Angehefteter Tweet

Position Journal

1.4K posts

@PositionJournal

I journal on my stock positions before buying. Mag7 Principal. Concentrated portfolio and evidence-based research. Outperformed SP500 by 2x in prev. 3 years.

100% not financial advice and don’t transact on this but: The candle on SPY today is the kind that you see near tradable bottoms

Politically speaking, especially with the mid-terms, Trump may look to make April the greenest month we've seen in a while. A total reversal of 2025 liberation day, by timing the announcement of multiple completed trade deals, targeted tariff relief on key allies, and fresh pro-growth executive orders right around the April 2 anniversary. This is to be able to say something like: “One year passed since Liberation Day, and the DOW is at record highs of xxK" If you think he's not able to, you forget that the market has "settled in" to the shocks of tariffs and all the fiasco from 2025. He very well could reset us to go higher.

𝕏 is reportedly developing AI-generated content detection features that will prompt users with a warning before allowing them to post.

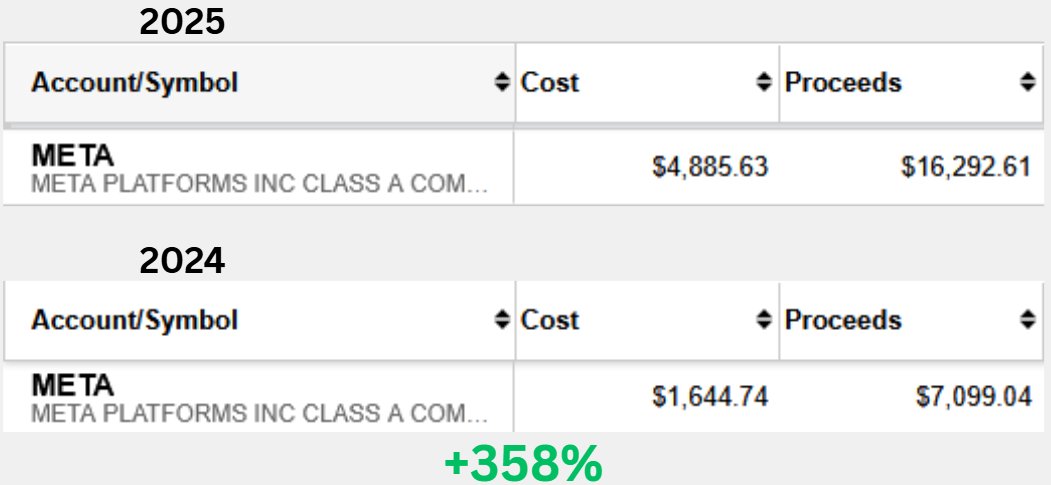

$META bulls totally miss how slow moving large organizations are and how they don't deliver instant yields after a major pivot or strategy shift. Don't expect instant rebounds. Here's the real timeline most investors miss, speaking from experience YEAR 1: Planning, heavy investment, internal deliberation, what will we do, when, why and how (Meta announces $70B in CapEx, rolls out Llama foundation model, begins massive integration of AI into their platforms). Market gets hyped on the announcements in AI such as promise of increased AI investments and stock often rallies on the vision. Year 1 passed, we saw highs of $750-780 in 2025 YEAR 2: Execution kicks in based on the plan. But the markets have already been ecstatic and they expect results and fireworks NOW. But true returns will only be delivered late Year 2 at best. You cannot expect Year 1's vision to have delivered returns. That means the rally to $750 was unjustified fundamentally. In Year 2, $META announces they're still executing to the plan and everything is fine, but the cash balance dropping from billions of CapEx coupled with revenue not materializing now SHAKES UP THE MARKET. This is when hope fades, selling pressure hits, and the stock gets punished. We saw this play out when Meta announced earnings this year and stock popped from $666 to $738 (+10%) and only for it to fade back down even lower, to now $617. A -16% drop despite amazing results, why did this happen? Because we are impatient investors, we need our money now, we need to see the future, today. YEAR 3: If execution is near-PERFECT, returns finally start to materialize and potentially explosively. But honestly, taking just 1 year to execute to core objectives is unrealistic. This is easily observed once you've seen the inner workings of how a Mag7 operates. I think we are in Year 2. Zuckerberg is executing, returns on investments will not be meaningful yet, but market hype and money will outflow, as it already happened dropping from $738 to $617, and will likely continue to outflow. But in reality, the company is improving. My message for you: $META bulls you are going to have to be much more patient. Expect more short-term pain. This is a long-term hold, record revenue, AI tools already at scale in ads and a clear path to frontier model releases. Wait it out until Year 3, to see if Zuck nailed the execution.

