplus country to run a $100 surplus with the world and to balance it by acquiring $100 of US assets means that unless the US itself intervenes, it must run the corresponding deficit.

Some might argue that "all the US has to do" is reduce its fiscal deficit by $100 and it will no longer run the a $100 trade deficit. This is wrong for at least two reasons. First, US fiscal policy should be determined by the needs of the US economy, and not the needs of foreign surplus economies.

Secondly, and more importantly, the idea that a $100 reduction in the US fiscal deficit will reverse the $100 investment by the surplus country into the US assumes that foreign surpluses are caused by US saving shortfalls. But Gopinath seems to agree that countries like China have agency, and that China's surpluses are the result of Chinese domestic policies, in which case why should they disappear if the US fiscal deficit declines? And if they don't disappear, why should foreigners stop balancing surpluses by acquiring US assets if the US fiscal deficit declines? isn't it possible that this would make the US an even safer destination, in which case net inflows into the US might actually rise?

It cannot be simply a coincidence that nearly three quarters of net capital flows end up in the three advanced economies (the US, the UK and Canada) with the most open capital markets, the most sophisticated and developed financial markets, and the least restrictions on foreign ownership. And because nearly three quarters of these capital flows end up in these three economies, it is also not a coincidence that these three economies account for nearly three quarters of global trade deficits.