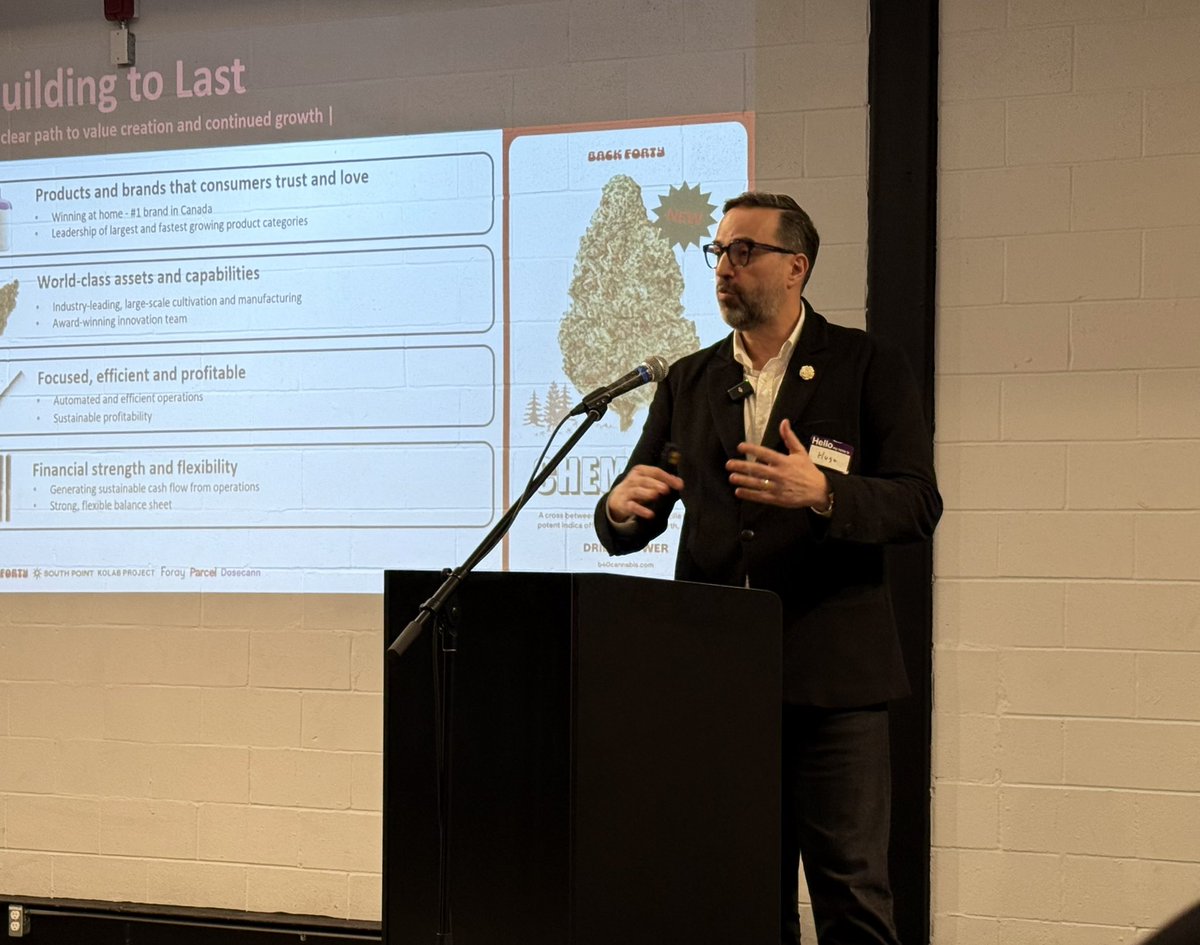

A lot of hard work and a lot of great people made these results possible. Grateful to our team, our partners, our customers and everyone who has backed us along the way. Proud of what we've built together - and focused on what comes next. 🙏 $cbwtf $xly.to

Auxly Cannabis Group@AuxlyGroup

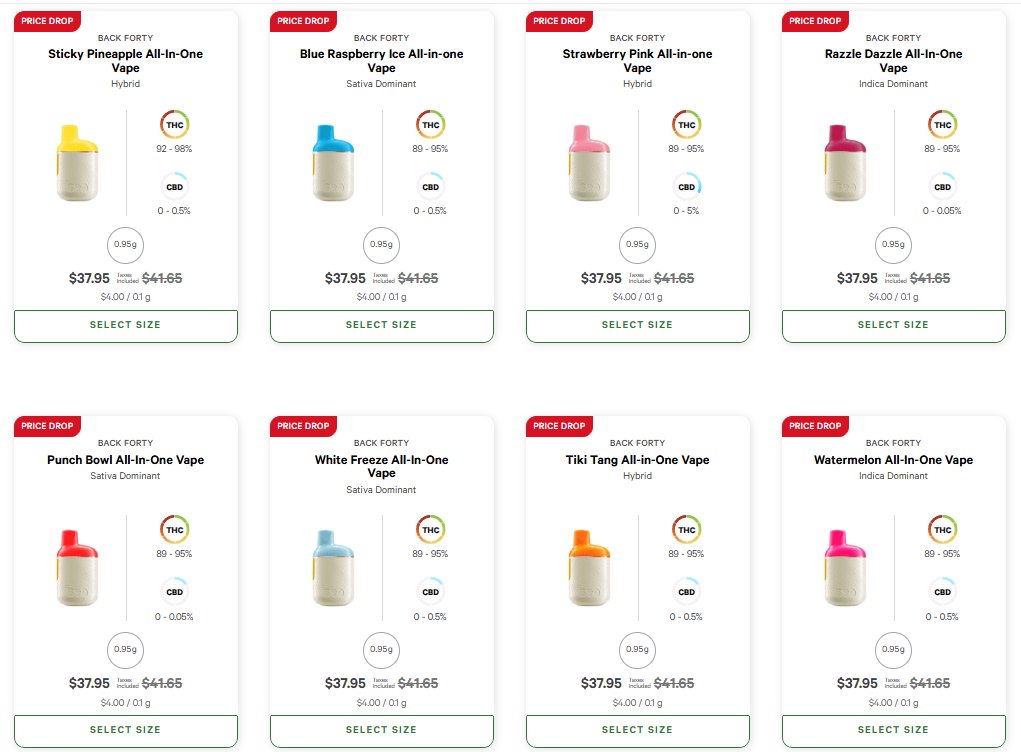

“In 2025, Auxly delivered 24% net revenue growth and 65% Adjusted EBITDA growth. Back Forty was the #1 cannabis brand in Canada for the entire year – a testament to the strength of our products, innovation, distribution and, most importantly, our people.” $XLY.TO $CBWTF

English