Today was the date I have been waiting for since January. 3/19. Here is everything that happened today & what may next. 🧵

Today is a sad day for me. I’ve decided to part ways with a large portion of my $HOOD shares. Not because I’ve lost conviction in the company. I still believe in the business and in Vlad’s leadership. But I’m staying disciplined to my macro thesis. I believe the next few years could be severely impacted by economic headwinds. If consumers have less capital, they have less to invest. And if they have less to invest, platforms like Robinhood feel that pressure. AI is advancing at an incredible pace. I believe it will drive productivity, but I also believe it could accelerate unemployment faster than we’re prepared for. Less disposable income across America means less money flowing into stocks. It’s that simple. I could be wrong. I genuinely hope I am. But I’m positioning for what I believe is coming. I’m building my fortress. Before trimming, I held 2,500 shares. Now I hold 1,400 shares, still one of my largest positions at roughly 20% of my portfolio. What am I doing with the cash? For now, I’m staying patient. Holding tight. Adding to $GLD. Observing. If the environment unfolds the way I expect, I want to be in a strong position to act decisively. Godspeed, fam.

$META bulls totally miss how slow moving large organizations are and how they don't deliver instant yields after a major pivot or strategy shift. Don't expect instant rebounds. Here's the real timeline most investors miss, speaking from experience YEAR 1: Planning, heavy investment, internal deliberation, what will we do, when, why and how (Meta announces $70B in CapEx, rolls out Llama foundation model, begins massive integration of AI into their platforms). Market gets hyped on the announcements in AI such as promise of increased AI investments and stock often rallies on the vision. Year 1 passed, we saw highs of $750-780 in 2025 YEAR 2: Execution kicks in based on the plan. But the markets have already been ecstatic and they expect results and fireworks NOW. But true returns will only be delivered late Year 2 at best. You cannot expect Year 1's vision to have delivered returns. That means the rally to $750 was unjustified fundamentally. In Year 2, $META announces they're still executing to the plan and everything is fine, but the cash balance dropping from billions of CapEx coupled with revenue not materializing now SHAKES UP THE MARKET. This is when hope fades, selling pressure hits, and the stock gets punished. We saw this play out when Meta announced earnings this year and stock popped from $666 to $738 (+10%) and only for it to fade back down even lower, to now $617. A -16% drop despite amazing results, why did this happen? Because we are impatient investors, we need our money now, we need to see the future, today. YEAR 3: If execution is near-PERFECT, returns finally start to materialize and potentially explosively. But honestly, taking just 1 year to execute to core objectives is unrealistic. This is easily observed once you've seen the inner workings of how a Mag7 operates. I think we are in Year 2. Zuckerberg is executing, returns on investments will not be meaningful yet, but market hype and money will outflow, as it already happened dropping from $738 to $617, and will likely continue to outflow. But in reality, the company is improving. My message for you: $META bulls you are going to have to be much more patient. Expect more short-term pain. This is a long-term hold, record revenue, AI tools already at scale in ads and a clear path to frontier model releases. Wait it out until Year 3, to see if Zuck nailed the execution.

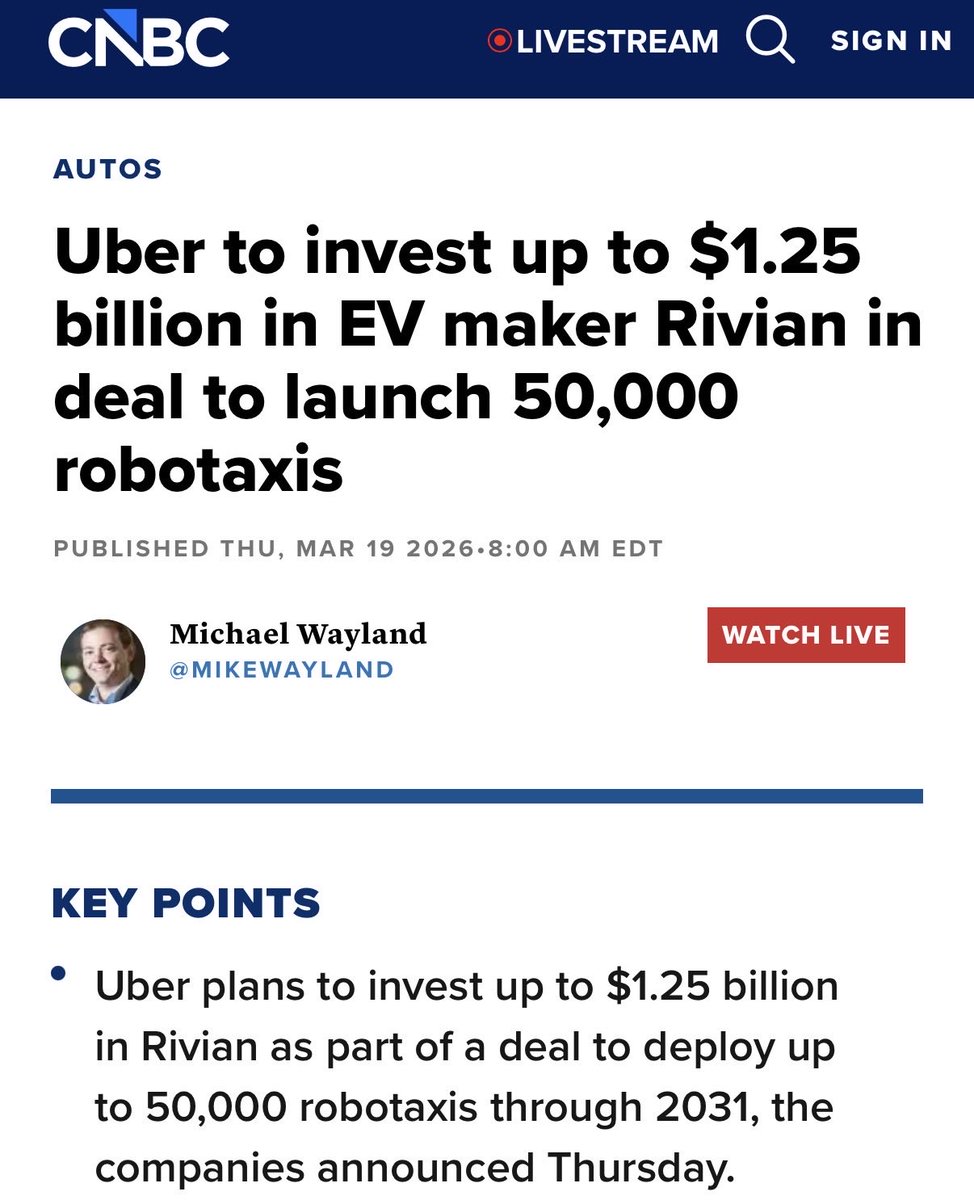

I have two medium risk, high reward positions I’m contemplating about which one to add to I’ll keep the post short because I usually write too long anyway. $RIVN - betting on American 🇺🇸 manufacturing, clean, reliable and loved cars, with self driving only 1.5 years behind Tesla and margins meaningfully boosting profits. The market always needs a #2 in every segment — and Rivian is it. $HIMS - NVO not only dropping suit but partnering up means both companies thought through a comprehensive gameplan. Dudum reconfirmed the 6.5B commitment by 2030 and growth overall is not slowing down. This private litigation was the biggest overhang, FDA commissioner already provided favorable comments and I think the DOJ will be a slap on the wrist if it even goes anywhere. I’m trying to journal my thoughts to really think it through — what bull and bear angle (short answers fine) am I missing?

@nikitabier @elonmusk I'm finding that Reddit algorithm rewards content quality and niche fit better. While X's algorithm rewards account authority and velocity Genuine question: how can small X creators be discovered without relying on bigger accounts? Reddit -Account created 10 days ago -Article posted 2 days ago -Posted X article with no images -136K views X -Account created Feb 2023 + Verified -Article posted 2 days ago -With images (implying higher engagement/retention) -500 views My X article was dead on arrival, while my Reddit article, with exact same content, received a fair shot.